Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Strategy generated close to $2 billion from Bitcoin this year, but SEC documentation conceals a significantly larger figure.

Strategy (previously MicroStrategy) asserts that its bold Bitcoin acquisitions have resulted in an almost $2 billion profit this year, despite the evident price challenges faced by the leading asset.

However, a detailed examination of the enterprise software firm’s legally mandated regulatory documents reveals a much bleaker scenario: according to standard accounting practices, the company is grappling with a multi-billion dollar unrealized loss, and its total Bitcoin holdings are significantly underwater.

In spite of these paper losses, the firm shows no inclination to reduce its pace. Equipped with a robust capital markets mechanism, Strategy continues to issue equity to finance substantial daily purchases, remaining undeterred by the disparity between its curated corporate metrics and its stark regulatory situation.

A tailored winning streak

According to its own standards, Strategy’s Bitcoin treasury strategy is impeccable, even amid the ongoing bear market conditions in the wider crypto landscape.

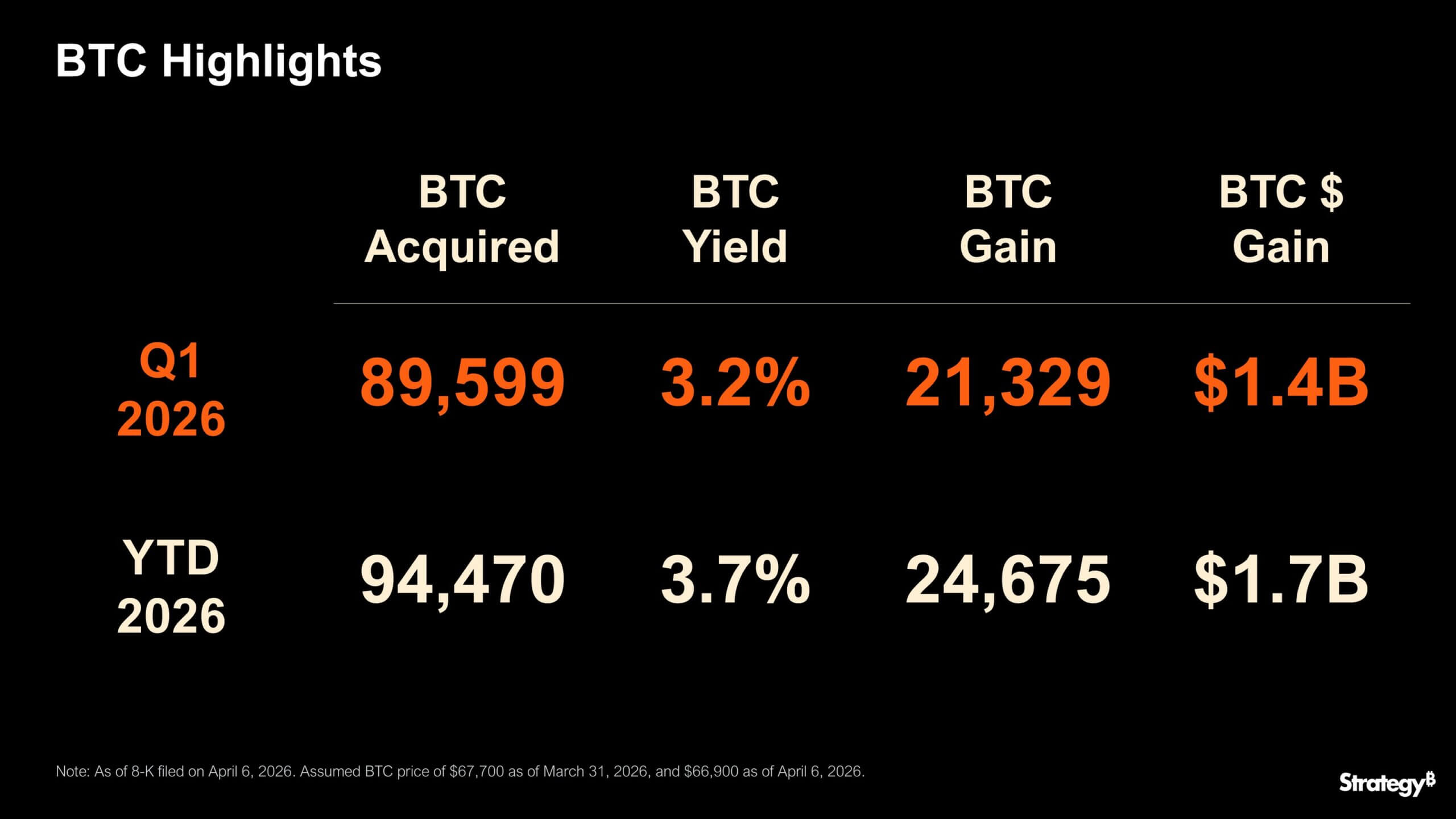

On X, the company reported that its BTC acquisition strategy has produced nearly $1.7 billion in Bitcoin profits since the start of this year.

Strategy's Key Bitcoin Metrics (Source: Strategy)

Strategy's Key Bitcoin Metrics (Source: Strategy)

This figure concludes a remarkable accumulation period that has fundamentally altered the supply dynamics of the crypto market.

Importantly, Strategy revealed that it has obtained an impressive 2.2 times the newly mined Bitcoin supply during this timeframe, amounting to over 94,000 BTC since the year’s onset.

