Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

On what is expected to be a momentous day for Bitcoin, I spent the morning reviewing historical data to assess the significance of the first Gold ETF at that time. Numerous analysts, including our own, have discussed how Gold ETFs transformed the commodity landscape, resulting in substantial gains over the following two decades. But what was the actual experience back then? Did gold surge immediately, or did it require time? Let’s explore.

First, we will examine the timeline of the relevant exchange-traded products.

On Nov. 18, 2004, State Street Corporation introduced SPDR Gold Shares (GLD), amassing $114,920,000 in assets under management at launch and reaching $1 billion within its first three trading days.

On Oct. 19, 2021, ProShares launched the ProShares Bitcoin Strategy ETF (BITO), which saw $570 million in inflows on its first day, achieving $1 billion in assets the following day.

On Jan. 11, 2024, eleven spot Bitcoin ETFs are set to debut in the U.S. with $115.88 million under management through the sponsors’ seed funds. This indicates that once they receive $115 million in inflows, issuers such as BlackRock, Ark, VanEck, and others will purchase Bitcoin from the open market via Coinbase and Gemini, similar to other investors.

Therefore, prior to the commencement of trading (excluding Grayscale, which is converting its trust* into an ETF that already has $28.58 billion in AUM), the total assets of the spot Bitcoin ETFs will exceed GLD’s day one trading. Including Grayscale, spot Bitcoin ETFs will have more assets under management than gold did during its first five years. GLD did not reach $29 billion in AUM until Feb. 12, 2009.

However, it is important to note that it was not the sole gold ETF at that time. BlackRock launched its iShares® COMEX® Gold Trust in 2005. Together with GLD, gold ETFs achieved a comparable AUM around Feb. 10, 2009, with IAU securing $2 billion in assets by the end of Q1 2009.

By the conclusion of 2009, three gold-backed ETFs were available for trading in the United States: ETFS Physical Swiss Gold Shares, SPDR Gold Shares, and iShares Comex Gold Trust.

