Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Visa and Coinbase are preparing for AI advancements, each developing distinct online ecosystems.

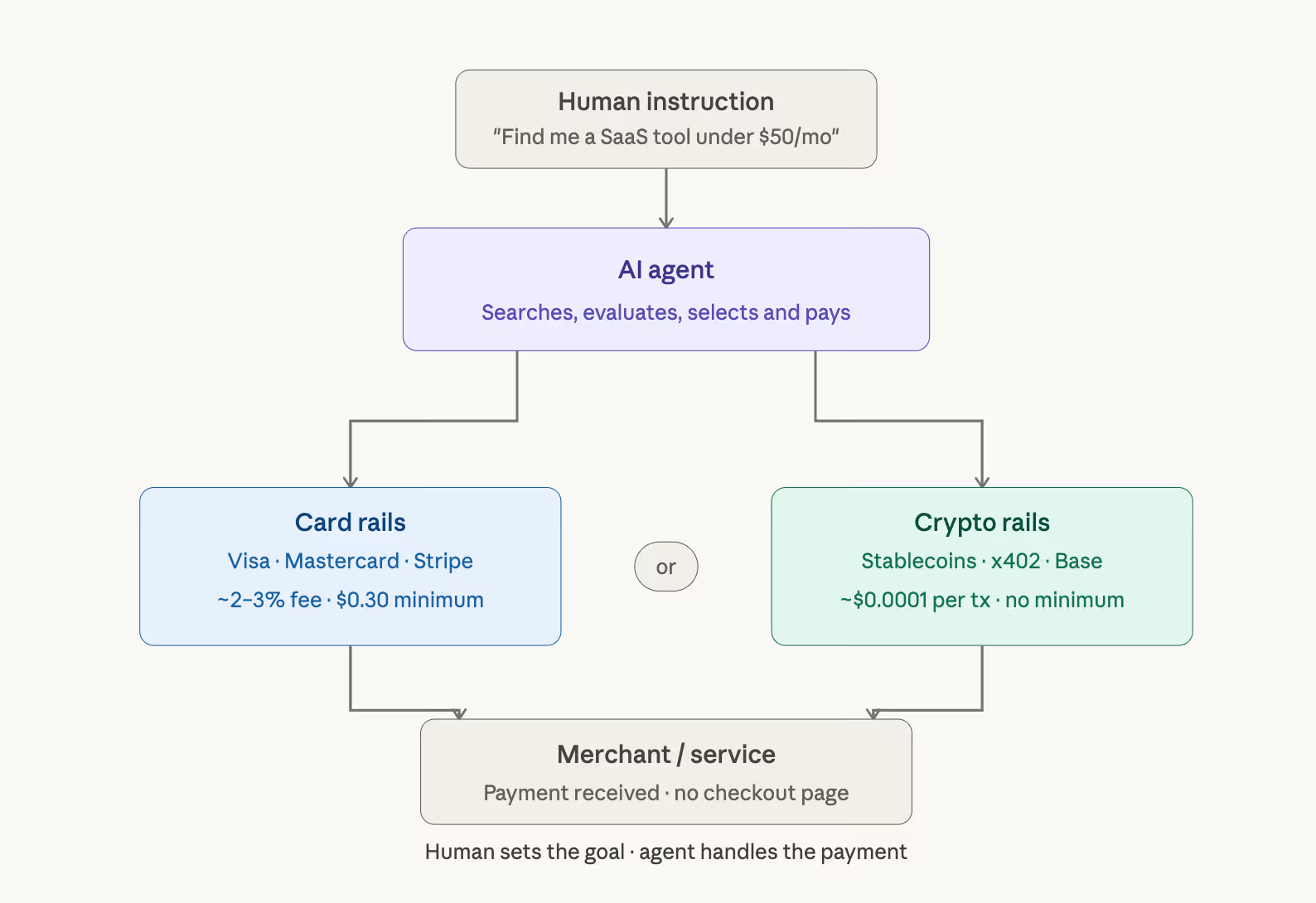

The forthcoming trillion-dollar payments network will not feature a checkout page. No card details, no CVV, no human intervention at the keyboard. Merely machines transacting with machines, thousands of times per second, for mere fractions of a cent.

