Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

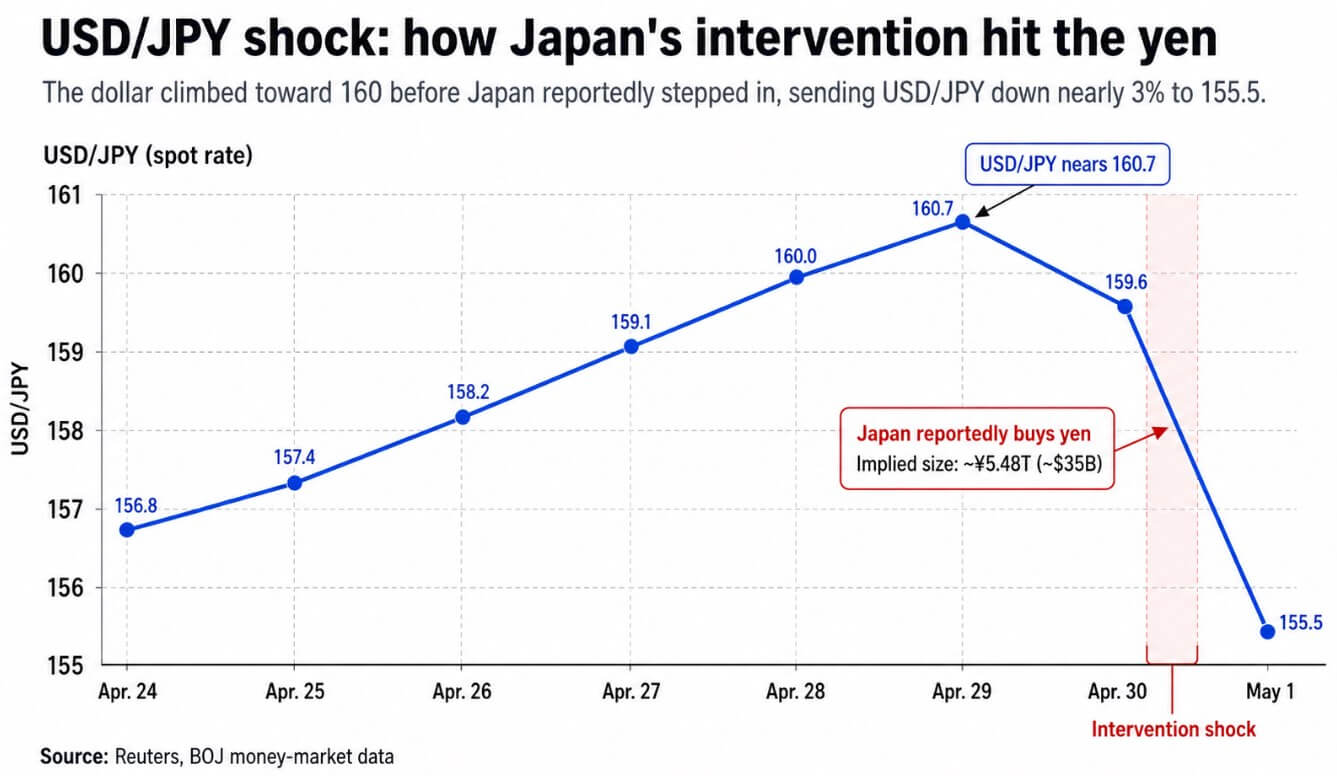

Japan has reportedly entered the currency market with approximately $35 billion in yen purchases, causing the dollar to decline nearly 3% to 155.5.

Data from the Bank of Japan (BOJ) regarding money markets suggests that this figure is accurate. Once confirmed by the Ministry of Finance’s monthly report, this would mark Japan’s first official intervention to support the yen in nearly two years and the second-largest in history.

The BOJ’s April forecast anticipates that the consumer price index (CPI) excluding fresh food will be between 2.5% and 3.0% in fiscal 2026, with economists predicting a resurgence in inflation as rising oil prices and yen depreciation increase import expenses.

Statistics indicate that 95% of Japan’s crude oil is transported through the Strait of Hormuz, and the BOJ’s baseline scenario expects Dubai crude prices to trend between $70 and $80, assuming no significant supply disruptions occur.

Tokyo’s political tolerance for rising import inflation while the yen depreciates has limits, which were exceeded this week.

The USD/JPY reached a peak of 160.7 on April 29 before Japan’s reported $35 billion intervention reduced the pair to 155.5.

The USD/JPY reached a peak of 160.7 on April 29 before Japan’s reported $35 billion intervention reduced the pair to 155.5.

