Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Bitcoin’s recovery could be tenuous as Wall Street cautions that the Hormuz disruption is not fully resolved.

A two-week conditional ceasefire between the U.S. and Iran has necessitated a swift revision of trade dynamics in the Strait of Hormuz, yet it has not completely reinstated the pre-war macroeconomic environment.

Oil prices have significantly decreased from their panic-induced peaks, global equities have surged, and Bitcoin has experienced a recovery alongside them. This marks a distinct departure from the pre-ceasefire sentiment, where markets appeared to abandon hopes for any imminent reopening.

The primary shift has been in the projected trajectory for energy. However, the path toward normalizing physical flows, insurance, shipping, and inflation remains unresolved.

Why this matters

The market no longer needs to account for an immediate worst-case scenario regarding closures, but it must still factor in a gradual return to standard energy flows. This is significant beyond just oil traders, as persistent fuel costs can sustain inflation at higher levels, limit the Federal Reserve’s ability to ease, and position Bitcoin as a macro risk asset rather than a straightforward safe-haven investment.

JPMorgan, UBS, and U.S. government energy analysts continue to characterize a slower recovery process beneath the ceasefire narrative. Their analyses no longer present a live argument against any reopening; instead, they serve as a caution that reopening and normalization are not synonymous.

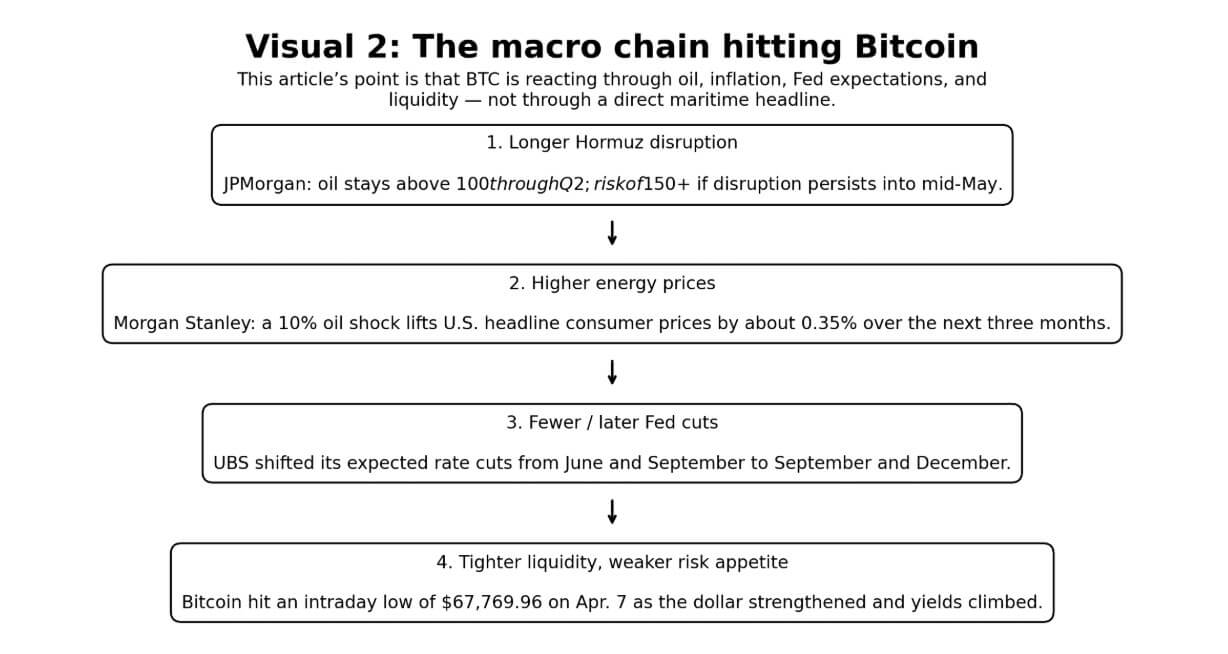

JPMorgan’s baseline scenario still anticipates elevated oil prices through the second quarter and cautions that crude could exceed $150 if disruptions escalate or continue into mid-May.

UBS predicts that while the conflict may de-escalate, damage to infrastructure will significantly delay the restoration of production to pre-conflict levels.

The EIA states that complete restoration of oil flows through the Strait of Hormuz will take time, even after the conflict concludes.

None of these three entities is forecasting a rapid return to normalcy in the energy market, which is now a crucial point for market participants. The ceasefire has mitigated immediate tail risks but has not yet assured the smooth movement of cargo, normal inventory levels, or typical inflation pass-through.

