Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

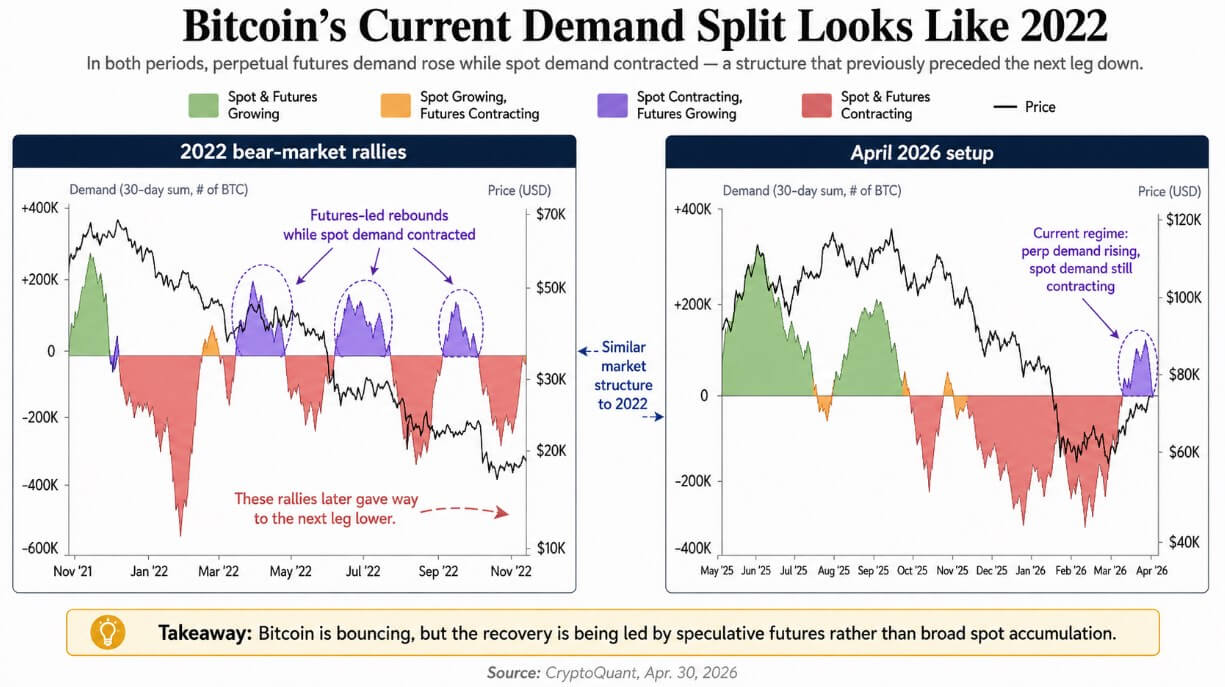

Bitcoin is mirroring a 2022 trend – and this time, we lack the purchasers for the subsequent developments.

CryptoQuant’s most recent report from April 30 indicates that perpetual futures are fueling Bitcoin’s rebound, while spot demand continues to decline. This mirrors the market dynamics observed during the bear market rallies of 2022, where leverage-driven recoveries ultimately led to further declines.

Spot purchases via exchanges, ETFs, or direct on-chain accumulation signify committed investment. Conversely, perpetual futures enable traders to gain directional exposure using borrowed funds, often at multiples of their collateral, without possessing the underlying asset.

When both demand types grow simultaneously, a rally tends to reinforce itself. However, when futures lead and spot lags, leveraged traders support the upward movement and may face forced exits if the price shifts against them.

The 2022 comparison

Multiple bear-market rallies in 2022 exhibited a similar pattern, with perpetual futures demand recovering prior to spot demand. Prices increased, and leveraged positions were unwound as spot buyers proved insufficient to absorb the selling pressure.

Although the rebounds appeared constructive, each ultimately transitioned into the next downward phase.

CryptoQuant’s charts illustrate Bitcoin’s demand distribution for April 2026, showing an increase in perpetual futures while spot contracts reflect the failed bear-market rally structure of 2022.