| Company | Seed Investment ($M) |

|---|---|

| Bitwise | 20 |

| VanEck | 72.50 |

| Valkyrie | 0.52 |

| Franklin Templeton | 2.60 |

| WisdomTree | 4.95 |

| Invesco Galaxy | 4.85 |

| BlackRock | 10 |

| Ark | 0.46 |

| Grayscale | 2,858 |

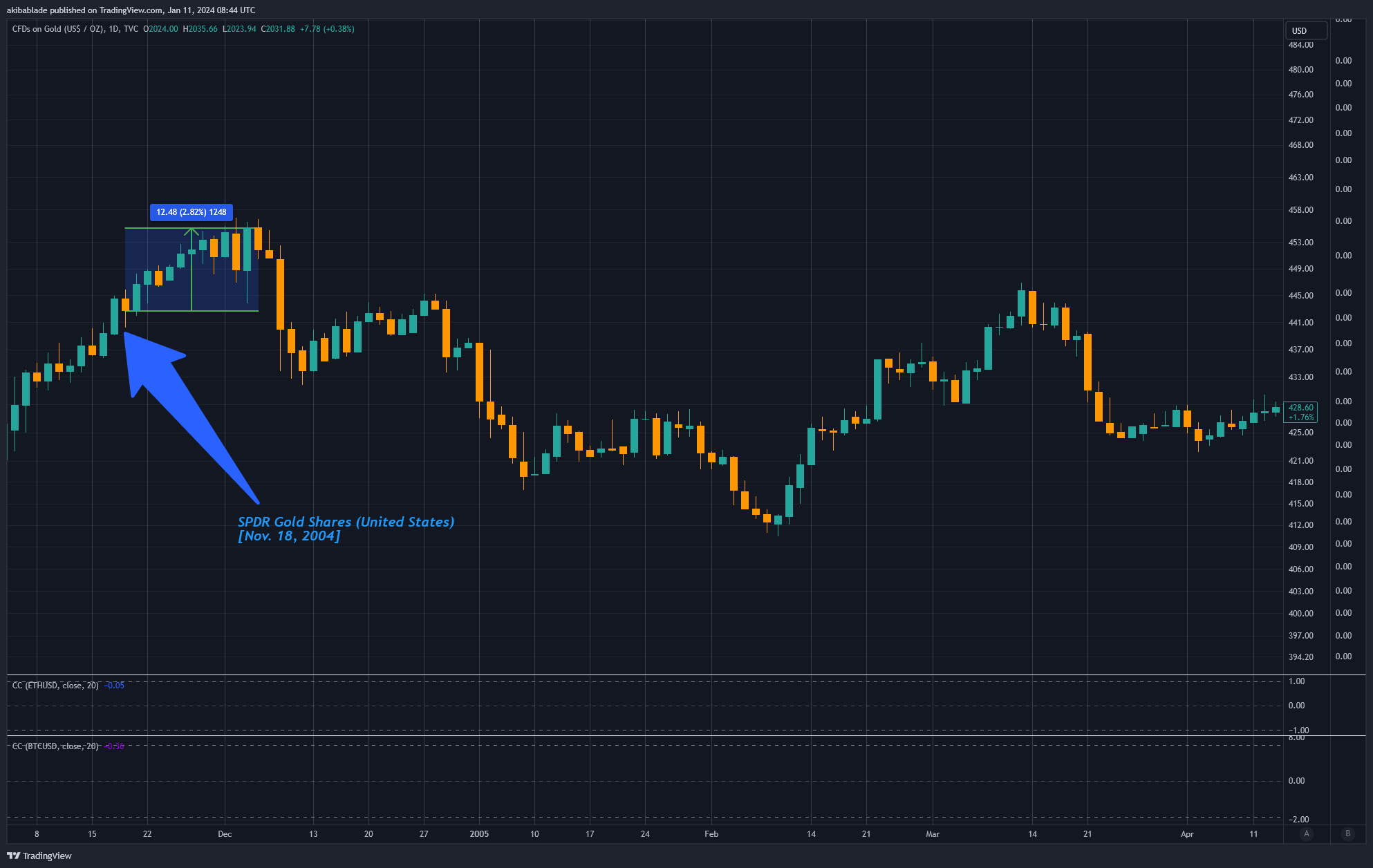

How did GLD trade at launch?

