Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

The U.S. economy nearly came to a standstill, yet inflation remained excessively high, complicating a straightforward intervention by the Federal Reserve.

The U.S. economy commenced 2026 with significantly less momentum than what markets had anticipated a few months prior. As per the Bureau of Economic Analysis, the GDP growth for the fourth quarter of 2025 was revised down to 0.5%, a notable decline from the 4.4% rate observed in the third quarter.

Typically, such a revision would bolster the perspective that the Federal Reserve is nearing rate cuts. However, the challenge lies in the fact that inflation has not sufficiently decreased to provide policymakers with ample leeway.

Recent PCE data released today indicates that headline inflation stood at 2.8% year-over-year in February, with core PCE at 3.0%. Monthly increases in both metrics were recorded at 0.4%, a rate that still suggests persistent price pressures rather than a swift return to the Fed’s 2% target.

This interplay has emerged as a significant macro concern for Bitcoin and the wider cryptocurrency market. Investors are navigating an economy that is losing momentum, while inflation remains robust enough to keep the Fed cautious.

The divergence between these two trends has started to influence the risk landscape. It affects the trajectory of Treasury yields, the pricing of anticipated rate cuts, and the readiness of investors to continue allocating funds into risk assets.

Bitcoin has already demonstrated its ability to attract capital even in challenging macro conditions, particularly when demand for exchange-traded funds remains strong and supply is structurally limited. Nevertheless, weaker growth does not inherently create a more favorable environment for crypto.

The transmission mechanism operates through yields, liquidity, and confidence in the policy direction.

| Metric | Most recent | Previous benchmark |

|---|---|---|

| U.S. real GDP growth, annualized | Q4 2025: 0.5% | Q3 2025: 4.4% |

| PCE inflation, YoY | Feb. 2026: 2.8% | Jan. 2026: 2.8% |

| Core PCE inflation, YoY | Feb. 2026: 3.0% | Jan. 2026: 3.1% |

| Bitcoin price | $72,129 | 24h: +1.20%, 7d: +7.84%, 30d: +1.43% |

Infographic comparing weak U.S. macro data with Bitcoin strength, showing 0.5% GDP growth, 3.0% core PCE inflation, and Bitcoin at $72,129 after a 7.84% weekly gain

Infographic comparing weak U.S. macro data with Bitcoin strength, showing 0.5% GDP growth, 3.0% core PCE inflation, and Bitcoin at $72,129 after a 7.84% weekly gain

The GDP downgrade altered the macro landscape for Bitcoin

As of the latest update on April 9, CryptoSlate’s Bitcoin price page indicates BTC trading at $71,201, reflecting a decrease of 0.72% over the past 24 hours, an increase of 7.60% over the past week, and a rise of 0.99% over the last month. This profile accurately represents the current market condition.

Bitcoin has experienced a rebound, yet this movement has occurred within a macro environment that still appears unsettled. A downward revision in GDP can initially seem like a straightforward recession indicator.

The broader implication lies elsewhere. The downgrade coincided with inflation remaining sufficiently high to keep the typical rescue mechanisms out of immediate reach.

For Bitcoin, the forthcoming movements depend less on a single growth figure and more on whether incoming data can sustainably lower rates and real yields.

The 0.5% GDP figure challenged the notion that the U.S. economy was undergoing a controlled slowdown with enough resilience to withstand tight policy and sufficient disinflation to reduce borrowing costs in an orderly manner.

The series of official estimates, from the advance release to the second and then the third estimates, indicated a clear decline in confidence regarding late-2025 growth. Markets can typically absorb a weak quarter when inflation is decreasing rapidly enough for the Fed to intervene.

This time, however, the inflation aspect of the equation has remained stubborn enough to maintain uncertainty regarding that path.

The PCE report for February exacerbated that issue. Headline PCE met expectations at 2.8% year-over-year, while core PCE came in slightly below expectations at 3.0% compared to a 3.1% consensus.

The monthly details were less reassuring. Both headline and core inflation rose by 0.4% from the previous month, a rate that keeps inflation above the desired level for the Fed if the central bank were preparing to pivot aggressively.

This is why the GDP revision and the inflation figures should be viewed together. The growth slowdown suggests easier policy, while the inflation data keeps that outcome conditional.

Persistent inflation prevented the Fed from providing easy relief

This tension also clarifies why the market response has been more intricate than a typical reaction where weak growth raises hopes for quicker easing. Treasury yields remain sufficiently elevated to maintain restrictive financial conditions.

