Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

The focus is on America’s cryptocurrency surge, while Israel and Pakistan might be indicating future trends.

This month, Israel and Pakistan provided a more subdued examination for cryptocurrency compared to the ongoing situation in US capital markets. What if the more significant transition in 2026 is occurring at the intersection of digital assets and local currencies along with bank accounts?

The Israeli cryptocurrency company Bits of Gold announced that Israel’s Capital Market Authority has sanctioned the issuance and distribution of BILS, a stablecoin pegged to the shekel, following a two-year pilot program. Just days prior, the State Bank of Pakistan released BPRD Circular Letter No. 10 of 2026, which revokes its 2018 ban on virtual currencies.

This circular from Pakistan permits regulated entities to establish bank accounts for PVARA NOC or licensed VASPs and their clients under specified compliance conditions.

These two developments are quite distinct from the US spot ETF cycle. However, they highlight the operational framework that determines whether cryptocurrency evolves beyond merely being an investment vehicle. The US has provided legitimacy, liquidity, and a significant debate regarding the digital dollar.

Other regions are exploring a different operational framework: whether cryptocurrency can integrate with local currencies, bank accounts, merchant payment systems, and enforceable market regulations.

Related Reading

Related Reading

CLARITY Act stablecoin fight shifts from yield to who captures digital-dollar economics

Washington’s stablecoin regulations are transforming a yield competition into a broader struggle over payments, reserves, wallets, and banking infrastructure. Apr 28, 2026 · Liam 'Akiba' Wright

This distinction alters how global adoption should be assessed. A Bitcoin ETF allows investors to gain exposure. A regulated shekel stablecoin enables users to maintain a domestic currency on-chain.

A central bank circular permitting licensed cryptocurrency firms to open accounts provides the sector with a pathway back into regulated banking. The first validates an asset class, while the second and third assess whether cryptocurrency can evolve into usable financial infrastructure.

The evaluation is still in its early stages. BILS requires proof of issuance and utilization. Pakistan still needs licensed VASPs with genuine banking relationships. New licensees in Hong Kong still need to initiate their business operations.

The UAE still requires clearer public alignment between dirham-token announcements and entries in the Central Bank register. Nonetheless, the emerging trend is becoming increasingly difficult to overlook: in 2026, the practical work surrounding cryptocurrency is increasingly focused on where digital assets intersect with money, banks, merchants, and settlement systems.

Local money and bank access

Bits of Gold states that the approved BILS initiative is a shekel-pegged stablecoin originally developed on Solana, with involvement from Fireblocks, QEDIT, EY, and the Solana Foundation during the pilot phase.

The policy indication is the local-currency aspect. BILS introduces the shekel into an on-chain market that is predominantly influenced by dollar stablecoins and raises the question of whether a national currency can achieve a programmable version without relinquishing the entire payments framework to USD tokens.

This represents the monetary-sovereignty perspective. Dollar stablecoins have become the primary unit for much of the settlement activity within the cryptocurrency space.

A shekel token, contingent upon issuance and adoption following approval, offers Israel a means to experiment with domestic-currency rails within that same infrastructure. The outcome will be assessed less by market visibility and more by whether wallets, exchanges, payment providers, and regulated entities find a rationale for its use.

Pakistan provides the banking component of this development. The State Bank of Pakistan circular is significant as it replaces FE Circular No. 3 of 2018 and allows SBP-regulated entities to open accounts for PVARA NOC or licensed VASPs and their clients.

The circular also links access to banking controls, documentation, monitoring, customer-risk assessments, and adherence to Pakistan’s virtual-asset regulations.

This alters the operational landscape for licensed cryptocurrency firms. Bank accounts are fundamental financial infrastructure. They determine whether a regulated VASP can manage client funds, reconcile transactions, fulfill due diligence, and channel activities into monitored pathways.

For a market like Pakistan, which Chainalysis ranks among the top countries for cryptocurrency adoption, access to banking can dictate whether usage remains informal or transitions into traceable institutional frameworks.

Hong Kong serves as a licensing comparison for the same rails-first approach. On April 10, the Hong Kong Monetary Authority granted stablecoin issuer licenses to Anchorpoint Financial Limited and The Hongkong and Shanghai Banking Corporation Limited.

The HKMA register includes both with effective dates of April 10, 2026. This transition moves the jurisdiction from policy formulation to identified licensed issuers, while leaving the business-launch and user-adoption evaluations ahead.