On April 28, the BOJ maintained its policy rate at 0.75%, with three board members dissenting in favor of a 1% rate. The Federal Reserve also kept its policy rate steady at 3.50%-3.75% on April 29.

This short-rate reality of approximately 275 to 300 basis points is the fundamental reason the carry trade continues to rebuild. Yen borrowing costs remain low compared to global standards, and the yield spread to U.S. rates makes it appealing to invest that capital in higher-yielding assets.

Intervention without rate alignment merely provides temporary relief. According to Reuters, 65% of economists surveyed on April 16 anticipate the BOJ will reach a 1.0% rate by the end of June 2026, with additional hikes expected through 2027.

Why the yen is everyone's problem

Data from the Bank for International Settlements (BIS) from its 2025 triennial survey indicates that the yen constituted 16.8% of all foreign exchange transactions globally.

Another BIS analysis regarding the August 2024 episode estimated yen-funded carry trades at around $250 billion prior to that unwind, while UBS approximated the total near $500 billion, with only about half of that unwound at the time.

A separate BOJ report highlighted that yen liabilities financing balance sheet expansion are primarily driven by hedge funds and financial intermediaries that hold assets far removed from Japanese currency markets.

CFTC positioning data from April 21 reveals that leveraged funds in CME yen futures held 80,220 long contracts against 148,717 short contracts, with gross shorts increasing by over 16,000 week-over-week.

When the yen unexpectedly strengthens, those short positions require coverage, and the assets funded by those trades need to be reduced.

| Metric | Bank of Japan | Federal Reserve | Why it matters for the carry trade |

|---|---|---|---|

| Policy rate | 0.75% | 3.50%–3.75% | The significant gap keeps yen funding inexpensive and U.S. assets relatively appealing |

| Latest policy decision date | Apr. 28, 2026 | Apr. 29, 2026 | Indicates the rate divergence is current, not historical |

| Current short-rate gap | Approximately 275–300 bps | This spread is the primary mechanical driver of yen-funded carry trades | |

| Policy bias | Three BOJ board members dissented in favor of a 1.0% rate | Fed maintained its position | Indicates Japan may be gradually moving toward tighter policy, but not quickly enough to eliminate the spread |

| Market expectation | Reuters poll: 65% of economists foresee BOJ at 1.0% by end-June 2026 | No comparable immediate shift in the draft | A BOJ rate hike could narrow the carry spread and render short-yen positions less attractive |

| Carry-trade implication | Low-cost funding currency | Higher-yield destination market | Investors can borrow cheaply in yen and pursue better returns elsewhere |

| Article takeaway | Intervention can disrupt FX markets, but without rate convergence it merely provides temporary relief | Higher U.S. yields sustain the carry incentive | Clarifies why yen weakness continues to rebuild and why a sudden yen rebound can pressure risk assets, including Bitcoin |

BIS data also indicates that foreign-currency credit denominated in yen decreased by 4.9% during 2025, suggesting that the carry complex may already be somewhat smaller, which implies that the mechanical force of any unwind is diminished.

Related Posts

Bitcoin’s sensitivity is linked to global leverage, as the balance sheets, margin calls, and risk appetites of the same macro funds simultaneously short yen and long higher-yielding assets.

The BIS’s August 2024 review found that procyclical deleveraging and margin increases intensified the shock across risk assets, with Bitcoin dropping 13% during the sell-off.

