Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Strategy’s STRC achieves all-time high trading volume following significant $1B Bitcoin acquisition as market capitalization doubles since Friday.

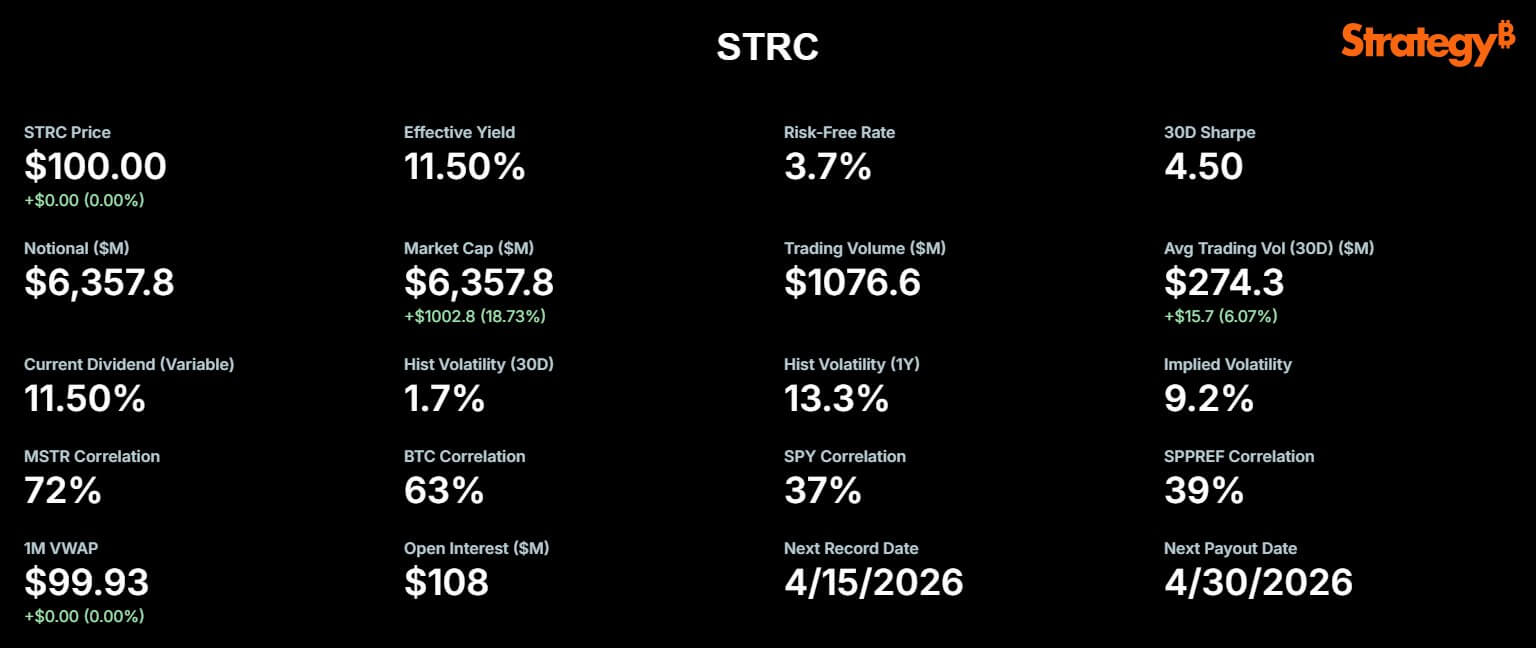

Strategy’s perpetual preferred stock, STRC, was instrumental in the company’s Bitcoin strategy this week, achieving over $1.1 billion in daily trading volume.

In a post on X, Strategy announced April 13 as the record date for STRC. Michael Saylor also mentioned that the security closed at par with merely “one penny of volatility” after $1.156 billion in liquidity flowed through the market.

STRC Record Trading Volume. (Source: Strategy)

STRC Record Trading Volume. (Source: Strategy)

This trading spike followed Strategy’s disclosure that it had acquired 13,927 Bitcoin for approximately $1 billion between April 6 and April 12.

With this acquisition, the company now possesses 780,897 Bitcoin, purchased for a cumulative total of $59.02 billion, averaging $75,577 per coin.