CryptoQuant’s charts illustrate Bitcoin’s demand distribution for April 2026, showing an increase in perpetual futures while spot contracts reflect the failed bear-market rally structure of 2022.

CryptoQuant’s chart indicates that Bitcoin’s current movement in April 2026 has returned to a state where spot contracts are diminishing while futures contracts are on the rise. This suggests that borrowed capital is re-emerging before actual cash demand, a condition that contributed to the fragility of the failed rallies in 2022.

The magnitude of today’s futures market amplifies that fragility. CoinGlass data revealed $47.64 billion in 24-hour Bitcoin futures volume compared to $4.07 billion in spot volume, resulting in a ratio of approximately 11.7x, with open interest around $54.19 billion as of April 30.

Perpetual futures can involve borrowed capital up to 50 times the collateral on certain platforms, meaning relatively minor price fluctuations can lead to significant forced liquidations.

With spot volume at $4 billion daily, a long-side flush can quickly test the market’s depth.

What the ETF data adds

Recent US spot Bitcoin ETF flows have further emphasized the market structure warning, as Farside Investors data indicates total outflows of $490.5 million between April 27 and April 29.

The ETF bid has become inconsistent precisely as futures positioning is increasing, while the long-term ETF outlook remains stable.

| Metric | Current read | Why it matters |

|---|---|---|

| BTC futures volume, 24h | $47.64B | Derivatives activity is dominating the market |

| BTC spot volume, 24h | $4.07B | Spot support is much smaller than futures activity |

| Futures/spot volume ratio | 11.7x | Indicates the rally is heavily leverage-driven |

| BTC open interest | $54.19B | Large leveraged position base that could unwind |

| US spot BTC ETF flows, Apr. 27–29 | -$490.5M | Recent ETF demand has turned inconsistent |

| IBIT cumulative net inflows | ~$65.2B | Long-term institutional demand remains robust |

| Total US spot BTC ETF cumulative inflows | ~$58.1B | The structural ETF bid is still positive overall |

Related Posts

IBIT alone represents approximately $65.2 billion in cumulative net inflows, while the entire US spot Bitcoin ETF sector totals around $58.1 billion, reflecting genuine structural buying that was absent in 2022.

From April 13 to April 29, IBIT absorbed about $1.47 billion in net inflows, maintaining the long-term institutional perspective. The immediate observation is that the ETF bid is not currently providing strong support for prices at a time when futures positioning would most benefit from it.

