Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Bitcoin on-chain transactions decline significantly as corporate products influence price movements.

Bitcoin’s resurgence to approximately $71,000 has sparked a renewed bullish discussion regarding price, liquidity, and positioning. However, it has also revealed a less reassuring reality within the network itself.

The fee market has seen minimal movement.

In a market that still views on-chain congestion as an indicator of genuine demand, this discrepancy warrants more focus than yet another summary of macroeconomic factors or ETF inflow trends.

Related Reading

Related Reading

Bitcoin’s rebound looks like a trap and Wall Street knows it – as real Hormuz threat may not be over

Financial institutions and energy analysts anticipate a slower recovery in oil supplies, maintaining inflation and Federal Reserve risks for Bitcoin.

Apr 8, 2026 · Gino Matos

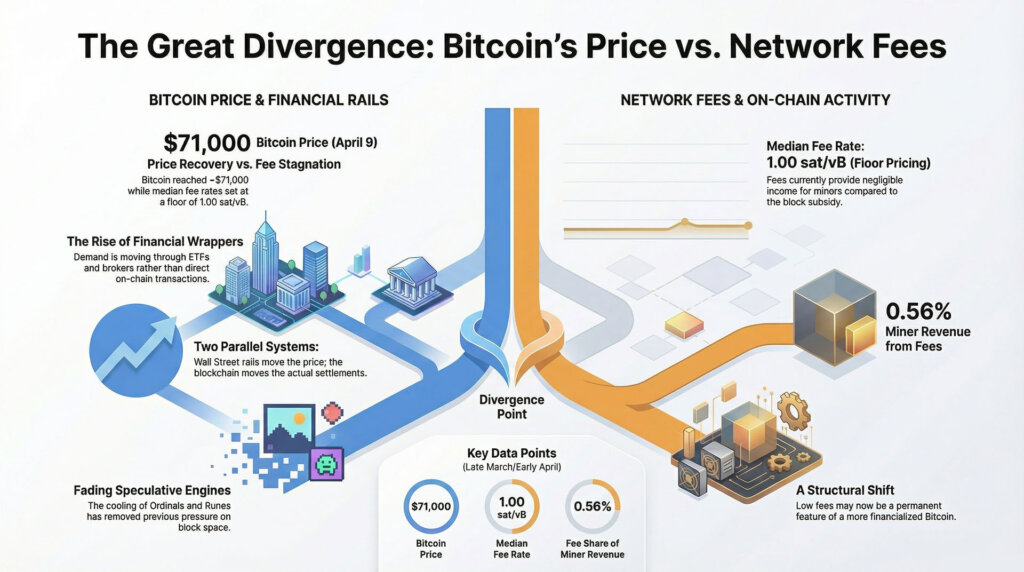

On CryptoSlate’s Bitcoin price page, BTC was last recorded at $70,990 on April 9, reflecting a decline of 0.86% over the past 24 hours, an increase of 6.11% over the last week, and a rise of 0.85% over the past 30 days.

The price has evidently bounced back from the lower end of its recent range, while the base layer appears calm, inexpensive, and uncrowded.

This disconnect indicates something significant about where this movement is genuinely occurring. Increased Bitcoin demand is being manifested through financial instruments, brokerage channels, and ETF mechanisms rather than through users vying for block space on-chain.

The price movement can still be sustainable under this arrangement. However, the signal it conveys is distinct.

A recent Bitcoin block space report covering March 19 to March 26 indicated that the median fee rate began at 1.13 sat/vB and remained at 1.00 sat/vB for the remainder of the week. In practical terms, this represents a floor price.

Users were still able to secure confirmations without paying a premium for limited space. Across 1,028 blocks, the report recorded only 18.03 BTC in total fees, or approximately 0.0175 BTC per block.

Even more notable, these fees constituted just 0.56% of miner revenue for the week, compared to 3,212.5 BTC from subsidies.

Price has recovered, while the fee market still looks half asleep

These figures are unusually low for a market trading around $71,000. Previous cycle logic led the market to expect that a rising Bitcoin price would coincide with busier blocks, increased competition for inclusion, and a fee market that begins to rise before most participants notice.

This reflex continues to influence how many crypto participants perceive demand. The current market is conveying a different message.

Price can recover even while on-chain urgency remains subdued.

