Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

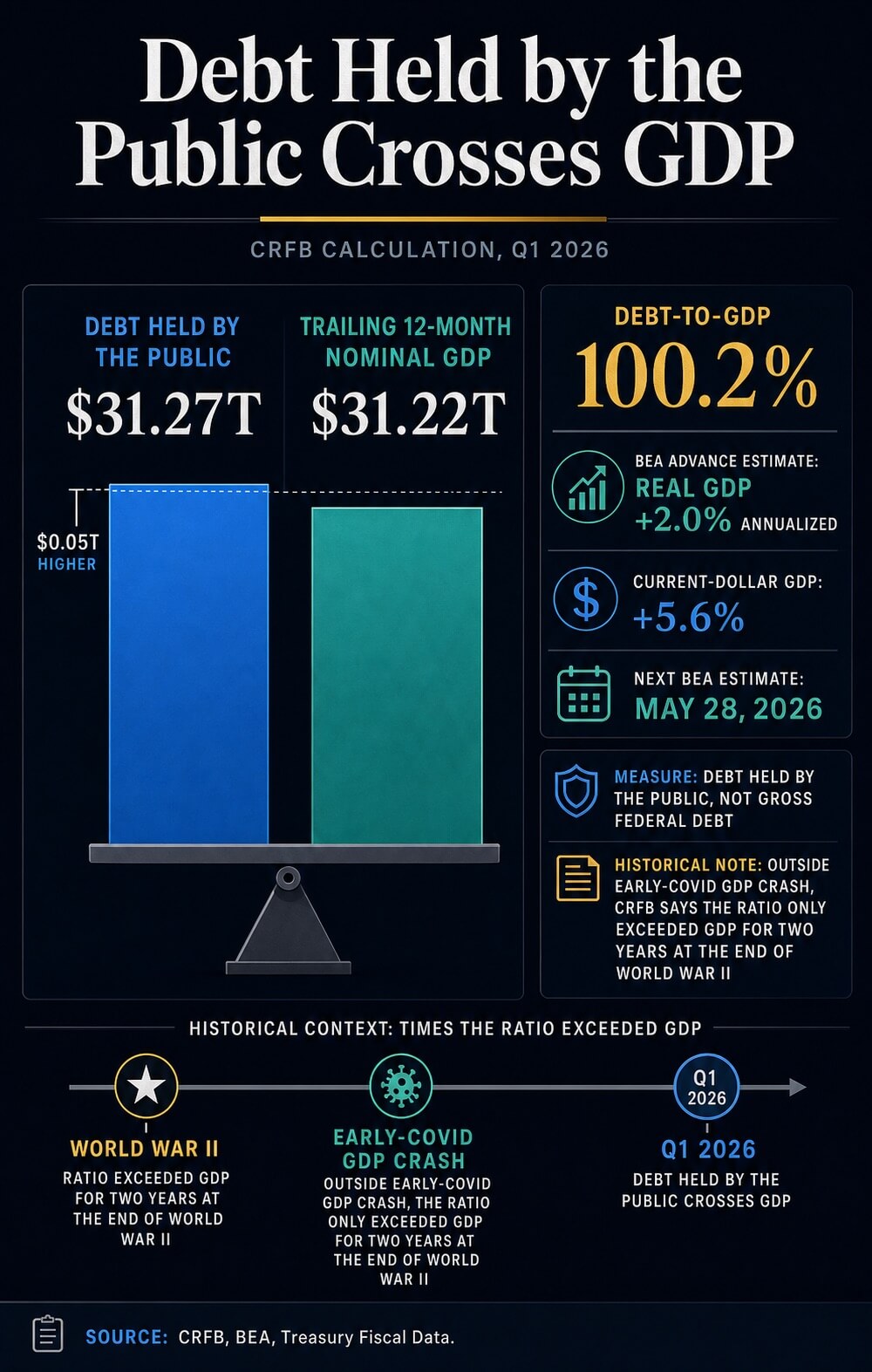

America’s debt of $31.27 trillion surpasses its GDP, subtly strengthening the argument for Bitcoin.

