Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

The traditional Bitcoin strategy operated on the straightforward principle that when global M2 increases, capital tends to flow into risk assets, with Bitcoin capturing a significant portion of that influx.

This correlation fueled the bull market of 2020-2021, and throughout much of 2024, crypto Twitter focused on M2 overlays as evidence that the next upward movement was on the horizon.

Currently, while global M2 has been on the rise, Bitcoin has continued to lag behind.

Related Reading

Related Reading

Bitcoin breaks from M2 money supply as dollar strength overrides global cash growth

Liquidity continues to grow, but the rapidly strengthening dollar is tightening conditions before it impacts Bitcoin. Apr 1, 2026 · Gino Matos

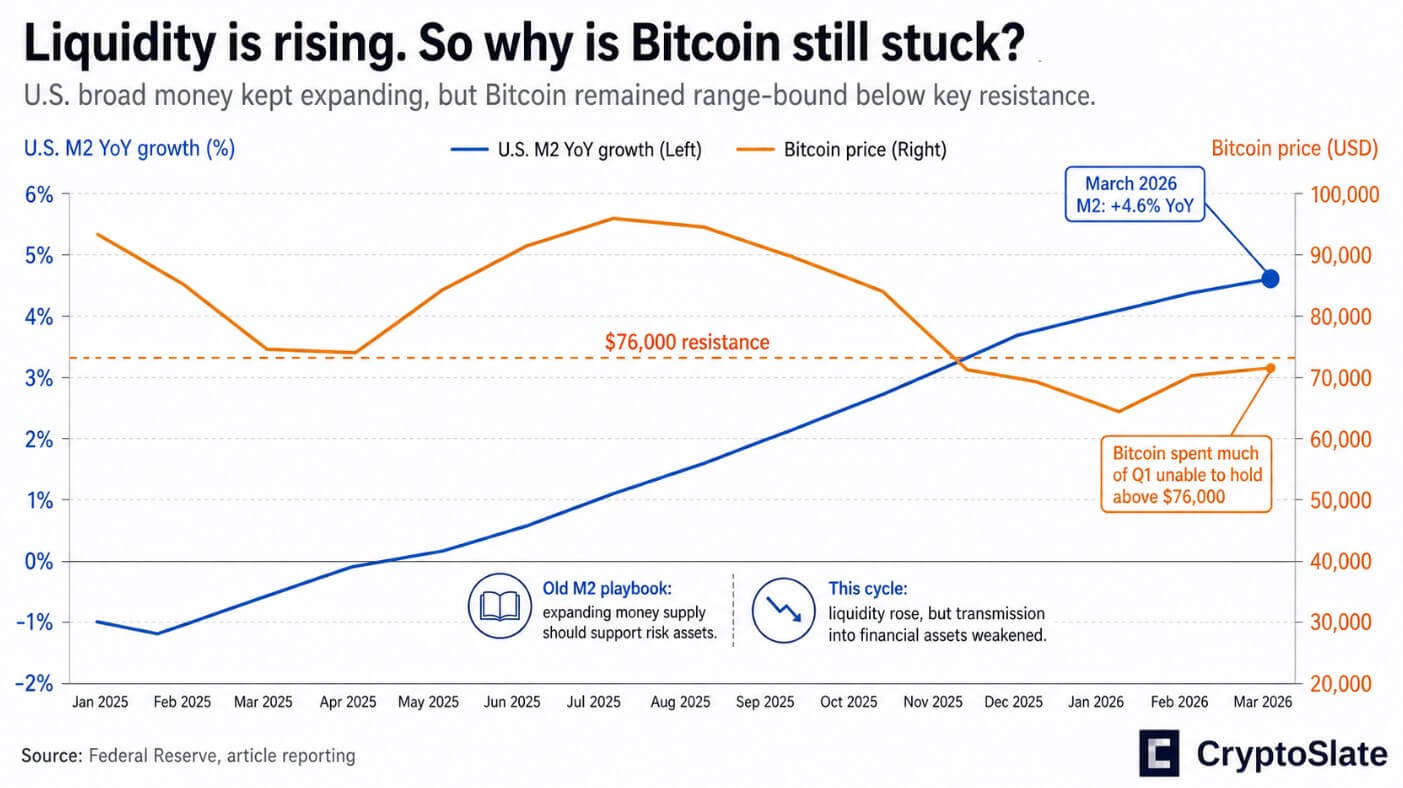

In March 2026, US M2 reached nearly $22.7 trillion, reflecting a 4.6% increase year over year, while Bitcoin struggled to maintain a position above $76,000, a threshold identified by Real Vision’s chief crypto analyst Jamie Coutts as significant resistance during an episode of CryptoQuant’s Unbiased podcast.

Coutts noted that the mechanism of transmission has shifted, as the type of liquidity now dictates whether the expansion actually reaches financial assets.

In the post-2008 quantitative easing era, the Federal Reserve directly purchased assets, inundating the system with bank reserves that predominantly flowed into equities, credit, and eventually crypto.

At present, Treasury issuance, reserve management, fluctuations in cash balances, and the creation of bank credit have supplanted the central bank’s balance-sheet influx.

