Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

US Treasury yields rise to peak levels in a year, creating additional challenges for Bitcoin liquidity.

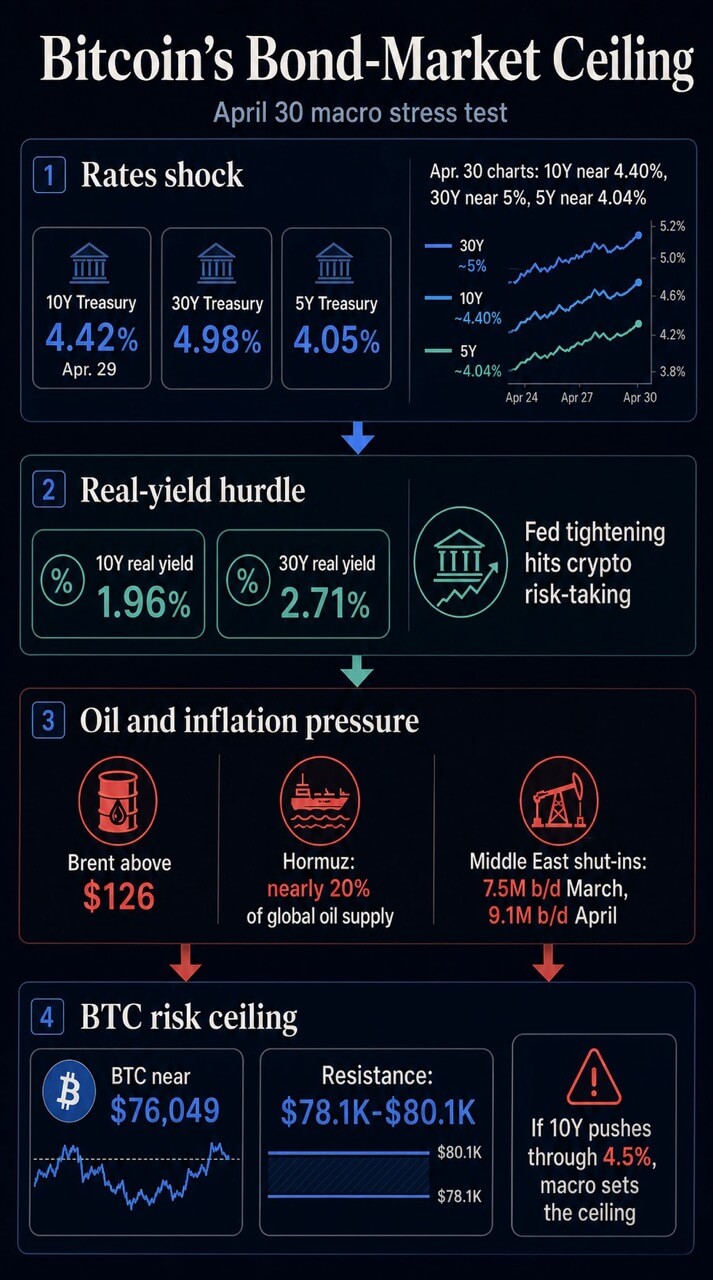

Bitcoin’s rebound in April is currently undergoing a dual macro challenge. The official Treasury curve for April 29 indicated the 10-year yield at 4.42%, the 30-year at 4.98%, and the 5-year at 4.05%.

Market charts today reflect a similar pressure zone, with the 10-year yield around 4.40%, the 30-year near 5%, the 5-year at approximately 4.04%, and WTI crude prices elevated.

Simultaneously, Brent crude is trading above $126, marking its highest level since 2022, following reports that President Donald Trump is prepared to maintain the Iran blockade for several months.

Currently, Bitcoin is priced near $76,049, approximately 40% lower than its peak in October 2025. The overall cryptocurrency market capitalization is around $2.54 trillion, with Bitcoin’s dominance at about 59.9%.

These figures place Bitcoin in a distinct type of challenge. The critical question is whether the rate market is increasing the cost of risk-taking more rapidly than the demand for cryptocurrency can accommodate.

If the 10-year yield approaches or exceeds 4.5%, Bitcoin’s immediate ceiling may be influenced by oil prices, Treasury supply, real yields, and Federal Reserve liquidity operations before being determined by crypto-specific flows.

The market inquiry is straightforward: if bond prices continue to decline, will Washington need to alleviate geopolitical oil pressures or adjust Treasury and Fed operations before Bitcoin can regain risk appetite?