The public debt of the United States has surpassed the size of the U.S. economy, according to calculations from the Committee for a Responsible Federal Budget (CRFB), providing a tangible fiscal benchmark for Bitcoin’s hard-money argument as investors consider limited assets in light of Washington’s debt trajectory.

CRFB reported that public debt reached $31.27 trillion by the end of the first quarter of 2026, compared to a trailing 12-month nominal GDP of $31.22 trillion. This results in a ratio of 100.2%, based on the Bureau of Economic Analysis’s preliminary estimate for first-quarter output.

For Bitcoin, this threshold transforms a theoretical scarcity discussion into a pressing macroeconomic issue: whether a fixed-supply, non-sovereign asset becomes more appealing as confidence in sovereign balance sheets declines. Debt serves as the narrative input, while liquidity, interest rates, ETF demand, and risk appetite act as the transmission mechanisms.

The increase above 100% of GDP bolsters the argument investors can make for Bitcoin as a scarce form of monetary insurance. However, it remains uncertain whether these investors will increase their exposure while Treasury yields, reserve conditions, and volatility continue to influence risk pricing.

Implications of the debt threshold

CRFB’s analysis focuses on debt held by the public, which refers to federal debt owed to external investors and other non-government entities. This metric carries a different market significance than the total public debt outstanding, which also encompasses intragovernmental holdings.

This distinction is crucial because the Bitcoin comparison is valid only if the fiscal metric is well-defined. Treasury’s Debt to the Penny data, including its March 31 API record, differentiates between debt held by the public and intragovernmental holdings as well as total public debt outstanding.

The benchmark relies on the public-debt measure rather than the broader figures often referenced in political discussions.

CRFB also contextualized the threshold historically. Aside from the brief GDP decline at the onset of COVID-19, it noted that debt only exceeded GDP for two years at the conclusion of World War II.

A debt ratio approaching wartime levels alters the terminology investors use regarding fiscal credibility, even as the U.S. Treasury market remains the focal point of global collateral.

Attention must also be paid to the GDP aspect of the ratio. The BEA’s first-quarter release was a preliminary estimate.

This indicated real GDP growing at an annualized rate of 2.0% and current-dollar GDP increasing by 5.6%, but the next estimate is set for May 28. Consequently, the exact ratio may fluctuate.

The fiscal signal remains sufficiently clear for market discussions, while the precise denominator is still tentative.