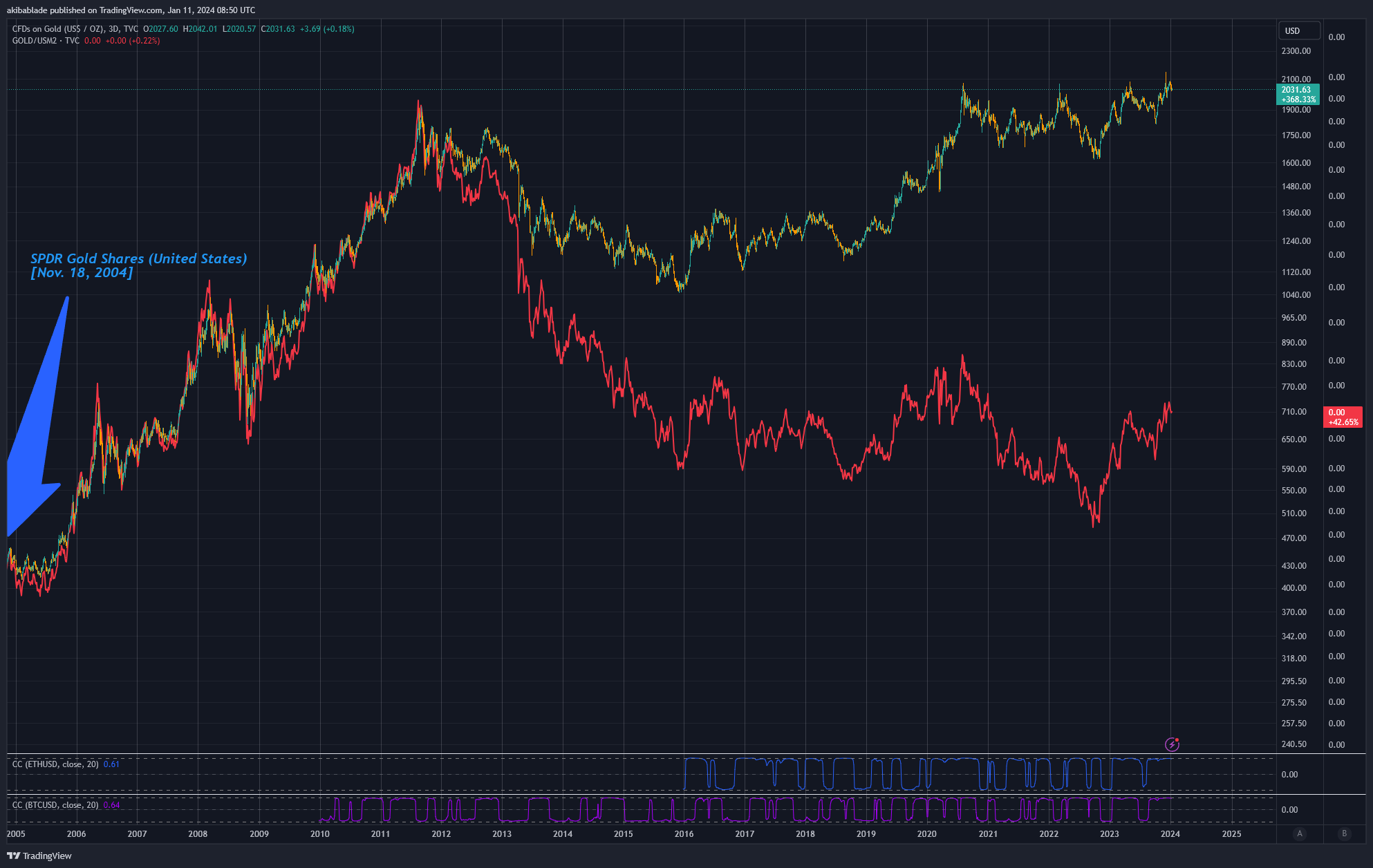

The first gold ETF was introduced in the U.S. on Nov. 18, 2004, and within 12 days, the price of gold increased by just 2.82%.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

This represented a sixteen-year peak for gold, which had not reached $453 per ounce since May 1988. However, it was not an all-time high. In fact, it would take another four years for that to happen.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