The company indicated that the purchase was entirely financed through at-the-market (ATM) sales of 10.02 million STRC shares, yielding around $1 billion in net proceeds.

Simultaneously, the combination of unprecedented trading activity in STRC and a weekly Bitcoin purchase funded solely through that preferred program signifies a notable shift in focus for the company.

For equity investors, this transition could substantially alter the dynamics of potential rewards and risks. An increased dependence on preferred stock may lessen immediate dilution for common shareholders, as fewer ordinary shares are issued initially.

However, it introduces more fixed claims ahead of equity in the capital structure, meaning preferred stockholders have the right to receive dividends before common shareholders receive any distributions. In essence, preferred shareholders are prioritized for payments, so common shareholders benefit only if the company retains sufficient profit after fulfilling these obligations.

This strategy could enhance returns if Bitcoin performs favorably, but it heightens reliance on continuous market access and disciplined dividend management. While the shift may increase short-term purchasing power and decrease equity dilution, it also elevates financial leverage and execution risk for common shareholders over time.

How STRC preferred stock took the lead for Strategy’s Bitcoin purchases

Introduced in July 2025, STRC was designed to function fundamentally differently from Strategy’s MSTR common stock.

Related Reading

Related Reading

Strategy launches ANOTHER Bitcoin share class to lure capital from $7T traditional funds

Strategy is expanding its Bitcoin-linked securities, providing innovative options for income-seeking investors to potentially outpace inflation.

Jul 22, 2025 · Oluwapelumi Adejumo

The preferred stock features a variable annualized dividend rate, currently set at 11.50% as of April. Its adjustable-rate structure is designed to strongly incentivize trading near its $100 par value.

This stable price anchor allows Strategy to utilize its ATM issuance program effectively. Issuing new STRC shares at a consistent price enables the company to rapidly raise capital and convert it into Bitcoin, reducing the friction and discounts typically associated with large secondary offerings.

Market observers note that STRC aims to deliver double-digit returns to investors while maintaining minimal price volatility, merging high-yield income with capital stability.

Essentially, Strategy’s executive chairman, Michael Saylor, stated:

“STRC delivers money market–like stability with market-leading risk-adjusted returns.”

Since its launch, STRC has financed the acquisition of nearly 70,000 Bitcoin, according to STRC.live. The recent $1 billion volume on April 13 could facilitate the purchase of over 6,000 additional BTC.

Strategy’s STRC Market Cap (Source: STRC.live)

Strategy’s STRC Market Cap (Source: STRC.live)

Unsurprisingly, STRC’s market capitalization has surged alongside this utility, nearly doubling from $3.4 billion in February to $6.36 billion today. With $21.6 billion worth of STRC shares still authorized for future issuance, the potential for further BTC accumulation remains extensive.

Related Reading

Related Reading

Strategy is using a high-yield funding engine to buy billions in Bitcoin and chase 1 million BTC

Strategy’s pursuit of 1 million Bitcoin relies on a high-yield engine that could either accelerate growth or hinder it.

Mar 17, 2026 · Oluwapelumi Adejumo

Bears point to reserves, refinancing, and the growing preferred stack risks

Despite market optimism, several analysts have expressed concerns regarding the sustainability of this model, referencing Strategy’s own financial disclosures.

As Strategy’s software business does not generate sufficient operating cash flow to meet its financial commitments, the company established a $2.25 billion reserve in early February. This reserve acts as a financial safety net, intended to cover nearly 2.5 years of dividend payments on preferred stock and interest payments on outstanding debt.

The reserve is essential because, without adequate regular business income, the company depends on this set-aside cash to fulfill fixed payments. If this reserve is exhausted before Strategy generates enough new income or identifies additional financing sources, the company could face pressure to liquidate assets or issue more shares, putting both preferred and common shareholders at risk.

Related Posts

Critics contend that a structure reliant on ongoing market access may seem stable until financing conditions change.

Independent Bitcoin analyst Derin Olenik recently released a critical analysis of the company’s obligations, cautioning that the current ATM growth rate is unsustainable.

According to Olenik’s calculations, the STRC obligations are escalating dramatically, with the notional value increasing at a compound monthly rate of approximately 30%.