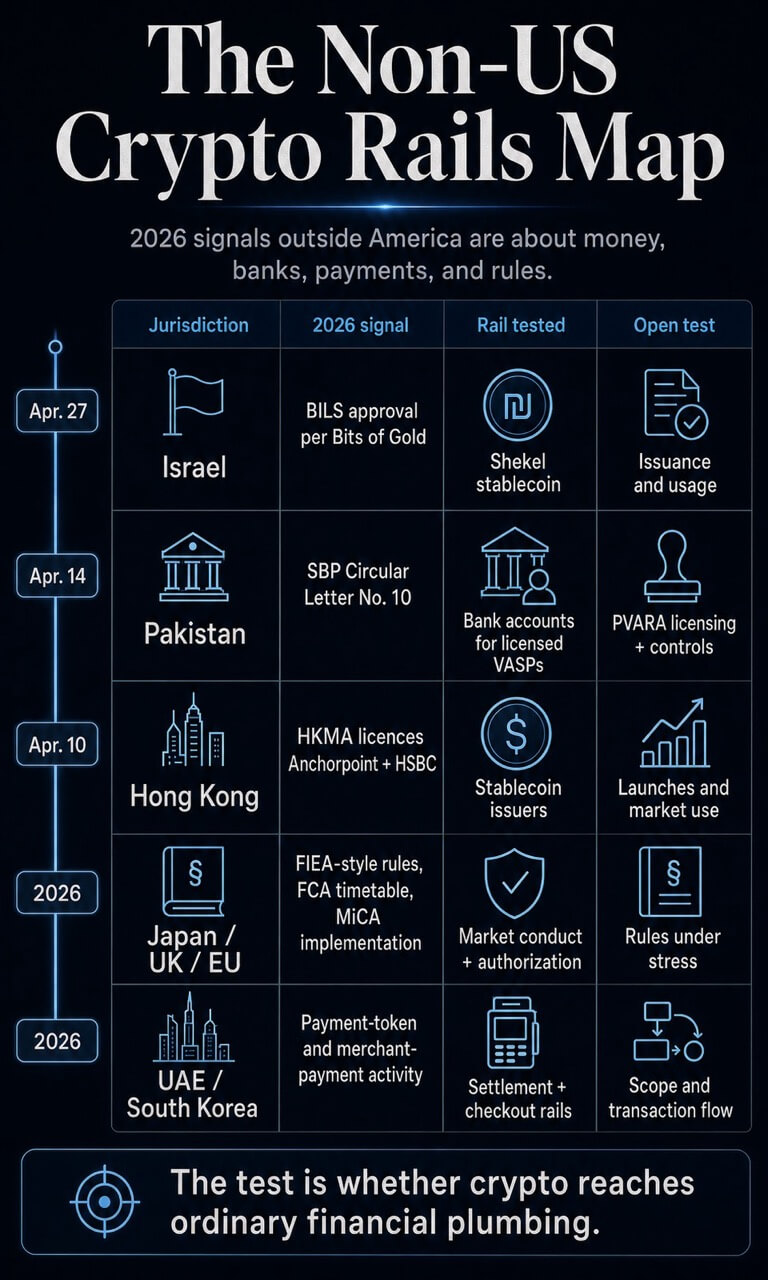

The preliminary overview is clear:

| Jurisdiction | 2026 signal | Rail being tested | Open test |

|---|---|---|---|

| Israel | Bits of Gold approval statement | Local-currency stablecoin | Issuance, redemption, and user uptake |

| Pakistan | SBP Circular Letter No. 10 | Bank accounts for licensed VASPs | PVARA licensing and bank controls |

| Hong Kong | HKMA stablecoin issuer licenses | Named licensed issuers | Launches and market use |

| Japan, UK, EU | Rulemaking and implementation timelines | Market conduct and authorization | How rules perform under stress |

| UAE, South Korea | Payment-token and merchant-payment activities | Settlement and checkout rails | Scope, transaction flow, and adoption |

Rulebooks are becoming operating layers

This same trend is evident in conduct regulations. Japan’s Financial Services Agency has released documents indicating a transition from Payment Services Act treatment to Financial Instruments and Exchange Act-style oversight for crypto-assets.

The working-group report advocates for information provision, controls for crypto-asset service providers, market-abuse regulations, insider-trading rules, SESC powers, and enhanced user protection. The FSA’s weekly review also mentions draft Acts submitted to the Diet related to FIEA and PSA amendments.

Japan’s indication pertains to classification and conduct. Crypto assets are being directed toward a framework where disclosure, monitoring, and misconduct regulations influence participation. This makes access contingent upon behavior, oversight, and accountability.

It also illustrates why regulatory design can serve as a form of infrastructure. Markets utilize law as a routing layer when participants need clarity on who can list assets, who can hold them, who can market them, and which trading behaviors incur liability.

The UK is establishing a similar operational framework with an extended timeline. The FCA states that firms wishing to engage in new regulated cryptoasset activities can apply from Sept. 30, 2026, to Feb. 28, 2027.

Related Posts

The new framework is anticipated to be implemented on Oct. 25, 2027. A related consultation notice indicates the regulator is progressing through authorization, oversight, consumer duty, custody, prudential, and market-abuse considerations.

Europe has already established a broader framework. ESMA asserts that MiCA introduces uniform regulations for crypto-assets encompassing transparency, disclosure, authorization, oversight, consumer information, market integrity, and financial stability.