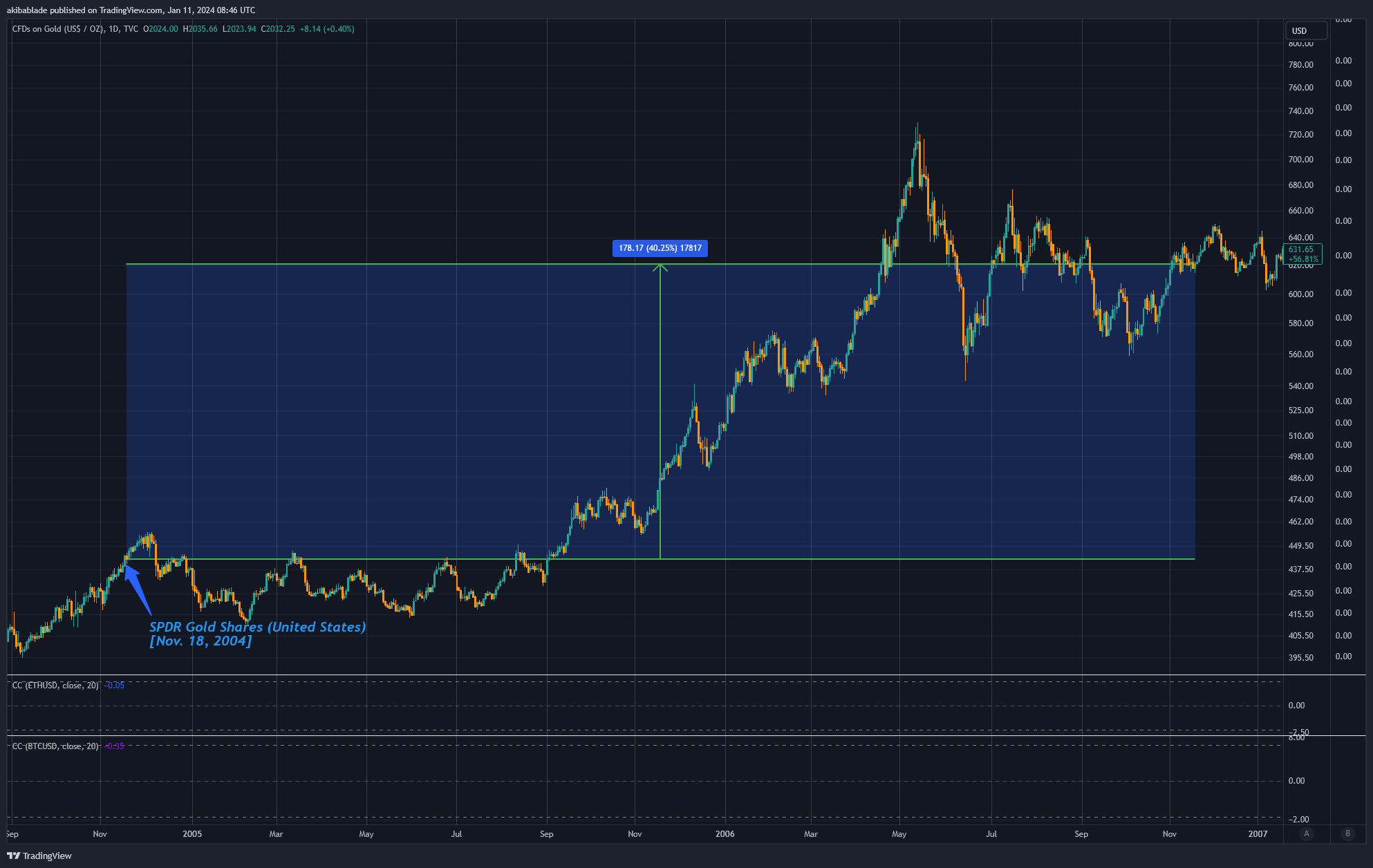

After the local high in Dec. 2004 at $453.40, gold entered a prolonged decline, with the price dropping 4% over the subsequent six months. On its sixth-month anniversary, GLD had accumulated $2.4 billion in assets under management, with gold priced at $419.75.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

However, conditions began to improve significantly for the primary commodity. By Nov. 2004, on the anniversary of its launch, gold had risen to $485.85, an increase of 8.15% since its introduction. Thus, gold’s performance was less impressive than Bitcoin’s after a year and could fluctuate based on a tweet from Gary Gensler. This was far from the groundbreaking impact many anticipate when comparing it to the gold ETF launch.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