One reason the fee market appears so muted is that Bitcoin has already lost one of the speculative demand drivers that previously distorted block-space pricing in earlier phases. Ordinals and other inscriptions once generated a noticeable surge of non-monetary demand for inclusion, while the Runes launch briefly created a similar effect on a larger scale around the 2024 halving.

This impulse has significantly diminished. The chain is no longer experiencing the same inscription-driven rush for block space, indicating that today’s low-fee environment is not merely a narrative about healthy efficiency or subdued user activity.

It also reflects the lack of a category that had previously inflated transaction volumes and exerted pressure on fees.

Related Reading

Related Reading

Bitcoin fees up more than 2000% since August due to renewed interest in Ordinals

Bitcoin Ordinals are experiencing renewed interest following their recent listing on Binance.

Nov 10, 2023 · Oluwapelumi Adejumo

This context clarifies why a rebound in BTC can occur alongside such a weak fee environment. Earlier in the cycle, Ordinals, inscriptions, and later Runes provided miners with an additional revenue stream and offered observers a reason to interpret mempool congestion as evidence of growing demand.

Currently, that support appears considerably thinner. The speculative activity that once congested the chain has diminished, leaving Bitcoin more reliant on either organic settlement demand or price-driven financial flows to carry the load.

In this regard, it is also about what has already exited the scene.

Part of this dynamic arises from the fact that the channels facilitating demand have evolved. A buyer utilizing a spot ETF, a brokerage product, or a treasury vehicle can inject capital into Bitcoin exposure without creating the same base-layer impact as a user transferring coins directly across the chain.

This distinction has become increasingly significant as Bitcoin access has become more financialized. Farside’s daily ETF flow data indicated a $471.4 million inflow on April 6, followed by outflows of $159.1 million on April 7 and $124.5 million on April 8.

The daily fluctuations were relatively modest, yet the overarching point is that flows through these financial instruments remain an active conduit for demand. Spot Bitcoin ETFs recorded $1.3 billion in net inflows for the month, marking the first positive month since October.

This represents the underlying mechanism behind the current divergence. Bitcoin demand is being divided across two systems.

One system influences price through funds, advisory platforms, and brokerage access. The other system facilitates transactions through the blockchain itself.

At present, the first system appears more active than the second. This leaves the fee market appearing lethargic even as the asset itself gains altitude.

The outcome is a rebound that appears bullish on screens, while the network’s own pricing of block space remains subdued. This combination carries a different implication than a comprehensive on-chain revival.

It suggests that the recovery has widespread distribution through financial channels, while direct pressure on Bitcoin’s settlement layer remains limited. For anyone still interpreting mempool congestion as a straightforward proxy for demand, the current situation serves as a reminder that the market structure surrounding Bitcoin has evolved more rapidly than many of the instincts people continue to apply to interpret it.

Glassnode’s April 1 weekly market note characterized Bitcoin as rangebound between $60,000 and $70,000 and noted that spot demand was showing early signs of absorption, while still lacking the conviction necessary for a sustained breakout. Glassnode also highlighted dense overhead supply between $80,000 and $126,000.

This range framework aligns well with the current divergence. Bitcoin has rebounded, yet the fee market has not adjusted to indicate widespread urgency, significant settlement demand, or a sudden rush for base-layer access.

Related Posts

Infographic showing divergence between Bitcoin price and on-chain activity, with price near $71K while network fees, miner revenue, and transaction demand remain subdued, highlighting a structural shift toward financialized demand over blockspace usage.

Infographic showing divergence between Bitcoin price and on-chain activity, with price near $71K while network fees, miner revenue, and transaction demand remain subdued, highlighting a structural shift toward financialized demand over blockspace usage.

Low fees point to where demand is landing, and to what miners still are not getting paid for

A separate report referencing Glassnode data on March fee activity indicated that Bitcoin’s 30-day simple moving average for daily transaction fees had decreased to 2.5 BTC per day in March 2026. The article described this as the lowest level since March 2011.

The precise historical context requires caution until the underlying primary chart is verified directly, yet the directional message aligns with the broader evidence. Fee conditions have tightened significantly, and they have remained tight even as BTC regained ground.

This compression creates a crucial divide between price strength and network monetization. Users benefit from a more accommodating chain. Miners receive very little additional revenue from transaction demand.

Following the halving, this revenue mix carries more significance than it did when the subsidy was contributing more substantially. The March 19 to March 26 block space report clearly quantified the issue, with fees making up just 0.56% of miner revenue for the week.