To illustrate this, Strategy’s management highlights two proprietary metrics: “BTC Yield” and “BTC Gain.” The company reports achieving a BTC Yield of 3.7% this year, resulting in a BTC Gain of 24,675 coins (approximately $1.7 billion).

For retail investors and crypto supporters, these statistics serve as clear evidence that the firm’s leveraged accumulation approach is effective.

Strategy’s Bitcoin gain metric is structured to reward balance-sheet growth on a per-share basis. In its annual report, the company states that BTC Yield reflects the percentage change in Bitcoin Per Share (BPS) from the start to the end of a period.

BTC Gain then translates that percentage change into a concrete Bitcoin figure by multiplying the amount of Bitcoin held at the beginning of the period by BTC Yield. BTC $ Gain further extends this by multiplying BTC Gain by the market price of Bitcoin.

The $14 billion SEC reality

Nonetheless, the shift from the company’s promotional materials to its Securities and Exchange Commission filings, along with the reported $1.7 billion gain, is overshadowed by a staggering accounting shortfall.

Strategy’s quarter-end filing indicates that the firm recorded a $14.46 billion unrealized loss on its digital assets for the three months ending March 31.

Under the fair-value accounting standards implemented in January 2025, fluctuations in market prices must be reflected directly in the income statement. As Bitcoin’s price declined between year-end and March 31, Strategy was compelled to reduce the official carrying value of its digital assets from $58.85 billion to $51.65 billion.