Bond yields are establishing the initial threshold

The primary pressure point is the nominal Treasury curve. A 10-year yield around 4.4% is already nearing the level highlighted by CryptoSlate in its recent analysis of the Bitcoin bond market, where the $80,000 test becomes increasingly challenging.

Related Reading

Related Reading

Bitcoin’s $80k test should be decided by the bond market this week

Bitcoin’s forthcoming movement may be influenced by Treasuries, as a breakout in 10-year yields could determine whether BTC surpasses $80,000 or transforms its inflow trend into another unsuccessful rally. Apr 28, 2026 · Gino Matos

The analysis from April 28 suggested that a breakout above 4.35%, trending towards a 4.6% range, could convert a renewed inflow trend into another failed rally at resistance.

The official curve on April 29 indicated that risk was within reach. The 10-year yield was at 4.42%, the 30-year at 4.98%, and the 5-year at 4.05%.

The long end of the curve is most directly related to duration risk, equity multiples, mortgage pressures, and the discount rate that investors apply to assets with uncertain or distant cash flows.

Bitcoin does not provide a coupon, dividend, or earnings stream. This means its macro case is heavily reliant on liquidity, risk appetite, scarcity demand, ETF access, and balance-sheet demand.

As Treasury yields rise, these factors face a more challenging comparison. Investors can earn nearly 5% at the long end of the U.S. risk-free curve while Bitcoin remains below its early-year highs.

The real-yield layer sharpens the setup. On April 29, the Treasury’s real curve indicated a 10-year real yield of 1.96% and a 30-year real yield of 2.71%.

Treasury publishes these rates as market data. The implications for Bitcoin arise from how BTC has traded within this environment.

Research from the IMF on the crypto cycle and U.S. monetary policy found that a common crypto factor accounted for 80% of crypto price variation and that Fed tightening diminished that factor through the risk-taking channel.

CryptoSlate has also posited that Bitcoin’s recent macro identity resembles a liquidity-sensitive tech beta more than a straightforward hedge against gold or the dollar.

In this context, rising real yields can act as a drag on the market’s willingness to pay for volatility. BTC can still appreciate, but it requires stronger evidence that demand is robust enough to withstand a higher hurdle rate.

Oil has emerged as a rates variable

The second pressure point is oil. Reuters reported that the U.S. was seeking international support to reopen the Strait of Hormuz while crude prices surged, and a U.S. blockade of Iranian oil exports remained part of the pressure strategy amid stalled negotiations.

The Guardian subsequently reported Brent trading above $126 after Trump indicated that the blockade could persist for months.

This issue extends beyond foreign-policy risk. Oil has now become a component of the rate equation because energy prices influence inflation expectations, headline inflation, freight costs, input expenses, consumer pressures, and the Fed’s response function.

The Energy Information Administration’s April outlook provides context. It stated that the Strait of Hormuz had effectively been closed to shipping since February 28 and that nearly 20% of global oil supply typically passes through the strait.

Brent had already approached nearly $128 on April 2. The EIA projected Brent to average $115 in the second quarter, assuming the conflict would ease after April.

A separate EIA report estimated that Middle Eastern producers curtailed 7.5 million barrels per day in March, increasing to 9.1 million barrels per day in April.

This forecast already considered the disruption a significant energy-market event. The latest developments regarding a prolonged blockade challenge the duration assumption underlying that base case.

The Fed has already made the connections. Its April 29 statement noted that inflation was elevated, partly due to rising global energy prices, and that developments in the Middle East were creating significant uncertainty.

Chair Jerome Powell’s opening remarks went further, indicating that March PCE estimates suggested 3.5% headline inflation and 3.2% core PCE, with headline inflation being bolstered by global oil prices.

The vote indicated that the Fed’s constraints were both internal and external. The FOMC maintained the target range at 3.50% to 3.75%.

Stephen Miran dissented in favor of a 25-basis-point cut. Beth Hammack, Neel Kashkari, and Lorie Logan supported the hold but opposed retaining the easing-bias language in the statement.

This division represents the rates-market equivalent of the oil shock. One faction perceived sufficient downside risk to advocate for a cut, while another saw enough inflation risk to resist easing language. Bitcoin is affected by this disagreement.