The Strait of Hormuz transported 20.9 million barrels per day in the first half of 2025, accounting for approximately 20% of global petroleum liquids consumption and one-quarter of all maritime oil trade. It also managed 11.4 billion cubic feet per day of LNG, representing over 20% of global LNG trade.

U.S. intelligence assessed on April 3 that Iran’s presence in the strait is significant, as control over global energy flows is a key leverage point for Tehran.

This assessment was more impactful prior to the ceasefire as a directional market indicator, but it still serves as a structural reminder that formal de-escalation does not automatically ensure frictionless navigation.

| Institution / actor | Current timeline / base case | Key forecast / assessment | What it implies for oil | What it implies for markets |

|---|---|---|---|---|

| JPMorgan | Ceasefire reduces immediate tail risk, but disruption risk extends through Q2; partial normalization remains the base path | Oil may remain elevated through Q2 and could exceed $150 again if disruptions continue into mid-May or the ceasefire collapses | Crude can decline from panic highs without a swift return to pre-shock pricing | Relief rally now, but inflation and rate-cut pressures may persist |

| UBS | Conflict may ease in the coming weeks, but recovery will take longer | Infrastructure damage means restoring production to pre-conflict levels will require significantly more time | Energy markets may loosen before they fully normalize | Risk assets may recover first, with macro normalization following later, if at all |

| EIA | Full restoration will take months even after the conflict ends | Flows, routes, and output will normalize gradually; retail fuel costs will remain high | Oil and fuel prices may stay elevated even after a nominal reopening | Consumer-price pressures will persist beyond the ceasefire narrative |

| U.S. intelligence | Iran continues to view chokepoint control as strategic leverage | Tehran considers energy-flow control a fundamental bargaining tool | Lower confidence in a frictionless reopening | Markets maintain a geopolitical risk premium beneath the relief rally |

| Ceasefire backdrop | Immediate escalation risk has diminished, but durability remains uncertain | Markets can price reopening faster than shipping systems can normalize | Crude loses the panic premium first; physical tightness may linger longer | Relief rally in risk assets is justified, but the macro all-clear is not yet confirmed |

Physical oil markets remain critical to observe for indications of whether reopening leads to normalization. The ceasefire has alleviated the headline shock, but immediate cargo pricing, insurance conditions, and routing friction are more telling than front-month futures alone.

Earlier this week, North Sea Forties crude reached $146.09 per barrel, Dated Brent hit $141.365, and some immediate cargoes traded above $150, while European jet fuel reached $226.40 and diesel $203.59. Brent futures peaked near $110 during the height of the panic.

The disparity between immediate physical prices and the headline futures market is where inflation transmission is still evident.

According to Morgan Stanley’s consumer analysis, a 10% increase in oil prices due to a supply shock raises U.S. headline consumer prices by approximately 0.35% over the subsequent three months, with real consumption beginning to decline and remaining subdued for the following five to six months.

The EIA’s April forecast projects U.S. gasoline prices averaging above $3.70 for 2026, with diesel peaking above $5.80 and averaging $4.80 for the year.

The macro chain

Bitcoin’s trading dynamics still flow through oil, then inflation, followed by Fed policy, and finally risk appetite. The distinction after the ceasefire is that the chain has loosened but not broken.

Bitcoin reached an intraday low of $67,769.96 on April 7, when the oil shock, stronger dollar, and rising Treasury yields compressed risk appetite across markets.

Since the ceasefire, BTC has bounced back alongside equities as traders adjust for a lower likelihood of an immediate worst-case energy scenario. This movement is logical, but it does not yet resolve the subsequent question of whether lower oil headlines will lead to a sustained easing of inflationary pressures and rate expectations.

Related Posts

Earlier this year, BTC surged back above $70,000, with the same rationale now in play. Currently, liquidity conditions are still influenced by energy prices.

A four-step flowchart illustrates how a prolonged disruption in Hormuz transmits through energy prices, Fed policy, and liquidity to impact Bitcoin.

A four-step flowchart illustrates how a prolonged disruption in Hormuz transmits through energy prices, Fed policy, and liquidity to impact Bitcoin.

UBS has adjusted its Fed rate cut expectations from June and September, while also increasing the likelihood of a U.S. recession. IMF chief Kristalina Georgieva stated that even a quick resolution would lead to higher inflation forecasts.

Dallas Fed economists project that the Strait of Hormuz disruption could raise average WTI prices to $98 in the second quarter and reduce annualized global real GDP growth by 2.9% during that quarter. A two-quarter disruption could push WTI to $115 in the third quarter, while a three-quarter disruption could elevate it to $132 by year-end.