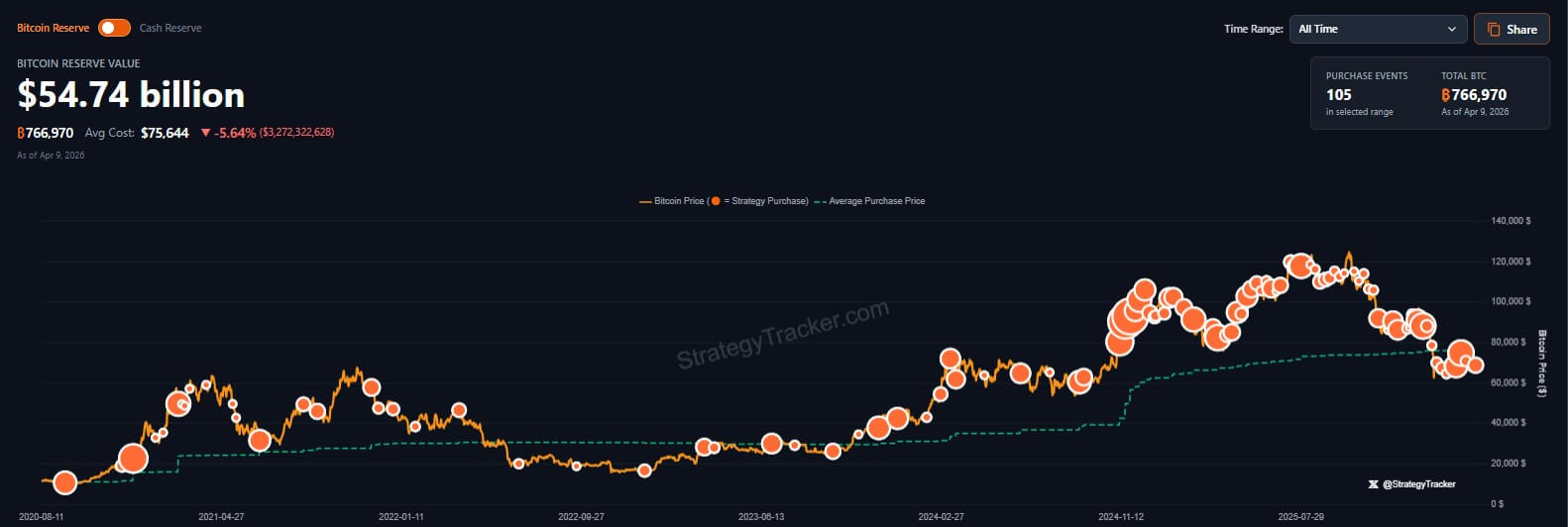

In addition to the quarter-end accounting losses, the company’s overall cost basis is also underwater. Strategy made significant purchases in a declining market during the first quarter, raising its total holdings to 766,970 BTC. The total acquisition cost was $58.02 billion, averaging $75,644 per coin.

With Bitcoin currently trading around $71,192, that reserve is valued at approximately $54.60 billion, placing the company about $3.41 billion below its total cost.

Related Posts

Strategy's Bitcoin Holdings Value (Source: Strategy)

Strategy's Bitcoin Holdings Value (Source: Strategy)

Strategy's Bitcoin buying continues with STRC

Despite billions in paper losses and an average purchase price that exceeds the market value, Strategy maintains that it will not sell any coins. Instead, it is reinforcing its position.

The ultimate testament to the market’s readiness to support this conviction is evident in the company’s STRC preferred stock issuance.

STRC is a high-yield credit structure that offers an 11.5% annual dividend. The asset is intended to trade closely to its par value of $100, and Strategy can effectively utilize its at-the-market (ATM) issuance program to finance aggressive Bitcoin purchases.

Indeed, STRC.live estimates indicate that STRC experienced daily volume reaching $333 million, marking the seventh-highest trading volume since its launch, on April 8. This trading activity could facilitate the acquisition of over 2,000 additional Bitcoins.

The figures are a vital indicator of financial stability for Strategy’s specific strategy, suggesting that demand for the firm’s equity remains insatiable.

As long as Wall Street continues to absorb equity offerings at a stable valuation, Strategy faces no immediate pressure to cease its operations.

Where the pressure sits

The company’s own disclosures clarify why the dashboard metric and the ongoing purchasing spree do not resolve the broader balance-sheet issue.

Strategy acknowledges that its Bitcoin KPIs do not account for existing and future liabilities, nor the preferential rights of preferred stockholders to dividends and assets in a liquidation scenario.

The annual report notes that purchases financed through non-convertible notes or preferred stock can simultaneously inflate BTC Yield, BTC Gain, and BTC $ Gain while also increasing overall indebtedness and senior claims on the asset pool.

This qualification has become increasingly significant as the capital structure expands. Strategy stated in February that it had established a $2.25 billion USD Reserve, providing approximately 2.5 years of dividend and interest coverage.

However, STRC has grown to a $3.4 billion market cap, and cumulative preferred distributions paid had reached $413 million at a blended annual rate of 9.6%.

Crucially, the annual report explicitly states that the software business is not anticipated to generate sufficient operating cash flow over the next 12 months to fulfill the company’s financial obligations and liquidity requirements, indicating that ongoing financing is essential to the model.

This implies that a significant drop in the market value of Strategy’s Bitcoin holdings, or a negative shift in investor sentiment and financing conditions, could hinder the firm’s ability to secure adequate equity or debt financing to meet obligations.

These risks are most likely to arise when Bitcoin is trading below its carrying value or cost basis. If the company cannot obtain financing in a timely manner or on acceptable terms, Strategy has acknowledged that it may need to sell Bitcoin to meet financial obligations or liquidity needs.

For the time being, the operation continues. Strategy is acquiring Bitcoin, the marketing dashboard still reflects a positive Bitcoin gain, and STRC remains close to par while providing fresh capital.

The post Strategy made nearly $2 billion on Bitcoin this year but SEC filing hides a far bigger number appeared first on CryptoSlate.