Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

In this week’s Crypto Long & Short Newsletter, Ruchir Gupta discusses the progress towards establishing a genuine fixed-income market for crypto-native yield. Additionally, Clara García Prieto addresses the mainstream adoption of bitcoin as collateral, noting that many are unprepared for its associated risks.

(Toxic Smoker/ Unsplash)

(Toxic Smoker/ Unsplash)

What to know:

You are reading Crypto Long & Short, our weekly newsletter that provides insights, news, and analysis tailored for professional investors. Subscribe here to receive it in your inbox every Wednesday.

Welcome to our institutional newsletter, Crypto Long & Short. This week’s highlights include:

- Ruchir Gupta addressing the movement towards a legitimate fixed-income market for crypto-native yield.

- Clara García Prieto discussing bitcoin’s role as mainstream collateral, while noting that many are ill-equipped for the risks involved.

- Key headlines of interest for institutions by Francisco Rodrigues.

- Chart of the Week highlights crypto card volumes reaching a record of $140 million.

-Alexandra Levis

Expert Insights

When price stops working, yield starts mattering

– By Ruchir Gupta, co-founder, Gyld Finance

A recurring pattern is observable across various asset classes. Bull markets are straightforward: take on risk, seize beta, and everything appears successful. When the environment shifts, leverage diminishes, and trading volumes decline, the focus transitions from “how much did you gain” to “what are you earning while waiting.”

Related Posts

Currently, crypto is experiencing this transition. Prices have seen substantial corrections, with bitcoin trading nearly 50% below its peak. Speculative positions have contracted. Perpetual funding rates have stabilized. For investors holding digital assets during this period, yield has become the buffer that justifies remaining in the trade.

Staking ether (ETH), as represented by the Composite Ether Staking Rate (CESR), yields approximately 2.5% to 4% annualized. Solana (SOL) validator rewards are closer to 6% to 8%. Lending protocols offer varying rates depending on collateral types. Crypto-native yield is genuine, diverse in its sources, and does not necessitate price appreciation to accumulate.