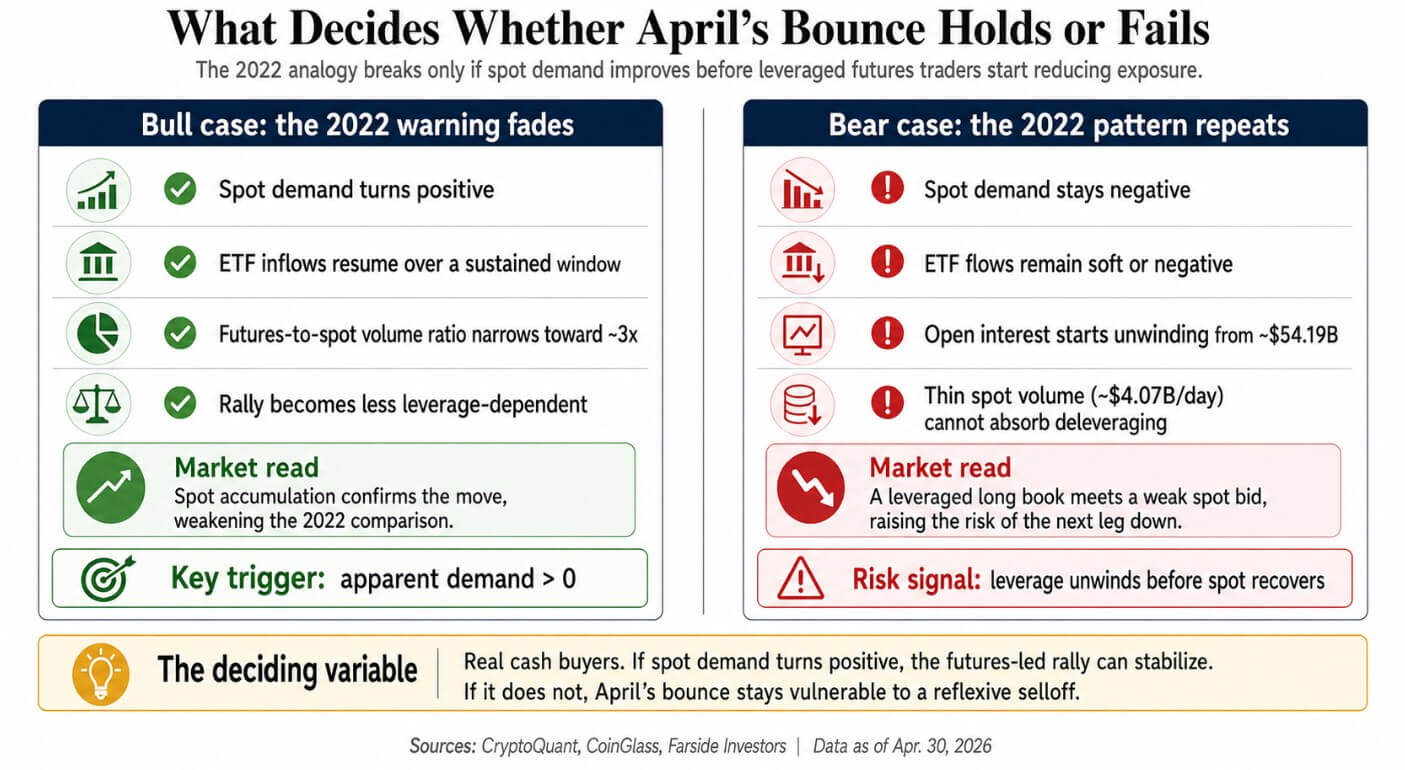

The bull case

The 2022 analogy falters when spot demand turns positive before leveraged traders begin to reduce exposure. CryptoQuant’s apparent demand measure rising above zero serves as a clear invalidation trigger, confirming that spot accumulation validates the futures-led movement.

The structural difference between 2026 and 2022 also provides a foundation for the bull case. Bitcoin now has regulated US spot ETFs, a more developed institutional framework, and a consistent corporate treasury demand that was not present four years ago.

Even CryptoQuant’s April 1 note, which highlighted significant contraction in spot demand, recognized that ETF and corporate buying had been accelerating.

The bull case relies on these buyers scaling up sufficiently to bring spot demand back into positive territory. If ETF inflows resume consistently and the futures-to-spot volume ratio narrows toward the broader market’s 3x average, the market structure argument weakens on its own terms.

A positive shift in spot demand serves as the bull trigger. Unwinding open interest against a thin spot volume of $4.07 billion daily poses the bear risk.

A positive shift in spot demand serves as the bull trigger. Unwinding open interest against a thin spot volume of $4.07 billion daily poses the bear risk.

The bear case

The bear case only requires leveraged traders to reduce exposure before spot demand turns positive. It necessitates that leveraged traders begin to decrease exposure prior to spot demand turning positive.

With $54 billion in open interest, even a partial unwind generates substantial absolute selling volume, and with spot volume at approximately $4 billion daily, the market lacks the depth to absorb a rapid unwind without a significant price drop.

This reflexivity amplifies the risk, as declining prices push leveraged longs toward liquidation, which in turn drives prices lower, creating a self-perpetuating cycle until spot demand strengthens enough to establish a floor.

Bear markets conclude when both spot and futures demand recover simultaneously.

The current situation shows futures recovering independently, and if this condition persists, Bitcoin has replicated the demand structure of the failed rallies in 2022. The forthcoming weeks of on-chain apparent demand and ETF flow trends will determine whether April’s rebound aligns with that pattern or diverges from it.

Either genuine cash buyers will step in to validate the futures-led movement, or the market will reveal the implications of a leveraged long position when the spot bid is too weak to maintain support.

The post Bitcoin is repeating a 2022 pattern – and this time we’re missing the buyers for what came next appeared first on CryptoSlate.