For miners, a rally that does not trigger a fee response still benefits through price, while leaving the network’s internal revenue base largely unchanged.

The distinction becomes clearer when Bitcoin is viewed as both an asset and a network, with each side expressing demand in different manners. The asset side gains from ETF adoption, advisory access, treasury accumulation, and improved risk appetite.

The network side benefits from actual users, transfers, settlements, and transactions that compete for limited capacity. These two layers can reinforce one another.

They can also diverge for significant periods. That is the current market situation.

There is also a practical aspect to the current setup. A calm mempool does not automatically imply weak Bitcoin.

This suggests that the rebound provides less evidence of renewed on-chain intensity than the price alone might suggest. A base-layer fee response would indicate that financial demand was spilling over into actual settlement competition.

In the absence of that response, a different interpretation becomes more central: one in which Wall Street distribution is doing more of the immediate lifting than users transacting natively on-chain.

This external-world interaction gives the current divergence its explanatory significance. Bitcoin is increasingly integrated into mainstream financial systems.

Morgan Stanley has recently launched a low-fee spot Bitcoin ETF, and Charles Schwab is preparing for direct spot Bitcoin and Ethereum trading by mid-2026. The access channels surrounding Bitcoin continue to expand.

As they expand, price can move along those channels long before the mempool indicates a similar demand pulse.

Related Reading

Related Reading

Morgan Stanley’s new Bitcoin ETF buys 430 BTC on debut, raising pressure on BlackRock’s IBIT

MSBT’s strong debut adds a new fee and distribution threat to the spot Bitcoin ETF race.

Apr 9, 2026 · Oluwapelumi Adejumo

The next test sits in the fee market, the miner revenue mix, and whether price strength spreads into actual settlement demand

The immediate question is whether the current divergence is temporary or structural. There are valid arguments on both sides, and the upcoming weeks should help clarify the range of plausible outcomes.

The first scenario is a continuation of the current trend. ETF and brokerage demand continue to support the price; Bitcoin remains near the upper end of its recent range, and fee rates stay close to the floor.

This would strengthen the argument that this rebound is primarily driven by wrapper-led flows rather than a widespread return of native transaction demand. It would also reinforce the notion that price can recover through distribution and access to capital, while the chain’s fee market remains tranquil.

The second scenario involves a catch-up move in block-space demand. If the price recovery begins to translate into actual transaction competition, the market should start to observe higher fee estimates, deeper backlogs, increased pressure in the mempool, and a larger fee share in miner revenue.

This shift would alter the interpretation of the rally. It would imply that the movement is transitioning from exposure to usage, which would provide the recovery with a different kind of sustainability.

The third scenario would position the current divergence more as a warning than a curiosity. If ETF flows decline again, price falls back into the lower half of Glassnode’s recent range, and fee conditions remain weak, the market will have stronger grounds to view the rebound as a positioning move that never evolved into broader transactional demand.

In that context, the mempool’s quietness would cease to appear incidental and start to seem diagnostic.

A fourth scenario is more closely related to miner economics than price direction. If fees remain this low while miners continue to operate in a post-halving environment, focus will shift to how the network is being monetized.

CoinShares’ Q1 2026 mining report characterized the final quarter of 2025 as the most challenging quarter for miners since the 2024 halving, with a sharp price decline and near-record hashrate impacting margins. A prolonged period of low fees would maintain that pressure in focus.

Price appreciation is beneficial, while a broader fee contribution would be even more advantageous.

This is why the fee market deserves to be at the forefront of the current Bitcoin discussion. A move back toward $71,000 is significant.

It also raises an important question. Where, precisely, is the demand becoming tangible?

At this moment, the most compelling answer is that demand is materializing in financial products more rapidly than it is within Bitcoin’s own block space.

This carries a measured but crucial implication for how this market should be understood. The rebound has gained momentum through the channels Bitcoin has sought to penetrate for years: funds, advisers, brokers, and mainstream financial systems.

The blockchain itself has yet to demonstrate the same urgency in its pricing of access. For anyone observing Bitcoin as both a monetary asset and a network, that gap serves as the signal.

The market has advanced. The chain has barely reacted.

The next round of evidence will determine whether that calm finally breaks or whether Bitcoin’s most potent demand engine now exists one layer removed from Bitcoin itself.

The post Bitcoin on-chain activity is a ghost town with price being controlled by corporate products appeared first on CryptoSlate.