US M2 grew 4.6% year over year by March 2026 while Bitcoin failed to hold above $76,000 resistance.

US M2 grew 4.6% year over year by March 2026 while Bitcoin failed to hold above $76,000 resistance.

The plumbing problem

The US public debt concluded the fourth quarter of 2025 at over $38.5 trillion, marking a 6.3% increase year over year. In contrast, US M2 expanded by 4.6% during the same timeframe.

According to the most basic available figures, debt is outpacing broad money by nearly two percentage points annually. The current debt stock is approximately 1.70 times the total M2, a ratio without modern precedent in a supposedly accommodating monetary environment.

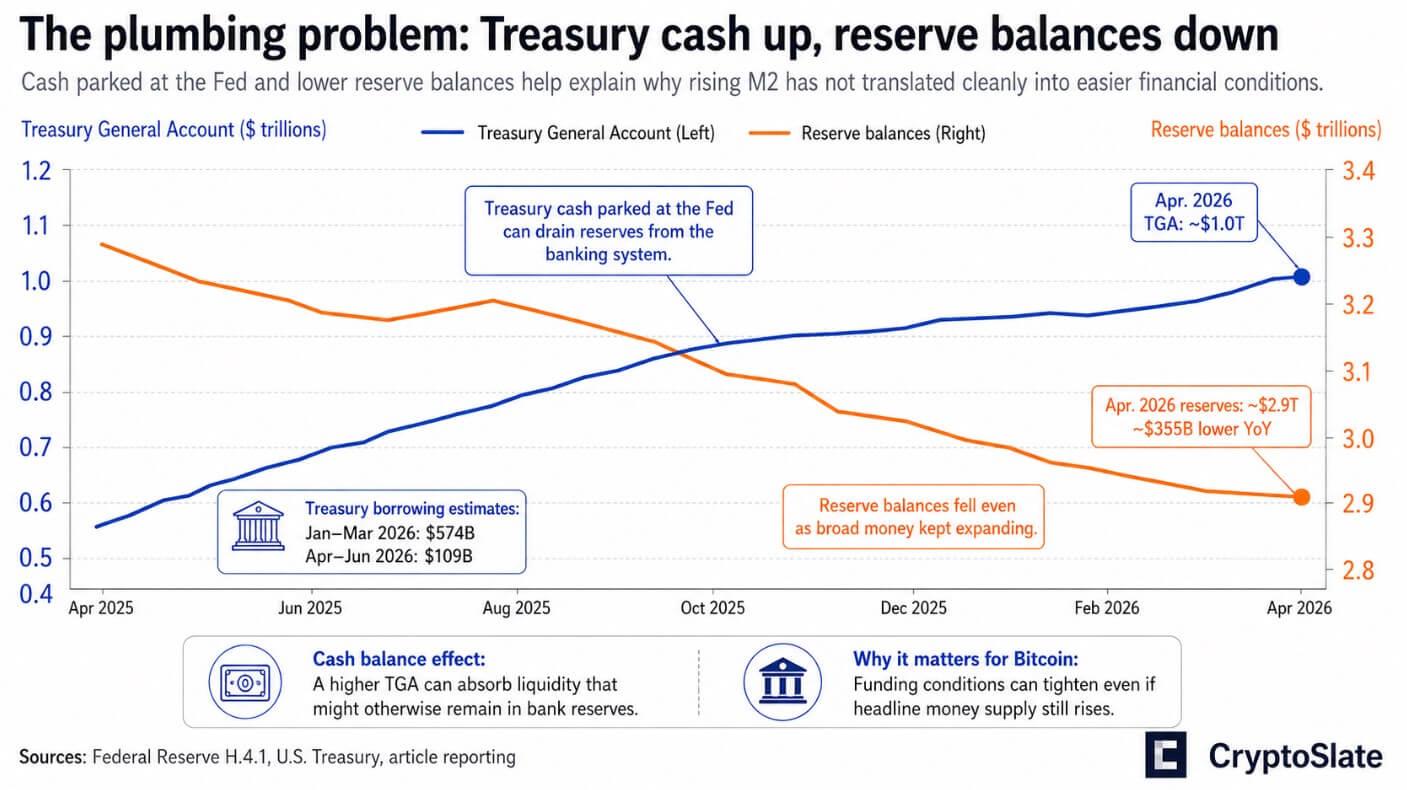

The Treasury’s own borrowing projections anticipated $574 billion in net marketable debt for the January-March 2026 quarter and an additional $109 billion for April-June, while maintaining a cash balance exceeding $1 trillion.

The Treasury General Account, held at the Federal Reserve, contained about $1 trillion according to the latest H.4.1 data. Cash held at the Fed drains reserves from the banking system even as M2 continues to rise.

Reserve balances decreased to around $2.9 trillion in the Fed’s April 22 release, down approximately $355 billion from the previous year.

Broad money appears to expand on paper, while the mechanisms that actually transfer reserves into financial markets are tightening marginally.

The Treasury General Account climbed to roughly $1.0 trillion in April 2026 as reserve balances fell approximately $355 billion year over year to $2.9 trillion.