Related Posts

Policy levers begin with plumbing

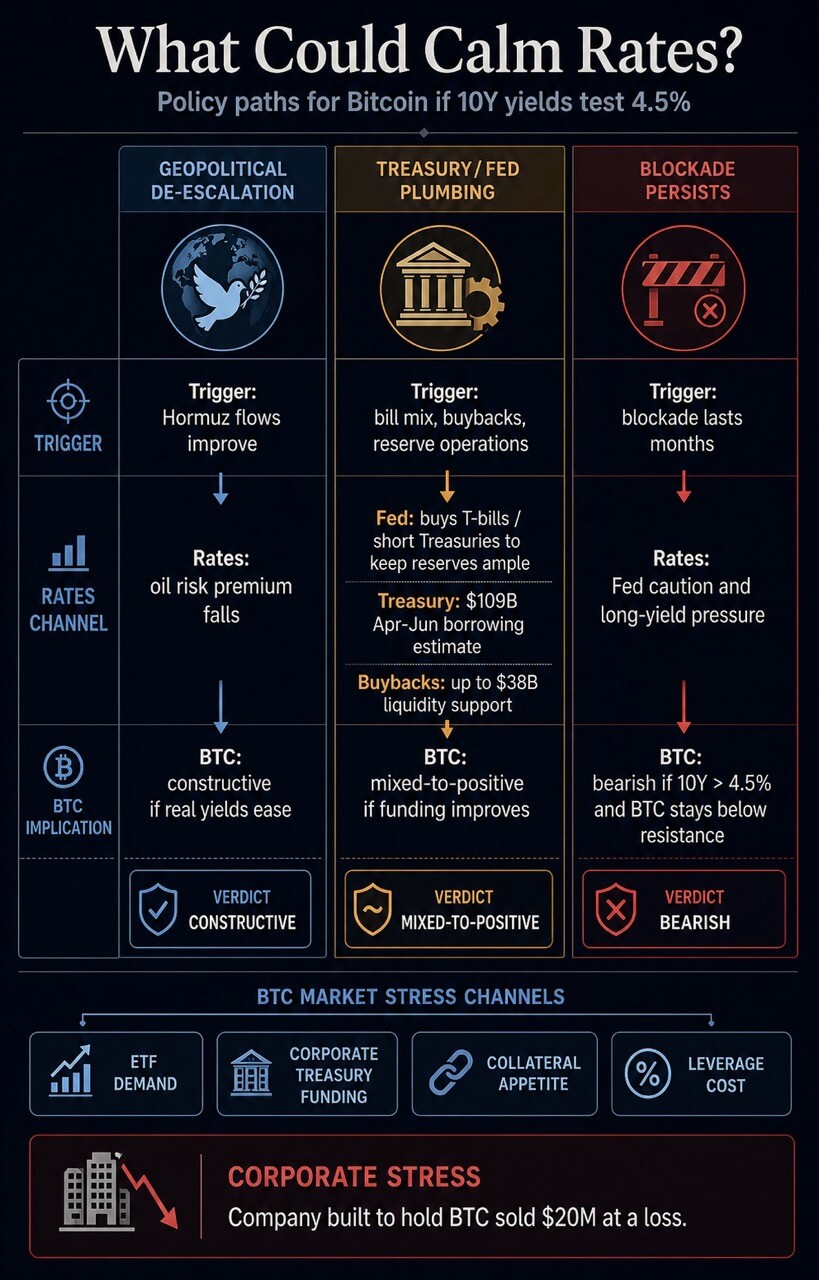

If yields continue to rise, Washington has limited near-term options to alleviate the pressure. One option is geopolitical: reduce the oil shock by altering the blockade strategy or reopening a route for Gulf energy flows.

This approach would be the most straightforward for risk assets as it would directly address the inflation impulse.

Another option involves liquidity management. The Fed’s implementation note maintained the administered-rate structure and instructed the Open Market Desk to purchase Treasury bills, and if necessary, other Treasuries with remaining maturities of three years or less, to ensure an adequate level of reserves.

This serves as a reserve-management tool. It can support market functioning and bank-reserve conditions while still leaving oil prices and term premiums outside the direct toolset.

Treasury has its own mechanisms. Its latest refunding page indicates the next major financing documents are scheduled for May 4 and May 6.

February borrowing estimates projected $109 billion in privately held net marketable borrowing for April through June, with an assumed $900 billion cash balance by the end of June.

The February refunding statement indicated that Treasury could adjust bill sizes, expected the Treasury General Account to peak around $1.025 trillion in late April, and planned buybacks of up to $38 billion for liquidity support, along with up to $75 billion in the one-month to two-year bucket for cash management.

These tools can influence market plumbing. Bill issuance alters the segment of the curve that absorbs supply. Buybacks can enhance off-the-run liquidity.