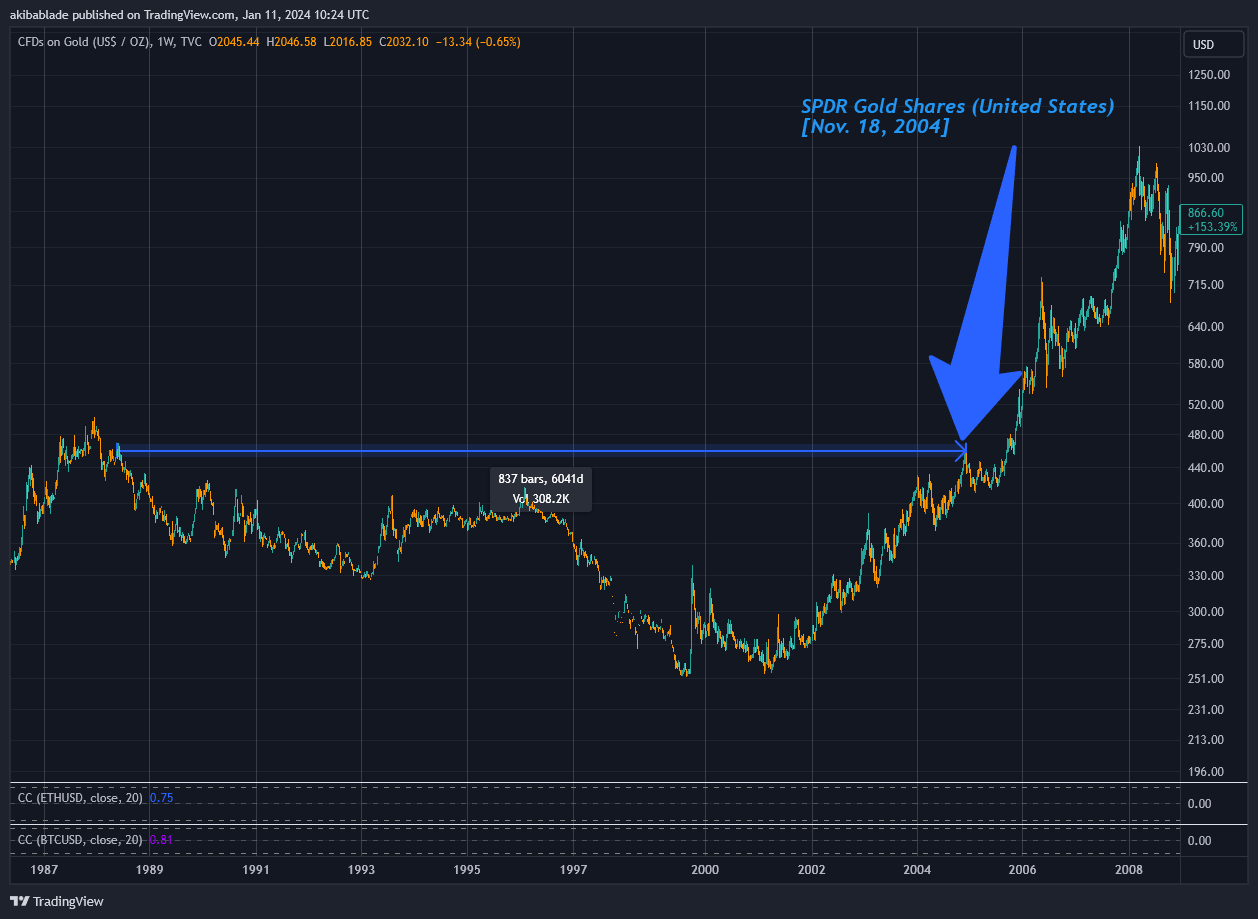

As GLD celebrated its second anniversary on Nov. 18, 2006, gold had risen to $620.50, reflecting an approximate 40% increase.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