The 10-year Treasury yield hovered around 4.3% following the GDP and PCE releases, while real yields have remained high enough to sustain competition from safer assets. For Bitcoin, this creates a significant constraint.

Investors can still achieve solid nominal and inflation-adjusted returns in traditional fixed income, which raises the threshold for non-yielding assets. CryptoSlate recently highlighted this dynamic in its analysis of how Bitcoin responds to real yields first.

Related Reading

Related Reading

Altered inflation data exposes a risk that leaves Bitcoin stuck in a high-stakes waiting game

When the data itself is the concern, yields become more significant than the headline, and Bitcoin follows suit.

Jan 24, 2026 · Andjela Radmilac

This remains the most evident transmission mechanism in this context.

The labor market has added another dimension to the situation. The latest BLS employment report indicated March payroll growth of 178,000 and unemployment near 4.3%.

Weekly claims have increased slightly, with the Department of Labor reporting 219,000 initial jobless claims, yet the overall labor backdrop still appears resilient enough to provide the Fed with justification to remain patient. A labor market that is gradually softening, rather than rapidly deteriorating, supports the case for policy patience.

Consequently, markets are contending with two incomplete signals simultaneously: weaker growth and inflation that remains sufficiently elevated to maintain caution.

For households, the practical implications are clear. The economy is decelerating, household expenses still feel elevated, and interest-rate relief may take longer than many anticipated.

Mortgage rates, credit card costs, and consumer financing conditions all reflect that same tension. Bitcoin enters this scenario as a market that often benefits from looser liquidity, lower real interest rates, and a heightened appetite for alternative stores of value.

However, those supports are only partially present at this time. The GDP downgrade has made the soft-landing narrative more challenging to uphold.

It did not, by itself, provide a clear signal for risk assets to rally.

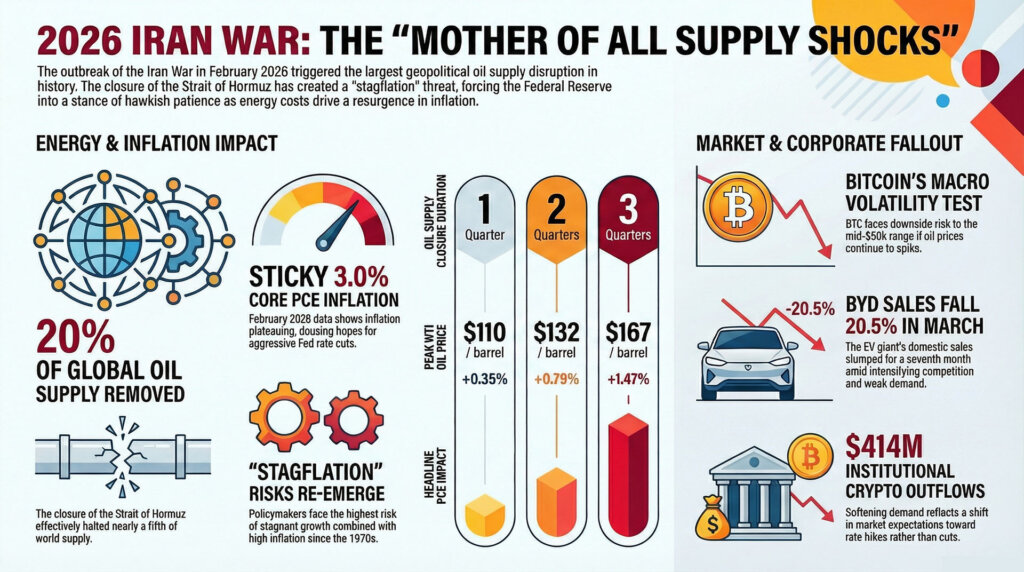

Infographic showing the 2026 Iran war triggering a global supply shock, with 20% oil supply disruption, rising inflation, and impacts on energy prices, markets, and crypto flows

Infographic showing the 2026 Iran war triggering a global supply shock, with 20% oil supply disruption, rising inflation, and impacts on energy prices, markets, and crypto flows

ETF demand is aiding Bitcoin in navigating a challenging macro backdrop

Bitcoin’s recent price movements reflect this uncertainty. The asset has recovered sufficiently to indicate that demand remains genuine, yet the movement has not exhibited the kind of decisive follow-through that would suggest a fully restored risk-on environment.

Related Posts

According to CryptoSlate’s BTC market data, the coin has seen significant gains over the week while remaining nearly unchanged over the past month. This combination suggests a market willing to respond to supportive flows and tactical optimism, while still acknowledging that macro conditions have not yet transitioned into a clearer pro-risk regime.