How do AI Agents function and how do they facilitate payments? (Agentic commerce (Xavi Torrent/Getty Images))

How do AI Agents function and how do they facilitate payments? (Agentic commerce (Xavi Torrent/Getty Images))

Key points:

- Leaders in the crypto and AI sectors contend that self-sufficient AI agents will soon execute far more online transactions than humans, preferring crypto wallets over traditional bank accounts due to their ability to circumvent identity verification and compliance challenges.

- Advocates assert that stablecoins and frameworks such as Coinbase’s x402 enable economically viable sub-cent, high-frequency machine-to-machine payments in ways that conventional card networks, with minimum fees around 30 cents, cannot achieve.

- Although current volumes for x402 are minimal and contain a considerable amount of artificial activity, established card networks like Visa and Mastercard are launching their own AI-agent payment solutions, indicating a potential division between regulated human transactions on card systems and stablecoin-based payments for AI agents.

Your AI just processed several payments as you read that headline. You authorized none of them. Visa facilitated none of them. And if the most optimistic figures in the crypto sector are accurate, that is not an error — it represents the forthcoming direction of the internet economy.

Coinbase’s founder Brian Armstrong anticipates that the number of AI agents engaged in online transactions will soon surpass that of humans. Binance’s founder Changpeng Zhao went further, forecasting that agents will execute one million times more payments than individuals, all in cryptocurrency. These statements were made on the same day last week and generated significant discussion in the crypto community.

The primary argument is structural.

AI agents cannot open bank accounts because financial institutions necessitate identity verification that software cannot supply, while a crypto wallet solely requires a private key. There is no KYC, no compliance assessment, no delays — and this disparity is what Armstrong highlighted.

However, the wallet issue is only part of the equation. The remaining aspect is economic.

Agents do not shop like humans. When an AI agent is performing a task — such as gathering information, coordinating a supply chain, or compiling a report — it may utilize dozens of specialized APIs within a single session.

Related Posts

Each request might only be worth fractions of a cent, as it pays for GPU computing time, real-time data feeds, web scraping services, or the hiring of a sub-agent for translation. None of these transactions align with what Visa or Mastercard were intended to handle.