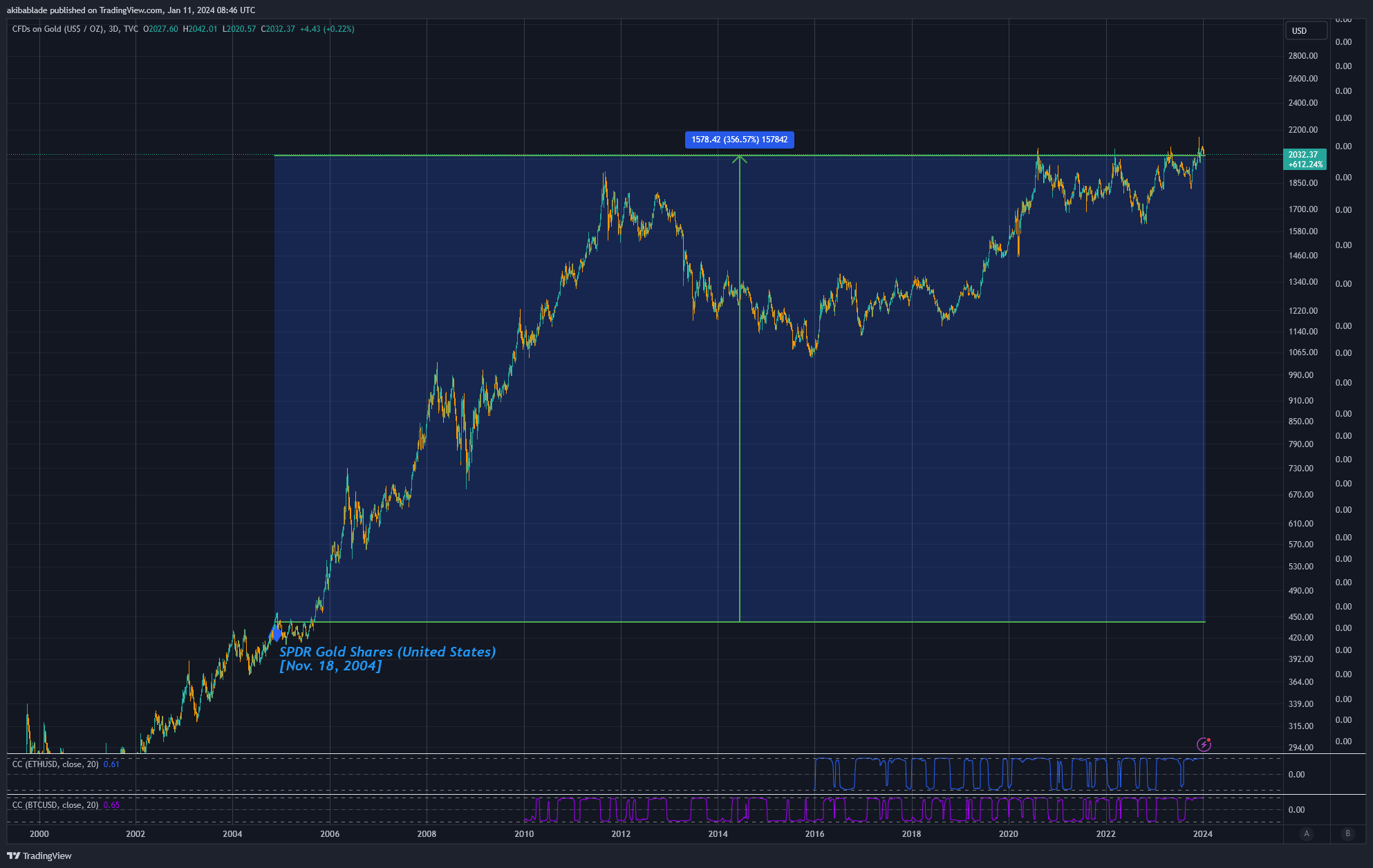

Currently, gold is valued at around $2,032 as of press time, representing an astonishing 356%. However, this is over a nearly 20-year period. In comparison, if Bitcoin were priced at $210,000 on Jan. 11, 2044, how many investors would consider that return satisfactory? Following gold’s trajectory, that would be the price point we would be examining.

Gold Price (Source: TradingView)

Gold Price (Source: TradingView)

Nonetheless, comparing gold and Bitcoin is akin to contrasting apples with oranges. While Bitcoin may be referred to as digital gold, it is undoubtedly much more.

Let’s begin by analyzing gold in relation to the M2 money supply in the U.S. M2 is a comprehensive measure of the money supply. It encompasses all components of M1 (notes and coins, checking accounts, other checkable deposits, traveler’s checks) plus savings deposits, small-denomination time deposits (time deposits in amounts of less than $100,000), and balances in retail money market funds.

M2 only excludes large deposits, institutional money market funds, short-term repurchase agreements, and other larger liquid assets, making it a pertinent long-term metric for evaluating the purchasing power of the U.S. dollar.