This modeling is now more effective as a risk map for potential ceasefire failure or incomplete normalization rather than as a live baseline scenario. The market has distanced itself from a pure closure outlook but has not yet fully priced a return to pre-conflict macro conditions.

Consequently, the rate-cut discussion has evolved. Traders are no longer questioning whether the oil shock is intensifying; they are now inquiring whether the relief rally will last long enough to allow for a reopening of Fed options later this year.

When gasoline averages above $3.70 and diesel exceeds $4.80, the financial impact reverberates through every sector of the real economy, tightening financial conditions well before the Fed takes formal action.

Likely scenarios

The baseline scenario has shifted. It is no longer a complete market capitulation regarding a near-term reopening. Instead, it reflects a ceasefire relief rally with underlying incomplete normalization.

This intermediate path remains significant for Bitcoin, as lower oil prices are beneficial only if they continue to translate into reduced inflationary pressures, steadier growth expectations, and a more credible path for rate cuts.

The bear scenario now hinges on either a ceasefire breakdown or an extended period where shipping resumes only partially, keeping the physical market pricing scarcity. If disruptions extend into JPMorgan’s mid-May threshold, the market could revert to previous conditions.

Dallas Fed modeling indicates WTI could reach $115 in the third quarter under a two-quarter disruption. Morgan Stanley cautions that if Iran maintains structural control over cargo flows, even during a nominal reopening, oil markets may continue to trade at a higher risk premium.

For Bitcoin, this setup aligns with the clearest near-term downside scenario: oil prices remain high, inflation expectations rise, the Fed remains cautious, and risk assets lose their relief momentum.

Options demand clustered around $60,000 to $50,000 downside strikes during the last acute risk-off period. A retest of that range becomes increasingly plausible if the situation deteriorates back toward the pre-ceasefire stress trajectory.

| Scenario | Oil outcome | Inflation effect | Fed implication | BTC implication | Key condition to watch |

|---|---|---|---|---|---|

| Bear case: ceasefire fails or disruption lasts into mid-May or longer | Oil re-establishes at very high levels; $150 returns as a working risk benchmark | Inflation expectations begin to rise again | Fed remains on hold longer; rate-cut hopes diminish | Strongest near-term downside scenario; retest of lower ranges becomes more likely | Whether disruption continues through JPMorgan’s mid-May threshold or the truce collapses |

| Bull case: ceasefire holds and navigation genuinely normalizes | Brent declines sharply toward pre-shock levels | Inflation shock unwinds more rapidly | Easing expectations return more clearly | BTC rebounds alongside equities and broader risk assets | Whether navigation is restored freely, with insurance and cargo flows normalizing quickly |

| Middle case: reopening without normalization | Oil decreases from extremes but retains a significant risk premium | Inflation cools only gradually | Fed receives limited relief and remains cautious | BTC improves only partially; upside remains constrained by persistent macro pressures | Whether reopening actually normalizes flows, inventories, and pricing |

| Sticky-aftershock case | Physical flows improve, but fuel and supply-route normalization takes months | Consumer-price pressures persist even after calmer headlines | Financial conditions remain tight before the Fed alters policy | BTC does not receive an immediate all-clear even after calmer headlines | Whether gasoline, diesel, and supply-chain stress remain elevated into later quarters |

The bull case is still linked to Morgan Stanley’s perspective that if flows return genuinely and freely, Brent could decline toward $70, as global oil appeared oversupplied prior to the conflict.

In this scenario, the inflation shock reverses more swiftly, Fed easing comes back into focus, and Bitcoin recovers alongside equities. This is the rationale the current relief rally is attempting to price in.

The decisive condition remains: genuine freedom of navigation is essential.

A ceasefire that restricts physical cargo movement due to security risks, insurance issues, congestion, or operational control results in a different oil market, where part of the risk premium remains embedded, and Bitcoin’s upward trajectory is constrained by the same inflationary pressures.

This distinction between reopening and normalization is where institutional research is now converging.

The EIA indicates that full restoration of flows will take months, even after the conflict concludes, as supply routes and output normalize. Morgan Stanley asserts that real consumption will remain depressed for five to six months following an oil shock of this magnitude.

For Bitcoin traders, the pertinent question is no longer whether markets believe in any reopening at all. It is whether the oil-and-inflation overhang dissipates quickly enough to restore rate-cut expectations before the ceasefire premium diminishes.

The post Bitcoin’s rebound may be fragile as Wall Street warns Hormuz disruption is not really over appeared first on CryptoSlate.