Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Treasurys, private credit, and commodities are propelling growth, yet a majority of tokenized assets are still detached from DeFi markets.

Key points:

Related Posts

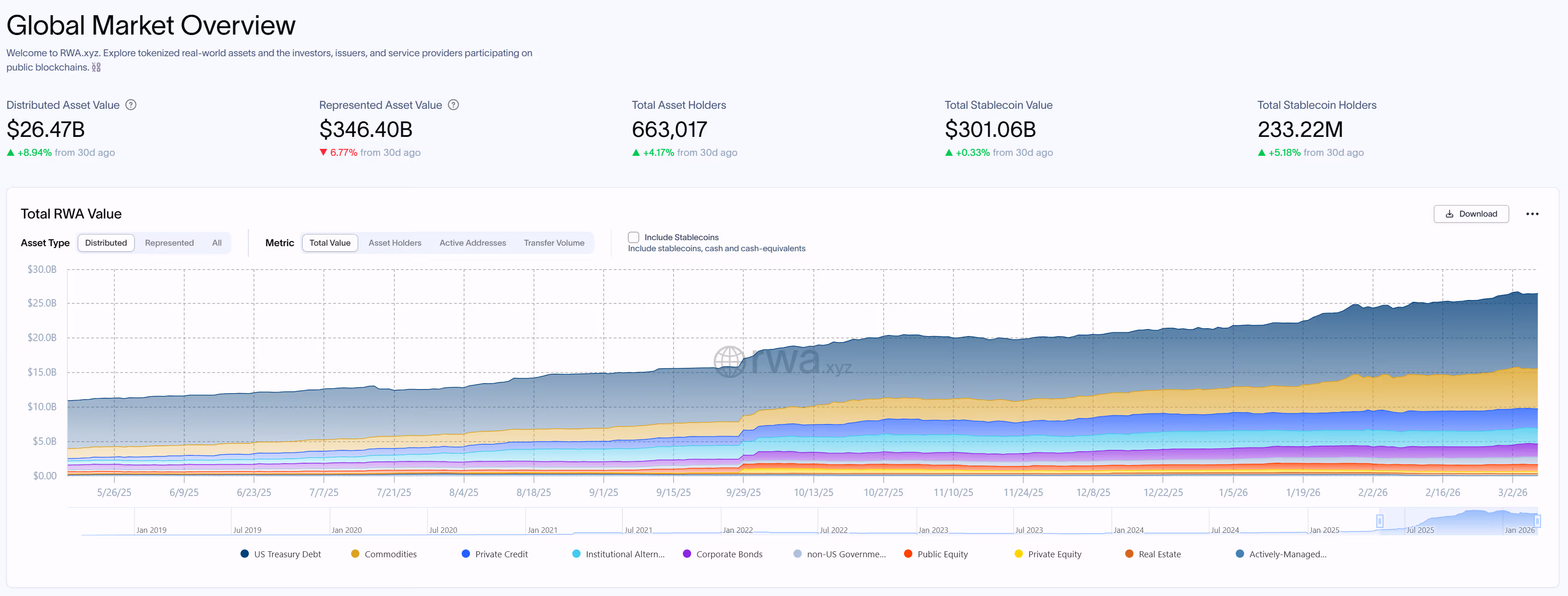

- Tokenized real-world assets, excluding stablecoins, have risen to over $25 billion onchain, nearly quadrupling within a year, with six categories now surpassing $1 billion each.

- A significant portion of the growth represents substantial, infrequent institutional allocations rather than active secondary trading, as issuers focus on capital formation and fundraising efficiency over liquidity.

- Approximately 12% of the roughly $8.5 billion in RWA-backed stablecoins is utilized in DeFi, leaving the majority of assets constrained by compliance hurdles and raising concerns about the potential for tokenization to connect with permissionless finance.

Six asset classes have crossed the $1 billion mark onchain, yet only 12% of RWA-backed stablecoin supply has engaged with DeFi protocols.

Tokenized real-world assets, excluding stablecoins, have surpassed $25 billion in onchain valuation, nearly quadrupling from about $6.4 billion the previous year, according to information from RWA.xyz.

(RWA.xyz)

(RWA.xyz)

This achievement, along with ongoing growth as RWAs reach the $20 billion milestone by the end of 2025, marks a transition from initial experimentation to institutional-grade deployment. Asset managers such as BlackRock, Fidelity, and WisdomTree have introduced tokenized fund offerings in the past year, while the number of tokenized U.S. Treasury products has increased from 35 to over 50, based on data from Nexus Data Labs.

According to RWA.xyz data, six tokenized asset categories have now surpassed the $1 billion threshold: U.S. Treasuries, commodities, private credit, institutional alternative funds, corporate bonds, and non-U.S. government debt.

Issuance exceeds integration

Nevertheless, much of the activity is driven by asset issuance rather than active trading.

Despite the increase in supply, much of the activity is indicative of asset issuance over active trading. Onchain transfer data reveals that many of the largest RWA transactions cluster around $10 million per transfer, a trend that aligns with institutional allocation batching rather than ongoing market engagement.

A survey from tokenization platform Brickken conducted in February 2026 supports this observation: 53.8% of tokenized asset issuers identified capital formation and fundraising efficiency as their primary reasons for tokenization, while only 15.4% mentioned liquidity.

Even when assets transition onchain, the majority remain segregated from decentralized finance.

6/7

The twist nobody talks about:

RWA-backed stablecoin supply = ~$8.5B

Only $1B (11.8%) is actually deployed in DeFi

88% sits idle because of KYC/whitelisting walls

Permissionless assets (reUSD, etc.) hit 96%+ utilization

Composability is the next unlock for RWA

h/t… pic.twitter.com/gpbyRl9CD0

— Diego | Take Profits (@0xTakeProfits) March 7, 2026

Nexus Data Labs estimates that approximately $8.49 billion in RWA-backed stablecoin supply exists, but only around $1 billion, or 11.8%, is currently utilized within DeFi protocols.

The remaining 88% remains outside onchain lending and trading systems, primarily due to compliance mandates, including KYC checks, transfer limitations, and whitelisting.

This disparity highlights the key question for the sector as it moves into the latter half of the year. The supply of tokenized assets is expanding rapidly enough that some forecasts predict the market will exceed $400 billion by the end of the year.

Whether these assets stay confined within permissioned frameworks or start to integrate with the composable collateral, lending, and trading systems that characterize DeFi will likely influence whether tokenization develops as a complementary settlement layer for traditional finance or evolves into something fundamentally different.