Related Posts

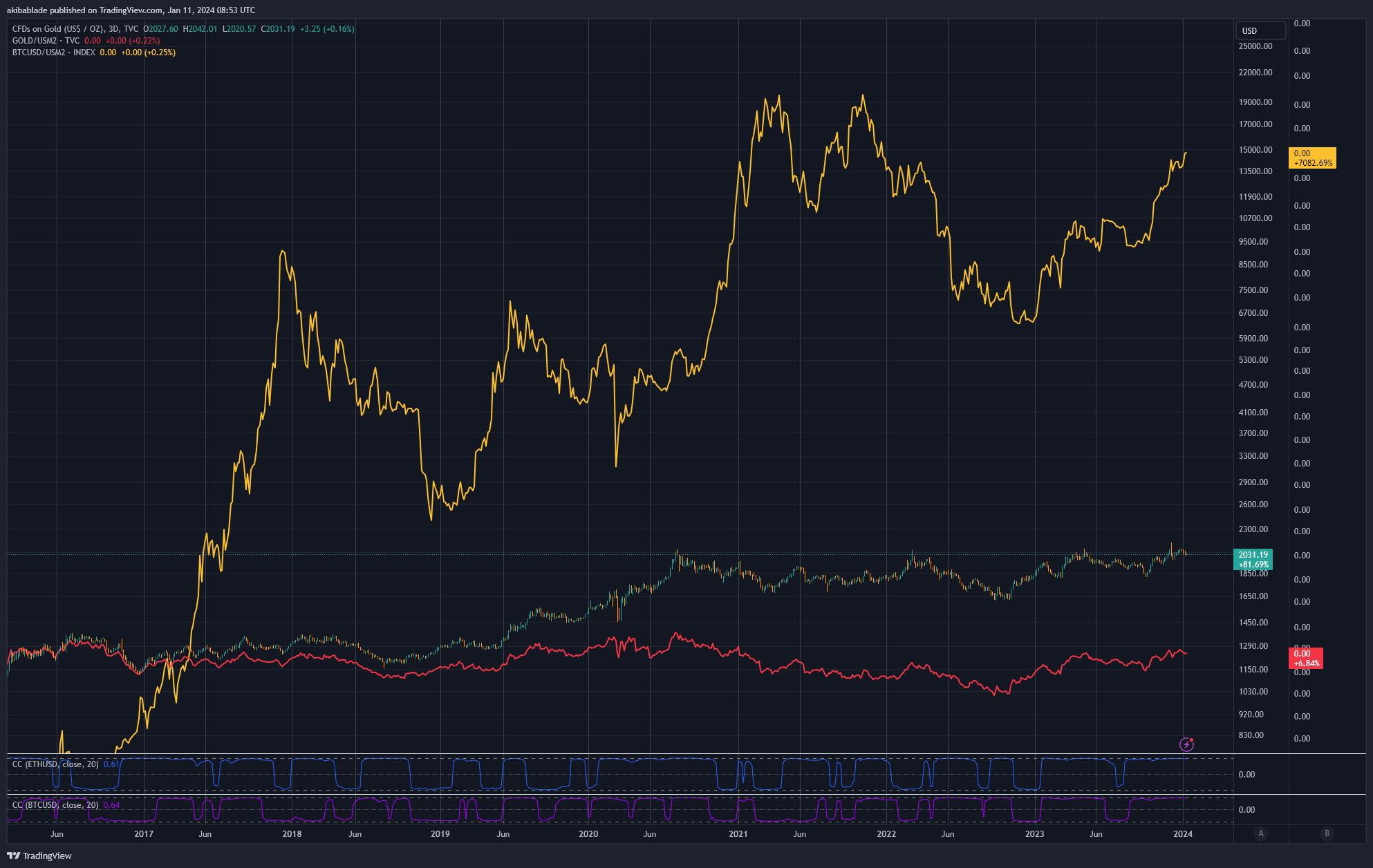

When adjusted for the M2 supply, gold has increased by only 42%. Gold closely followed the Gold/M2 ratio from 2004 until 2012, and while the dollar price of gold continued to rise, Gold/M2 has been on a downward trend since then.

Gold Price vs. M2 Money Supply (Source: TradingView)

Gold Price vs. M2 Money Supply (Source: TradingView)

Comparisons with Bitcoin

Since we cannot compare Bitcoin over the same timeframe as it was not launched until 2009, and its price discovery was highly volatile during its early days, I have utilized the period from 2015 to 2024 in the chart below to compare Gold/M2 to Bitcoin/M2.

As illustrated, Bitcoin has outperformed gold significantly (7,082%) over the past decade, even when accounting for the 70% increase in the M2 money supply.

Gold Price vs. M2 Money Supply vs. Bitcoin (Source: TradingView)

Gold Price vs. M2 Money Supply vs. Bitcoin (Source: TradingView)

Moreover, Bitcoin has demonstrated growth even against dollar dilution, and it possesses a fixed supply and tight market dynamics. Only 30% of all Bitcoin in circulation has been traded within the past 12 months.