At this rate, the company’s obligations could more than double every three months and increase tenfold within a year, significantly intensifying the pressure on cash flow and reserves.

If this trend continues, Olenik estimates Strategy will deplete its $2.25 billion reserve in just nine to ten months, rather than the anticipated two-and-a-half years.

He warned that, to cover such a shortfall without liquidating Bitcoin, Strategy would need to significantly dilute its common shareholders.

Even if MSTR returns to its previous all-time high, Olenik calculates that the company would need to issue over 1 billion new shares to cover preferred dividends, diluting existing common equity by nearly 400%.

In light of this, he concluded that:

“If ATM issuance halts, Bitcoin accumulation stops. If issuance continues, the math dictates hyper-dilution regardless of the stock price. From a common shareholder’s perspective, STRC should not be viewed as Digital Credit, but rather Digital Kamikaze.”

MSTR bulls see STRC as a cleaner way to add Bitcoin

Conversely, Strategy supporters contest the bleak scenario Olenik has outlined.

They argue that Strategy has effectively tapped into a distinct investor base of income-focused buyers willing to accept a fixed claim and limited upside for STRC.

By channeling proceeds from these conservative investors into an asset with high anticipated long-term volatility and upside, Strategy preserves Bitcoin exposure for common shareholders.

Preferred investors receive a yield-focused instrument that currently behaves more like short-duration credit than a cryptocurrency proxy. In practical terms, ‘short-duration credit’ refers to debt securities or financial instruments that mature in a relatively brief period, typically less than five years.

These investments are often perceived as less risky because their values are less sensitive to interest rate fluctuations and are expected to return principal to investors sooner. For STRC, this implies its trading behavior is more stable and predictable, akin to short-term corporate bonds, rather than mirroring the price volatility typical of cryptocurrencies.

Notably, Strategy itself has consistently referred to STRC as its flagship “Digital Credit” instrument.

Bitcoin analyst Adam Livingston remarked:

“[STRC] is a machine that converts capital markets access into long-duration Bitcoin exposure, while the fixed claim gets smaller and smaller relative to the asset if BTC keeps compounding.”

Supporters assert that the model is effective as long as Bitcoin appreciates faster than the cash cost of servicing the preferred dividend.

In this scenario, each successful STRC issuance transforms capital markets demand into additional Bitcoin holdings, while the fixed preferred claim diminishes relative to the asset base as Bitcoin appreciates over time.

Saylor has also reassured anxious investors, stating:

“Our BTC Breakeven ARR [Accounting Rate of Return] is approximately 2.05 percent. If Bitcoin grows faster than that over time, we can cover our dividends indefinitely without issuing new MSTR shares.”

MSTR common shareholders remain the key audience

For MSTR holders, the crucial question is whether this funding model continues to be accretive to the common stock over time.

In the short term, the evidence is encouraging. STRC experienced record turnover, remained at par, and Strategy utilized this market access to acquire $1 billion of Bitcoin in one week.

This result supports management’s perspective that STRC can function as a reliable, repeatable funding channel rather than merely a one-time financing tool.

Over a longer timeframe, the situation is inherently more complex. Every successful STRC raise adds another layer of fixed claims ahead of the common stock.

Strategy’s own risk disclosures acknowledge that future preferred issuance could dilute existing shareholders and that adverse shifts in financing conditions could complicate the maintenance of necessary dividend reserves.

Dilution refers to the reduction in existing shareholders’ ownership percentage when new shares are issued, thereby decreasing each shareholder’s claim on the company’s assets and profits. Financing conditions are significant because if the company cannot access affordable or stable funding, it may struggle to raise sufficient capital to support dividend payments or sustain its financial structure, increasing overall risk for both preferred and common shareholders.

Ultimately, STRC illustrates both strength and risk. It operates as intended by attracting substantial liquidity and maintaining a price near par.

Yet it creates tension because each issuance round ties the broader Strategy thesis ever more closely to the company’s ability to preserve market access, sustain dividend support, and keep Bitcoin valuable enough to justify the financial structure built around it.

The post Strategy’s STRC hits record trading volume after massive $1B Bitcoin purchase as market cap doubles since Friday appeared first on CryptoSlate.