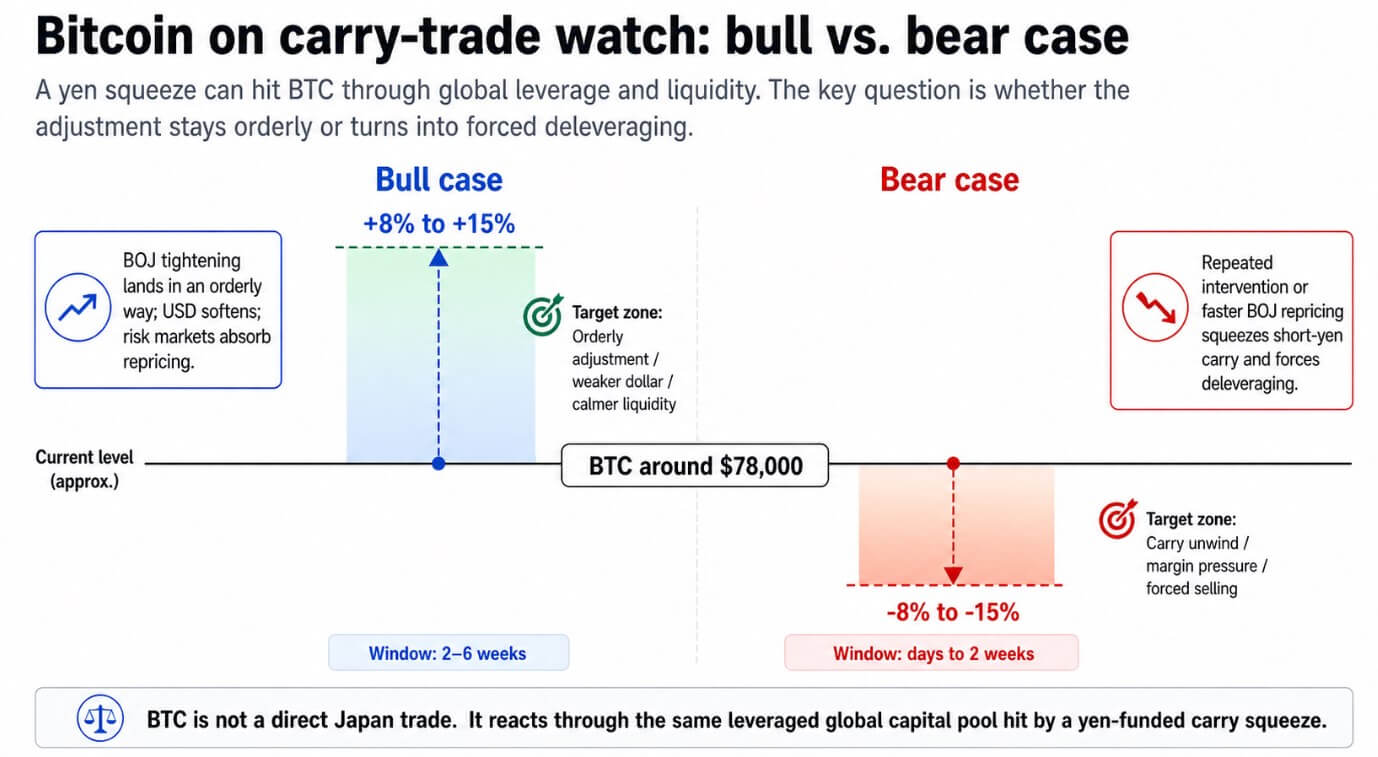

Bitcoin was trading in the $78,000 range on May 1, reaching an intraday peak near $79,000. A sudden yen squeeze compels leveraged macro portfolios to reduce gross exposure, and traders may sell Bitcoin due to its liquidity and the need for leveraged accounts to quickly raise cash.

The bull case

If the BOJ’s three dissenters are correct and a rate hike occurs in June, it will initiate a credible tightening cycle that compresses the carry spread, makes new short-yen positions less appealing, and results in a weaker dollar.

The intervention has already caused the dollar index to decline by 0.8%, with the euro, pound, and Swiss franc all appreciating. This broad dollar weakening historically creates a favorable environment for Bitcoin, which tends to follow global dollar liquidity trends.

In a smooth adjustment where the BOJ’s June hike occurs without triggering a chaotic unwind, USD/JPY could stabilize within a tighter range, allowing global risk markets to absorb the repricing without triggering cascading margin calls.

Bitcoin may navigate its initial volatility and revert to the weaker-dollar, easier-liquidity environment that fueled its rally through early 2024.

Coinbase Research’s outlook for the second quarter indicated that 75% of institutional respondents consider BTC undervalued at current levels, suggesting that buying interest may emerge following any short-term disruption.

A recovery of 8% to 15% from current levels over a two-to-six-week timeframe is a plausible scenario in this context.

The bear case

Repeated interventions or a sharper adjustment of BOJ policy expectations could pressure the short-yen trade with sufficient intensity to necessitate VAR and margin reductions across macro portfolios simultaneously.

In such a scenario, traders may sell Bitcoin due to its liquidity and the pressure on leveraged accounts.

The August 2024 situation serves as a reference point, with approximately a 15% decline occurring over a few days, driven by similar carry mechanics and exacerbated by forced selling.

A yen-funded carry squeeze could expose Bitcoin to an 8–15% decline within days, or an 8–15% recovery over two to six weeks if the adjustment remains orderly.

A yen-funded carry squeeze could expose Bitcoin to an 8–15% decline within days, or an 8–15% recovery over two to six weeks if the adjustment remains orderly.

Bitcoin’s position at the $78,000 level offers less buffer for holders with significant embedded gains who may be reluctant to endure a downturn.

A decline of 8% to 15% aligns with historical trends when interventions occur without policy support.

The post Japan has moved to save the yen again, and Bitcoin traders may pay the price appeared first on CryptoSlate.