The Treasury General Account climbed to roughly $1.0 trillion in April 2026 as reserve balances fell approximately $355 billion year over year to $2.9 trillion.

Bank credit continues to grow, with commercial loans and leases reaching about $13.7 trillion by mid-April, while this credit seems to be directed toward real-economy absorption.

During the April 29 FOMC meeting, the policy rate was maintained at 3.5%-3.75%, with total assets remaining around $6.7 trillion. Officials cited inflation as their main constraint, with no balance sheet expansion planned.

Related Posts

Why the old chart broke

Coutts contended on the podcast that Bitcoin’s underperformance is indicative of plumbing friction.

The decline from late 2024 into early 2025 was influenced by tightening reserve conditions in the fourth quarter, Treasury dynamics related to a government shutdown, derivatives-driven deleveraging, and the increasing influence of ETF and derivatives markets on Bitcoin’s price structure.

None of these factors are reflected in a global M2 overlay, as they represent characteristics of a financial system where Treasury supply, reserve management, and funding conditions have become the primary battleground.

Gold provides the clearest cross-market confirmation. Central banks acquired 244 tonnes of gold in the first quarter, a 3% year-over-year increase, with total gold demand reaching 1,231 tonnes and a record $193 billion in value, according to the World Gold Council.

Official institutions are hedging against sovereign debt credibility on a large scale, but they are doing so through gold, an asset that central banks can legally hold.

The IMF’s latest Fiscal Monitor indicated that global public debt is projected to reach 100% of GDP by 2029, with the US and China contributing significantly to this acceleration.

The Congressional Budget Office forecasts a $1.9 trillion federal deficit in FY2026, with public debt increasing from 101% of GDP to 120% by 2036, creating a structural supply overhang that will continue to compete with risk appetite for the same pool of reserves and capital.

Related Reading

Related Reading

Central bankers call crypto a “shadow” financial system as Binance breaks over $1 trillion trading volume

Binance’s early-year trading surge illustrates how market power is consolidating around platforms that now integrate trading, custody, leverage, and yield. Apr 25, 2026 · Oluwapelumi Adejumo

Two outcomes

In the optimistic scenario, inflation decreases toward the Fed’s projected trajectory, the Treasury cash balance diminishes, reserves are replenished, and bank credit continues to grow without triggering a growth scare.

In this context, the “liquidity is still expanding” thesis regains momentum. Bitcoin could quickly re-rate as the mismatch between debt and liquidity prevents the tightening of financial conditions at the margin.

Coutts considers the $60,000 range as a value floor and estimates that the likelihood of the cycle low already being in is better than 50-50.

Conversely, in the pessimistic scenario, debt issuance remains substantial, inflation remains persistent, Treasury funding pressures continue, and the Fed cannot ease without reigniting the inflation it has worked to suppress for two years.

In this case, Bitcoin would behave less like a monetary hedge and more like a high-beta risk asset susceptible to rates, funding conditions, and periodic deleveraging.

The April flash PMI from S&P Global already indicated growth running close to a 1% annualized rate. This fragile expansion does not need to enter a recession to create the kind of funding shocks that impact Bitcoin most severely.

| Factor | Bull case | Bear case |

|---|---|---|

| Inflation | Cools toward the Fed’s projected path | Stays sticky enough to keep policymakers cautious |

| Treasury cash balance | Declines, reducing reserve drain | Stays elevated, continuing to absorb liquidity |

| Reserve balances | Rebuild from current levels | Stay tight or fall further |

| Debt issuance | Remains manageable relative to liquidity growth | Stays heavy and outpaces liquidity growth |

| Fed stance | Can ease or soften without reigniting inflation | Cannot ease meaningfully without risking another inflation wave |

| Bank credit | Keeps expanding without a growth scare | Expands weakly or is offset by tighter funding conditions |

| Financial conditions | Loosen at the margin | Stay restrictive and prone to stress episodes |

| Market plumbing | Treasury supply and reserves stop acting as a headwind | Treasury funding strain and reserve friction remain the main battleground |

| Bitcoin behavior | Re-rates higher as the liquidity thesis regains traction; $60,000 holds as a value floor | Trades like a high-beta risk asset, with sharp drawdowns, failed breakouts, and possible retests of lower support |

| Investor takeaway | Expanding liquidity is enough to absorb debt and support risk assets | Liquidity may still be growing, but not fast enough to offset debt, reserves, and Treasury supply |

Coutts distinguishes the long-term monetary rationale for Bitcoin from the medium-term price behavior that is actually influenced by reserve flows.

In a scenario where debt surpasses broad money, where the Fed operates from a restrictive baseline, and where Treasury cash balances drain reserves even as M2 increases, the critical question for investors is whether that expansion is sufficiently rapid to absorb debt, reserves, and Treasury supply concurrently.

Until debt and reserve conditions shift decisively in Bitcoin’s favor, the asset will continue to experience the sharp declines and frustrating consolidations that characterize a market caught between a constructive long-term thesis and a tighter-than-anticipated short-term funding environment.

The post Bitcoin’s next risk is hiding in the gap between debt and liquidity appeared first on CryptoSlate.