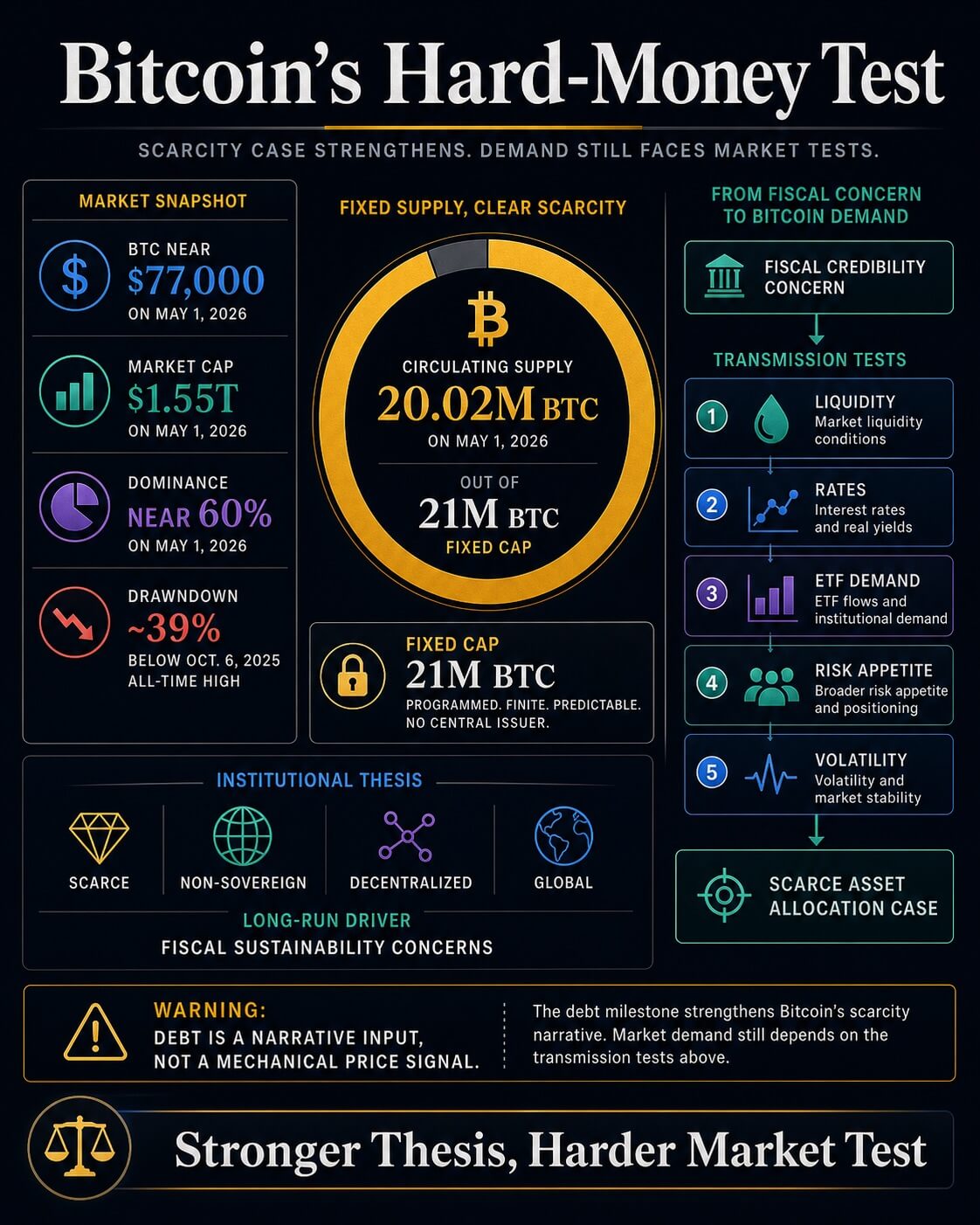

Bitcoin is relevant to this conversation because its supply schedule contrasts with fiscal expansion. CryptoSlate’s Bitcoin market page indicated approximately 20.02 million BTC in circulation on May 1, 2026, against a maximum supply of 21 million.

This fixed limit represents the fundamental monetary contrast with a fiscal system capable of issuing additional debt.

BlackRock has articulated the institutional perspective on this argument. In its Bitcoin diversifier paper, the asset manager characterized Bitcoin as scarce, non-sovereign, decentralized, and global.

It also noted that long-term adoption could be influenced by concerns regarding monetary stability, geopolitical stability, U.S. fiscal sustainability, and U.S. political stability.

This fiscal context positions CRFB’s debt marker within Bitcoin’s investment rationale. Allocators now have a contemporary U.S. reference point for a thesis that might otherwise appear abstract.

The premise is straightforward: if sovereign debt continues to grow at a faster rate than the economy, a credibly scarce settlement asset garners more attention in discussions about monetary hedges.

CryptoSlate’s broader market dashboard and Bitcoin page reported BTC near $77,000 on May 1, with a market capitalization of approximately $1.55 trillion, dominance around 60%, and a price roughly 39% lower than its all-time high on October 6, 2025.

A scarce asset can still behave like a risk asset when liquidity tightens.

Liquidity remains the determining factor

Recent coverage from CryptoSlate illustrates why the debt milestone must be distinguished from short-term price movements. An analysis of debt and liquidity suggested that U.S. debt growth, Treasury issuance, reserve balances, and bank credit conditions can constrict the mechanisms that facilitate liquidity into risk assets, even when overall money supply is increasing.

This perspective is significant for Bitcoin, as the asset occupies a position at the crossroads of two distinct trades. In the long term, it can be acquired as monetary insurance against fiscal and currency risks.

In the medium term, it continues to respond to the cost of capital, leverage, ETF flows, and the yield levels available on Treasuries.

Related Posts

A separate CryptoSlate article on Treasury yields and Bitcoin liquidity reinforced this point through the rates channel. Elevated long-end yields increase the threshold for assets that do not provide a coupon or dividend.

Bitcoin can maintain a stronger monetary narrative while still facing a more challenging comparison against Treasury income.