One factor contributing to Bitcoin’s resilience is the ongoing support from spot ETFs. Spot Bitcoin ETFs attracted approximately $470 million on April 6, marking one of the strongest inflow days of the year.

These inflows provide a crucial counterbalance to macro pressures as they create a consistent source of demand from investors who are allocating through regulated products rather than engaging with short-term volatility directly on crypto-native platforms. ETF demand does not eliminate macro risks.

However, it does alter the asset’s resilience profile. A market with genuine institutional inflows can withstand more pressure than one driven solely by speculative leverage.

Still, the next phase hinges on whether the slowdown evolves into a rates narrative or a stagflation narrative. This distinction is vital.

A rates narrative would involve weaker growth gradually pulling yields and policy expectations lower, thereby enhancing the environment for Bitcoin, growth equities, and other duration-sensitive assets. A stagflation narrative would entail weaker growth alongside persistent inflation pressures that may even accelerate, leaving the Fed constrained and risk assets facing a more challenging environment.

CryptoSlate’s recent explanation of why stagflation is re-emerging as a market term is relevant here, as it translates the jargon into something more comprehensible: costs remain high while the economy appears weaker.

Related Reading

Related Reading

Why Bitcoin was made for the stagflation economic conditions set to dominate 2026

Stagflation: The term of the year for 2026 and why Bitcoin enthusiasts should understand its implications

Mar 22, 2026 · Liam 'Akiba' Wright

Oil, inflation, and policy risk are converging

This is where external factors become more significant than any single crypto-specific catalyst. Energy is once again a focal point in the macro discussion.

CryptoSlate recently highlighted that oil risk and diminished rate-cut expectations are beginning to converge within the market narrative. If energy price pressures translate into inflation expectations, the growth slowdown becomes more challenging for risk assets to celebrate.

The same weak GDP figure that might typically raise hopes for quicker easing could instead heighten concerns that the Fed is losing its ability to respond.

Bitcoin fits into this context through multiple layers. The first layer involves policy expectations, which dictate the trajectory of front-end rates and shape broader liquidity conditions.

The second layer pertains to real yields, which affect the opportunity cost of holding BTC. The third layer involves structural crypto demand, particularly ETF inflows and spot accumulation. The fourth layer is risk sentiment, which determines whether markets interpret incoming data as conducive to easing or threatening to growth.

Bitcoin can perform well when one or two of these layers improve. Sustained upward movement typically becomes easier when three or more align.

Currently, structural demand appears favorable, while policy and rates remain mixed. This is why the market still feels dynamic rather than settled.

The slowdown has opened the door to a potentially more supportive macro path for Bitcoin. However, the inflation data has kept that door only partially ajar.

The upcoming test has a clearer roadmap; inflation, yields, ETF flows, and incoming growth data will inform markets whether the 0.5% GDP figure was merely a late-2025 anomaly or the beginning of something more enduring.

