Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

With just a few hours remaining, bitcoin has declined 22% in the first quarter, following a 25% decrease in the last quarter of 2025.

What’s next for bitcoin after a challenging six months (Getty images)

What’s next for bitcoin after a challenging six months (Getty images)

Key points:

- While it has shown better performance since the onset of the Iran war, bitcoin has lagged behind U.S. equities for almost six months, marking its longest documented period of underperformance compared to the S&P 500.

- Analyst Mark Connors suggests that bitcoin’s prolonged lag and prior deleveraging may pave the way for a recovery, although he contends that the timing will heavily depend on developments in geopolitical risks and energy markets.

Bitcoin’s decline in the first quarter concluded an atypical duration: nearly six months of underperformance against U.S. equities, a situation without precedent.

Related Posts

“That’s never occurred,” remarked Mark Connors, founder of Risk Dimensions, referencing data that indicates bitcoin has consistently lagged behind stocks since early October. This trend has prompted new inquiries into whether the asset is acting more like a risk asset than a hedge.

Bitcoin decreased by approximately 22% in the first quarter of 2026, following a 25% drop during the last three months of 2025. In contrast, the S&P 500 experienced a significantly smaller decline, resulting in a considerable performance disparity. Connors noted that the length of this gap, rather than merely its magnitude, is notable. Previous downturns have been sharper but shorter.

This weakness coincided with broader market challenges. U.S. equities recorded their worst quarter in four years, with the Nasdaq down over 10% from recent peaks. The combined drop in both stocks and cryptocurrency wiped out much of the surge that followed the 2024 election.

Progress on policy matters has been inconsistent. A new SEC chair has facilitated a pathway for additional crypto ETFs, and legislators have pushed forward initiatives like the GENIUS Act. Additionally, Trump signed an executive order in August aimed at simplifying the inclusion of alternative assets like cryptocurrencies, private equity, and real estate in 401(k) plans, which the Labor Department proposed a rule regarding on Monday.

March Indicates Signs of Stability

Despite the disappointing quarter, bitcoin performed better in March than many had anticipated.

The escalation in early March between the U.S. and Iran sent tremors through global markets, pushing oil prices and the U.S. dollar higher as investors responded to supply uncertainties and increasing costs.

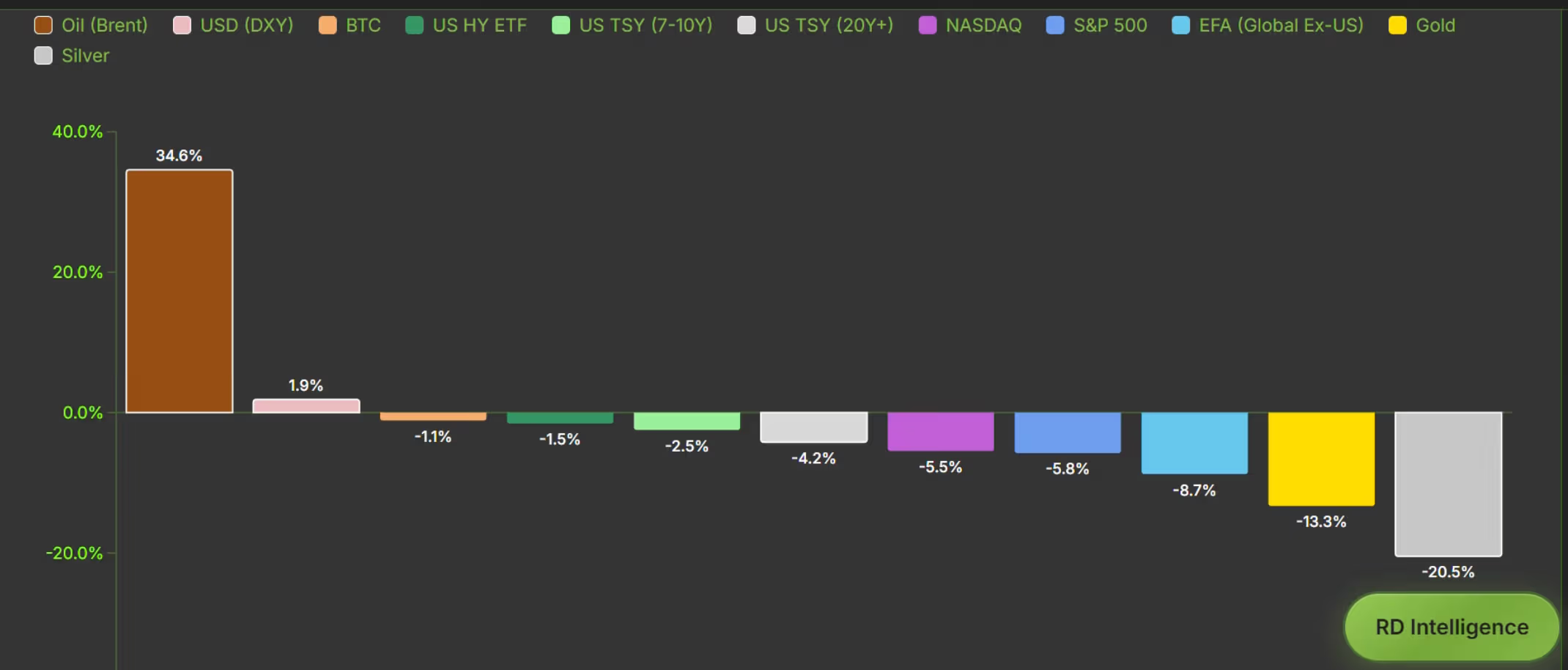

This volatility led to significant fluctuations across asset classes. Gold, which is frequently regarded as a safe haven, experienced dramatic swings as margin calls and urgent liquidity requirements compelled selling from both institutional investors and sovereign entities. The extent of this movement was among the most severe short-term disruptions in decades.

Conversely, bitcoin did not face the same degree of forced selling. The cryptocurrency increased by about 1% in March, while gold saw an 11% decrease during the same timeframe. “It really held its ground,” Connors noted.

(Source: Risk Dimensions)

(Source: Risk Dimensions)

He attributes this stability partly to earlier liquidations that eliminated leveraged positions. Bitcoin’s capacity to transfer swiftly across borders may also reduce forced selling compared to tangible assets.

Outlook: A “Coiled Spring”?

Looking forward, Connors highlighted bitcoin’s prolonged phase of underperformance against equities as a potential factor influencing future developments. Rolling 63-day data indicates that the asset has been trailing the S&P 500 since October — the longest such span on record — an imbalance that has typically preceded reversals.

If this trend persists, bitcoin might be entering a stage where relative weakness transitions into renewed demand, particularly as macroeconomic pressures related to debt and currency expansion continue to accumulate.

The timing, however, may be more dependent on geopolitical factors than market structure. The course of the Iran conflict and its effects on energy markets, liquidity, and global risk appetite could dictate how swiftly sentiment changes.

“It’s either two months or two years,” Connors stated.