Related Reading

Related Reading

US Treasury yields spike to highest levels in a year adding new problem for Bitcoin liquidity

Bitcoin’s next move now runs through Treasury yields, oil pressure, and Fed liquidity as markets test whether risk demand can hold near resistance. Apr 30, 2026 · Liam ‘Akiba’ Wright

This results in a two-tier market. The debt-to-GDP threshold enhances the macro environment for Bitcoin.

The funding landscape determines whether this environment translates into actual demand. Investors relying on the milestone as a price indicator require evidence from flows, yields, reserves, and volatility before the allocation case evolves beyond a narrative enhancement.

Related Reading

Related Reading

Bitcoin’s next risk is hiding in the gap between debt and liquidity

US debt is growing faster than M2, leaving Bitcoin trapped between a bullish liquidity thesis and tighter market plumbing that keeps capping risk. Apr 30, 2026 · Gino Matos

| Evidence layer | What it supports | What remains open |

|---|---|---|

| CRFB debt-to-GDP marker | Public debt has crossed GDP on CRFB’s calculation, reviving a World War II-era comparison. | The exact ratio can shift as GDP estimates revise. |

| CBO baseline | Debt held by the public is projected to rise from 101% of GDP in 2026 to 120% in 2036. | Faster nominal GDP growth or policy changes could alter the path. |

| BlackRock Bitcoin thesis | Fiscal sustainability concerns fit the institutional case for a scarce, non-sovereign asset. | Adoption logic and short-term price behavior remain separate tests. |

| CryptoSlate market context | BTC still trades with liquidity, yields, ETF demand, and volatility in view. | A debt milestone alone leaves flow confirmation unresolved. |

Two potential paths for the thesis

The Congressional Budget Office’s February outlook maintains focus on fiscal pressures. It anticipates that debt held by the public will increase from 101% of GDP in 2026 to 120% in 2036, surpassing the 106% peak recorded in 1946.

It also forecasts widening deficits, with rising net interest costs contributing significantly to the increase.

This trajectory provides Bitcoin’s hard-money thesis with a robust macro backdrop. If deficits remain substantial, interest costs escalate, and investors become more attuned to Treasury supply, demand for assets outside of sovereign issuance may rise.

In this scenario, the debt milestone symbolizes the constraint Bitcoin was designed to operate beyond.

The CBO’s own uncertainty analysis introduces the necessary caution. In a February follow-up regarding how outcomes could diverge from its baseline, the CBO indicated that economic and budgetary results could fall above or below its central estimate, including scenarios with faster nominal GDP growth.

The fiscal trajectory is significant, but it remains a projected path rather than a definitive outcome.

CryptoSlate’s previous coverage has been leading toward the same examination from various perspectives. A February analysis of the decade-long debt trajectory framed the issue through term premium, dollar vulnerability, and Bitcoin’s role as a hard asset.

A November article assessed U.S. debt in BTC terms, illustrating how swiftly fiscal expansion can outpace Bitcoin’s issuance schedule. CRFB’s new marker alters the timing: the ratio has now crossed the threshold.

Related Reading

Related Reading

US debt now worth 368M BTC: American debt machine adds a century of new Bitcoin supply this year alone

Mapping US debt in BTC exposes a fiscal expansion no blockchain would want to keep up with. Nov 14, 2025 · Liam ‘Akiba’ Wright

This leaves Bitcoin with two probable outcomes. In the favorable scenario, inflation subsides, reserve conditions improve, Treasury supply becomes more manageable, and the debt milestone reinforces the case for a modest allocation to scarce monetary assets.

In the unfavorable scenario, issuance remains high, yields stay elevated, and Bitcoin continues to trade as a high-beta liquidity asset despite the stronger long-term narrative.

The crossing of U.S. public debt over GDP provides Bitcoin’s scarcity thesis with a more defined macro anchor.

It supports the notion that some investors will persist in seeking non-sovereign monetary assets as fiscal ratios deteriorate. However, it leaves the more challenging market validation ahead: whether liquidity, rates, and flows will align sufficiently for that thesis to evolve into sustained demand rather than merely another macro slogan.

The post America’s $31.27 trillion in debt now exceeds GDP – silently reinforces the case for Bitcoin appeared first on CryptoSlate.