Related Reading

Related Reading

Bitcoin’s next risk is hiding in the gap between debt and liquidity

US debt is expanding more rapidly than M2, leaving Bitcoin caught between a bullish liquidity thesis and tighter market plumbing that continues to limit risk. Apr 30, 2026 · Gino Matos

TGA movements can either add to or deplete bank reserves. The limitation is that debt management can alleviate financing pressure while energy inflation continues to challenge the Fed.

| Path | Trigger | Rates channel | BTC implication |

|---|---|---|---|

| Geopolitical de-escalation | Hormuz flows improve or blockade pressure eases | Oil risk premium falls, inflation expectations cool | Most constructive path for Bitcoin if real yields ease with it |

| Treasury/Fed plumbing relief | Bill mix, buybacks, reserve operations, or TGA changes ease funding pressure | Liquidity conditions improve while oil risk remains live | Mixed-to-positive if real yields fall; weaker if it reads as stress response |

| Blockade persists | Oil stays elevated and duration extends beyond EIA’s April assumption | Fed keeps caution, long yields stay pressured | Bearish if the 10-year moves through 4.5% and BTC stays below resistance |

| Flow-led Bitcoin rebound | Spot and ETF demand absorb short-term holder supply | Rates stay high but stop accelerating | BTC can recover, but durability still depends on bonds calming |

Each path remains conditional. A geopolitical channel would directly address oil-inflation pressure. A plumbing channel would need to enhance funding conditions without making the response appear as stress.

The market still needs to demonstrate which path is active.

Bitcoin’s market has limited capacity

Bitcoin’s price structure highlights the macro squeeze more clearly. BTC dropped below $76,000 following the Fed’s decision, and Glassnode data indicated short-term holder profit-taking around the $78,000 to $79,000 range.

The same report noted that buyers would need to absorb overhead supply to advance towards $84,000, while a decline below $68,000 would reveal a deeper correction path.

CryptoSlate’s April 28 bond-market analysis identified the critical battleground around $78,100 to $80,100. This area now serves as a practical confirmation zone.

A reclaim would indicate that spot demand, ETF demand, or positioning can withstand the macro shock. A rejection would reinforce the notion that the bond market continues to set Bitcoin’s ceiling.

The broader liquidity context supports this caution. CryptoSlate’s April 30 debt-and-liquidity analysis argued that U.S. debt is increasing faster than M2 and that Treasury issuance, the Treasury General Account, reserve balances, and bank-credit conditions can maintain tight financial plumbing even as broad money rises.

A separate CryptoSlate analysis of M2 found that Bitcoin’s liquidity relationship is lagged and dependent on the regime, with real yields, the dollar, ETF flows, and geopolitical shocks capable of overriding the simple money-supply argument.

Corporate treasury demand introduces another channel. CryptoSlate’s coverage of the Bitcoin treasury trade indicated that corporate and sovereign holders may become sellers when funding pressure rises, debt needs increase, or cash becomes more valuable than balance-sheet optics.

A company designed to accumulate BTC, selling $20 million at a loss, exemplified this risk concretely.

This is why the current setup extends beyond spot traders. Rising Treasury yields can exert pressure on Bitcoin through discount rates, ETF demand, corporate treasury funding, collateral appetite, and the cost of leverage.

Oil continues to constrain the Fed. Treasury supply keeps reserves and term premiums in focus. Bitcoin’s own supply zone dictates how swiftly these macro forces manifest in price.

Bitcoin can still experience a rally from this point. A sufficiently strong flow bid can absorb profit-taking temporarily, and previous CryptoSlate coverage of oil conflicts indicated that BTC can withstand crude pressure intraday when demand is present.

Related Reading

Related Reading

Bitcoin surges alongside oil as BTC price finally decouples from the war narrative… until US markets opened

Bitcoin rose with crude oil while U.S. equities were closed, then reversed as the S&P 500 declined, leaving flows, oil, and Fed risk in conflict. Apr 29, 2026 · Liam ‘Akiba’ Wright

The challenge lies in durability. Once U.S. equities opened in that earlier session, Bitcoin reverted to the broader risk trade.

This remains the same unresolved test now. A BTC bounce below $80,000 would indicate that buyers are still active. A sustained move through the resistance zone would necessitate evidence that bonds, oil, or liquidity have ceased to work against the trade.

The next signal lies in the 10-year yield. If it retreats from the 4.4% to 4.5% range, Bitcoin’s demand narrative gains room to expand.

If it rises while oil remains high, BTC’s ceiling is likely to stay outside the crypto realm. The bond market would still be determining how much risk investors are willing to accept.

The post US Treasury yields spike to highest levels in a year adding new problem for Bitcoin liquidity appeared first on CryptoSlate.