Bitcoin’s supply is limited to 21 million coins, rendering it fundamentally scarce. This scarcity is a vital factor in its value, similar to precious metals like gold. However, Bitcoin’s supply is predictably finite, unlike gold, where new reserves can be discovered and mined. The introduction of spot Bitcoin ETFs is likely to enhance the scarcity effect.

As more investors engage with the ETF, a portion of Bitcoin’s limited supply will be secured to support these investment products, decreasing the available supply for regular trading on open markets. This reduced supply could result in price appreciation, particularly in response to rising demand (often driven by easier access through financial products like ETFs). There is also a cyclical aspect here, as ETF issuers must acquire Bitcoin from the open market to fill baskets of shares.

Additionally, the fact that 70% of the current circulating supply of Bitcoin has not moved in over a year indicates a strong holding behavior among existing Bitcoin holders. This holding pattern diminishes the effective circulation of Bitcoin, further increasing its scarcity.

When long-term holders retain a significant portion of an asset, any rise in demand, such as that generated by the launch of a new investment vehicle like the spot Bitcoin ETFs, can have a disproportionate impact on the price. There is less supply available to satisfy this new demand.

This behavior contrasts with gold, where holding patterns are more varied and include substantial industrial and jewelry use, which can suppress the scarcity-driven price appreciation observed in assets like Bitcoin.

Thus, while gold has experienced substantial gains over the past 20 years, comparing its ETF-driven growth to Bitcoin may, in reality, be quite underwhelming.

It is crucial to recognize that demand for Bitcoin in relation to its scarcity must still correlate with its demand at the asking price. It is improbable that Bitcoin will experience the same demand at $1 million per coin as it would at $1 per coin, for example. This is where the critical question arises: at what price does the demand for Bitcoin shift?

Digging into the numbers – Bitcoin vs gold AUM

Yesterday, Bitcoin traded $52 billion across all exchanges at approximately $45,000 – $47,000.

About 6.2 million BTC are in circulation (having moved within the past 12 months). Glassnode estimates that around 7.9 million coins have been lost or are unlikely to move anytime soon. Given the current circulating supply of approximately 19.59 million, we can estimate a liquid pool of between 6.2 and 11.6 million coins available for purchase.

At today’s valuation, this translates to around $291 to $545 billion in liquid coins in the market, or roughly ten times the daily volume traded.

Thus, hypothetically, each of the 11 spot Bitcoin ETFs launching today would need to acquire around $49 billion in AUM to absorb the entire theoretical liquidity in the market.

As of Jan. 10, 2024, the leading gold ETF, GLD, has an AUM of $56 billion. Evaluating the overall top ETFs, SPY has $483 billion, and IVV has $396 billion.

The total assets under management for all gold ETFs in the U.S. amount to approximately $114 billion.

Consequently, there is certainly potential in the market for spot Bitcoin ETFs to acquire currently liquid coins, but it remains a tight market, and in less than 100 days, it will become even tighter.

When analysts draw comparisons between the success of a spot gold launch 20 years ago and the anticipated performance of Bitcoin, they may be significantly underestimating the distinctions between gold and ‘digital gold.’

To put it into perspective, if BlackRock secures the same AUM in Bitcoin as it has in gold (approximately $27 billion), it would represent 5% to 9% of all liquid Bitcoin available in the market. Furthermore, there are currently 2.35 million BTC on exchanges. Therefore, it would need to purchase 24% of exchange-listed Bitcoin… at current prices, that is.

By examining the parallels and differences between the historical impact of Gold ETFs and the potential influence of the forthcoming spot Bitcoin ETFs, it becomes clear that while the success of Gold ETFs was notable, the distinctive characteristics of Bitcoin, such as its fixed supply and prevailing holding patterns, could result in an even more significant impact on the market, highlighting the potential for a transformative effect far beyond what was witnessed with gold.

The post Prediction: Bitcoin ETF will now dwarf gold performance based on historical data appeared first on CryptoSlate.