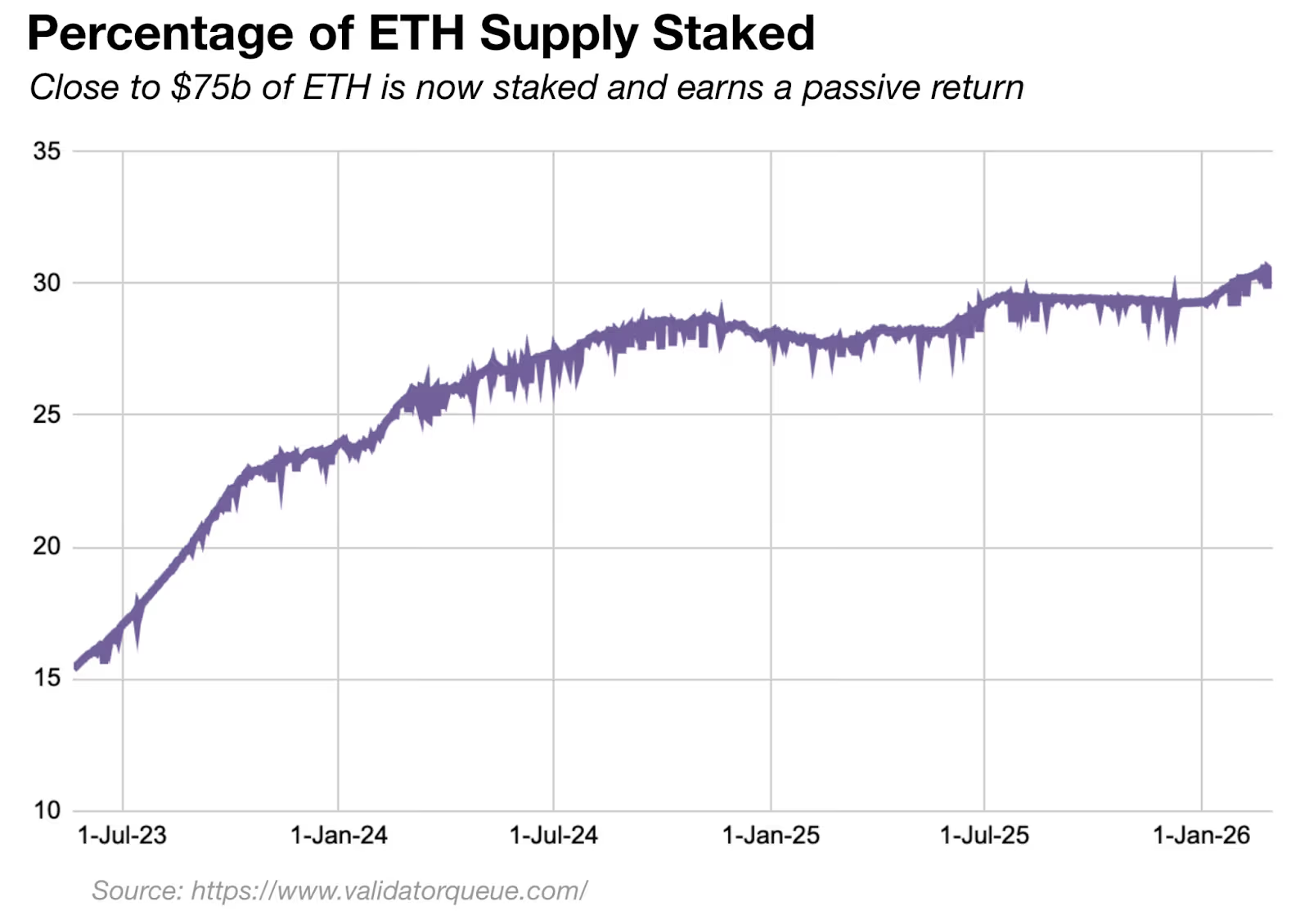

The most compelling evidence lies in the staking participation metrics. The supply of staked ETH has reached record highs, with nearly 30% of all ETH now staked. This increase persisted through periods of notable price declines. Allocators continued staking irrespective of ETH’s performance in spot markets because the yield was available regardless of price movements.