A wider global regulatory landscape has already demonstrated that regulation is evolving as a multi-market process. The 2026 layer adds a more precise focus: rulebooks are beginning to dictate how crypto products integrate into conventional financial channels.

The UAE provides an example of payment-token regulation, but scope remains a limitation. The Central Bank’s Payment Token Services Regulation outlines the framework for payment-token activities, while a February CBUAE register offers a public verification of licensed entities.

Additionally, an ADX-hosted announcement states that IHC, Sirius, and FAB have received CBUAE approval to launch the dirham-backed DDSC on ADI Chain for institutional payments, settlement, treasury, and trade flows.

Currently, the evidence suggests a regulated payment-token framework and institutional settlement aspirations; widespread retail usage would require additional proof.

South Korea introduces a merchant layer. Crypto.com and KG Inicis announced in March that they would integrate Crypto.com Pay across KG Inicis’s merchant network for international travelers and K-commerce users, allowing merchants to accept either fiat or digital assets.

South Korea’s K Bank collaboration with Ripple indicates another rail where banking and payment activities intersect with cryptocurrency. Both instances still require transaction data.

Their significance lies in shifting the adoption discussion toward checkout, settlement, remittance, and consumer-facing access.

Related Reading

Related Reading

The South Korean bank powering Upbit is testing Ripple integration for cross-border payments

South Korea’s Kbank is piloting Ripple-powered remittances, assessing whether bank-linked crypto rails can develop into genuine payment infrastructure. Apr 27, 2026 · Liam 'Akiba' Wright

Usage is the harder test

The US-centric interpretation remains influential due to the substantial figures involved. On April 29, the total cryptocurrency market capitalization was approximately $2.59 trillion, with Bitcoin valued at around $1.56 trillion.

Dollar stablecoins continue to dominate the active liquidity layer, with Tether’s 24-hour volume nearing $111.50 billion and USDC around $47.84 billion.

These statistics clarify why US policy and dollar rails consistently attract attention. The dollar stablecoin ecosystem is already substantial. US capital markets provide legitimacy at scale.

The CLARITY Act stablecoin debate illustrates that the US discussion also revolves around who captures the economic benefits of digital dollars. This benchmark remains crucial, as global cryptocurrency infrastructure still relies heavily on dollar liquidity.

Usage data complicates this benchmark. Chainalysis reported that adjusted stablecoin economic volume reached $28 trillion in 2025, with a baseline projection of $719 trillion by 2035 and a catalyst scenario approaching $1.5 quadrillion.

As projections, these figures represent scenario calculations rather than evidence of future payment flows. Their trajectory shifts the operational inquiry: stablecoins are being assessed as payment infrastructure, treasury infrastructure, and settlement infrastructure, in addition to their role as trading collateral.

The Chainalysis adoption research highlights why emerging markets are central to this discussion. It ranked India first, followed by the US, Pakistan, Vietnam, and Brazil, characterizing adoption as widespread across income levels.

It also linked sustainable adoption to on-ramps, regulatory clarity, and financial and digital infrastructure. These are the factors being evaluated by Pakistan’s banking circular and by local-currency stablecoin initiatives like BILS.

The IMF addresses the risk aspect. Its March report on stablecoin inflows and FX spillovers indicates that stablecoin movements can influence parity deviations, local currency depreciation, dollar premiums, and financial stability.

In simple terms, stablecoins become increasingly significant once they start functioning like a segment of the FX market.

This creates a live policy tension. Local-currency stablecoins can help maintain the relevance of domestic units in on-chain finance. Banking access can draw VASPs into monitored channels.

Payment integrations can transition cryptocurrency from portfolio exposure to checkout and settlement. Each rail also introduces new supervisory requirements concerning reserves, redemption, anti-money laundering controls, market abuse, and currency pressures.

The evidence indicates a specific division. US ETFs and Wall Street adoption have contributed to the financialization of cryptocurrency by enhancing access to exposure. The more challenging adoption evaluation is occurring where regulators determine whether cryptocurrency can engage with local currencies, bank accounts, merchants, and FX markets.

This evaluation is still in its early stages. BILS requires issuance and usage. Pakistan needs licensed VASPs operating through bank accounts. New licensees in Hong Kong must initiate their operations. Japan, the UK, and the EU require regulations that function effectively under market stress.

The UAE needs clear mapping between issuers and registers. South Korea requires merchant activity beyond mere announcements.

If these indicators materialize, the global cryptocurrency landscape will resemble less a US-led investment-product cycle and more a collection of regional financial systems integrating cryptocurrency under local regulations. If they do not materialize, the dollar and US capital markets will continue to perform the majority of the work.

The next evaluation is usage, measured against visibility.

The post Everyone is watching America’s crypto boom but Israel and Pakistan may be showing what comes next appeared first on CryptoSlate.