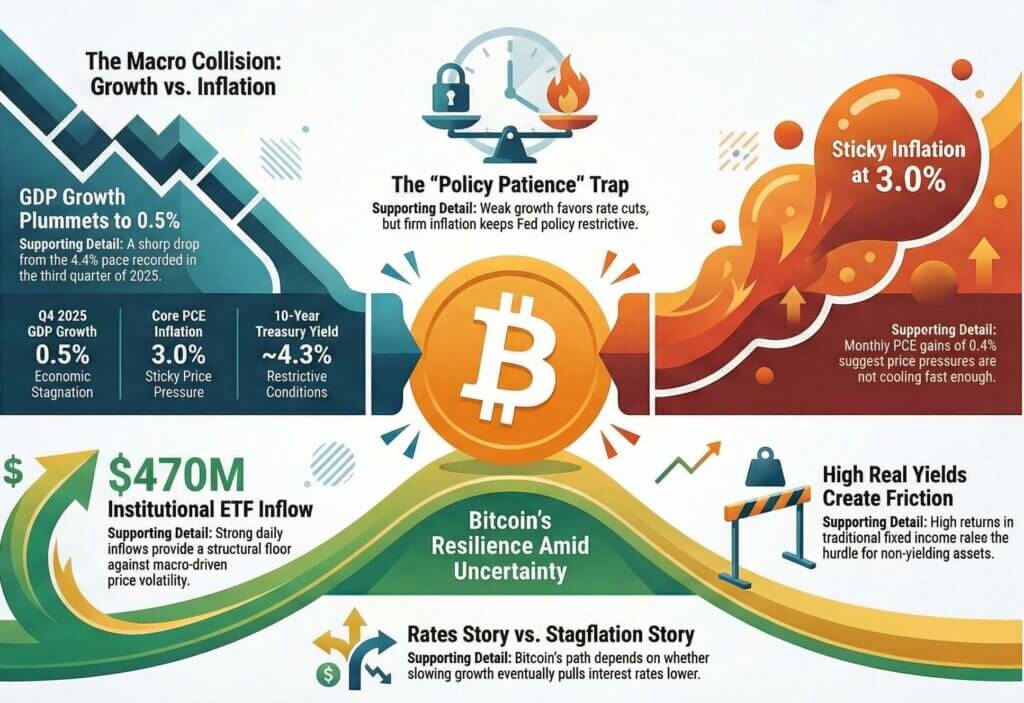

Infographic showing macroeconomic tension between slowing U.S. growth and persistent inflation, highlighting Bitcoin’s resilience, institutional inflows, and the impact of high real yields and restrictive policy conditions

Infographic showing macroeconomic tension between slowing U.S. growth and persistent inflation, highlighting Bitcoin’s resilience, institutional inflows, and the impact of high real yields and restrictive policy conditions

The next 30 to 90 days will determine which side of the contradiction yields first

The upcoming quarter has sufficient scheduled data to compel that decision. The immediate focal points include the next inflation releases, the April Federal Reserve meeting, and the first estimate of the first quarter GDP.

The Atlanta Fed’s GDPNow model will shape expectations leading into that report, while the Cleveland Fed’s inflation nowcast provides a real-time view of how persistent price pressures may remain before the official figures are released. These indicators maintain the emphasis on forthcoming changes rather than a retrospective debate over whether the fourth-quarter weakness was substantial or merely surprising.

A favorable scenario for Bitcoin would commence with a renewed trend of disinflation. This could arise from softer monthly CPI and PCE figures, easing energy pressures, or clearer indications that demand is cooling without a significant labor market disruption.

In such a scenario, yields would have the capacity to decline, Fed cuts would move closer on the market’s timeline, and Bitcoin would benefit from a lower-rate environment while still enjoying structural support from ETF demand. The Federal Reserve’s March Summary of Economic Projections continues to indicate 2.4% GDP growth in 2026, 2.7% PCE inflation, and a year-end fed funds rate of 3.4%.

These figures suggest that the official baseline still leans toward a slower but sustained expansion. If incoming data aligns with this direction, the current growth concern could transform into a pathway to easier conditions rather than a warning of broader decline.

A more challenging scenario would involve inflation remaining near current levels or rising again, particularly if oil or other supply-driven pressures keep monthly figures elevated. In this case, the growth slowdown would feel less like an opportunity for policy relief and more like a constraint on the Fed.

Bitcoin could still draw demand as a scarce asset and as a hedge against long-term policy stress, yet the immediate market reaction would likely remain tied to broader risk sentiment. Elevated real yields and postponed rate-cut expectations would continue to compete with the bullish structural case stemming from ETFs and long-term accumulation.

There is also a middle ground, which may be the most realistic outcome over the coming weeks. Growth could remain subdued without collapsing, inflation could gradually cool without providing immediate relief, and Bitcoin could continue to fluctuate within a range where each positive impulse encounters a macro counterbalance.

This type of market often frustrates directional conviction while still rewarding selective accumulation. It also tends to favor disciplined interpretation over dramatic conclusions.

The broader global context underscores the necessity for balance. The IMF’s latest World Economic Outlook update still forecasts global growth of 3.3% in 2026.

This perspective places the U.S. slowdown in context. It serves as a significant signal, especially as it coincides with inflation that remains above target, yet it has not escalated into a full-blown global crisis.

Bitcoin finds itself at the center of this distinction. It remains vulnerable to macro tightening and sensitive to real yields, while also benefiting from enhanced market infrastructure, deeper institutional access, and a structural demand base that was absent in previous cycles.

One conclusion stands out prominently. The GDP downgrade revealed genuine weaknesses in the soft-landing narrative.

The inflation data has prevented the Fed from providing immediate reassurance. Consequently, Bitcoin is navigating an unresolved macro contradiction, one that will likely be clarified by the next series of inflation, labor, and growth data rather than by today’s revision alone.

Growth has decelerated sharply, inflation continues to exert influence on policy, and Bitcoin’s next sustained movement will hinge on which side of that tension yields first.

The post The U.S. economy almost stalled, but inflation still stayed too hot for an easy Fed rescue appeared first on CryptoSlate.