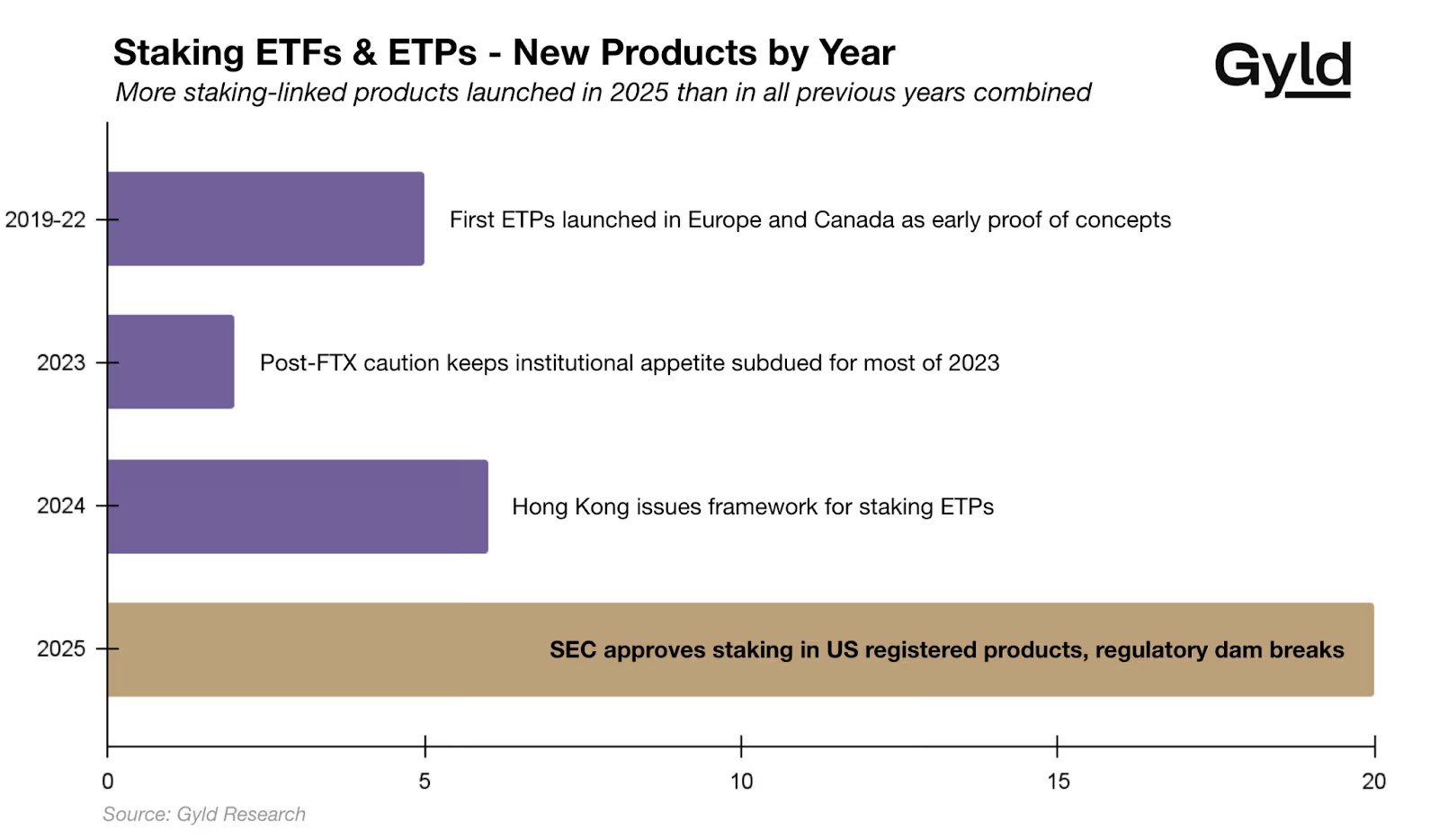

Institutions have taken note. Following the SEC’s provision of regulatory clarity regarding staking in U.S.-registered funds last year, nearly twenty staking-linked ETFs and ETPs have either launched or been filed, including BlackRock’s iShares Staked Ethereum Trust and offerings from VanEck, Grayscale, and Fidelity—more than in all prior years combined. Morgan Stanley, which oversees approximately $8 trillion in client assets, submitted an application in February for a national trust bank charter from the Office of the Comptroller of the Currency (OCC) to provide crypto custody and staking services to its investment clientele.

However, each of these products currently operates as a passive fund. Investors receive yield at whatever rate the network is offering, alongside price exposure, with no option to manage duration or isolate income from principal. This situation leaves much potential untapped.

Staking yield possesses two attributes that render it particularly intriguing as a tradable market:

First, rewards are not fixed and are influenced by network-level activities. Factors such as transaction volumes, validator set sizes, and overall participation all affect the rates. Staking rewards function similarly to macro rates: when network activity is high and demand for block space increases, rewards rise; when activity decreases, they fall. This variability is not merely a risk to be passively absorbed; it serves as a tradeable signal.

Second, staking is intrinsically illiquid in a structured manner. The entry queue for ETH validators currently exceeds two months, meaning capital committed today will not begin earning for over sixty days. This queuing dynamic creates a forward curve. The rate anticipated in three months differs from the rate available today, and the disparity between them is something a market should evaluate.

These two features collectively indicate that staking yield has the components of a legitimate rates market: a floating benchmark that shifts with observable fundamentals, and a term structure shaped by real illiquidity and expectations of forthcoming network activity. This is precisely the type of market that active managers are compensated to navigate.

Seizing this opportunity necessitates a toolkit that is not yet available in a regulated format: instruments that allow pricing yield independently from principal, enabling a buyer to speculate on rate direction without holding spot exposure; instruments with defined maturities that clarify and make tradable the illiquidity premium; and instruments that completely separate the income stream from the capital claim, so each can find its rightful holder. In traditional fixed income, these would be