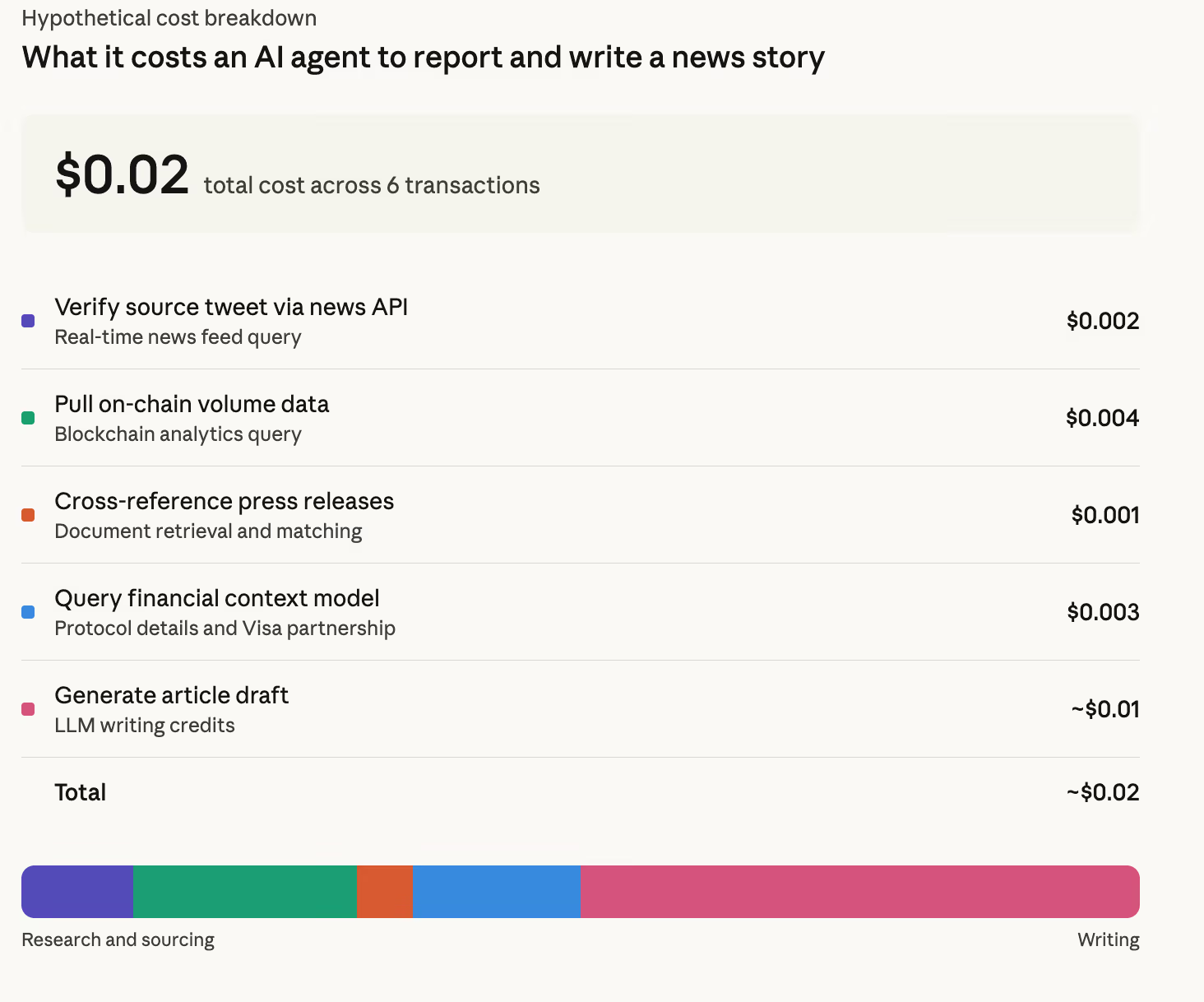

Imagine that this article was composed by an agent, commissioned by a “chief” agent at CoinDesk aiming to enhance the site’s authority.

To create it, that agent would have consulted a real-time news API to confirm Armstrong’s tweet ($0.002), retrieved on-chain data to look for volume figures ($0.004), cross-checked press releases ($0.001), and queried a financial context model for Visa protocol specifics ($0.003). It would ultimately produce the article at an additional cost, compensating another AI tool to actually write the piece.

The overall expense of reporting is under two cents with six transactions, based on current rates offered by protocols such as x402.

In contrast, Stripe’s minimum processing fee for a single transaction is approximately $0.30. Executing those six payments through a card network would result in costs exceeding 100 times the value of the payments themselves.

A human editor reviewing and publishing the content might subsequently incur charges from a sub-agent that managed SEO enhancements, another that conducted plagiarism assessments, and another that formatted for CMS software. Each micropayment is economically unfeasible on traditional card networks but trivial on-chain.

This forms the foundation of x402, Coinbase’s open payment protocol that integrates stablecoin payments directly into HTTP requests — allowing an agent to access a paywall, pay in USDC, and proceed with its task within the same interaction, without requiring human involvement. Cloudflare, Circle, AWS, and Stripe are all supporters of this initiative. Google’s open agent payments standard includes x402 as a settlement layer.

Every sector characterized by high-frequency, low-value data exchanges becomes a potential candidate.

In healthcare, an agent managing a patient’s insurance claim pays for each document fetched from a medical records API. In logistics, a procurement agent bids for freight slots across numerous carriers in real time, settling the winning bid instantly. In media, AI crawlers compensate for each article indexed instead of negotiating bulk licensing agreements. In finance, a trading agent pays a specialized model fractions of a cent for each risk signal utilized.

However, a caveat exists: the infrastructure is ahead of the demand.

CoinDesk reported this week that x402 currently processes approximately $28,000 in daily volume, with Artemis indicating that about half of observed transactions are artificial activity rather than legitimate commerce. The merchants x402