Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

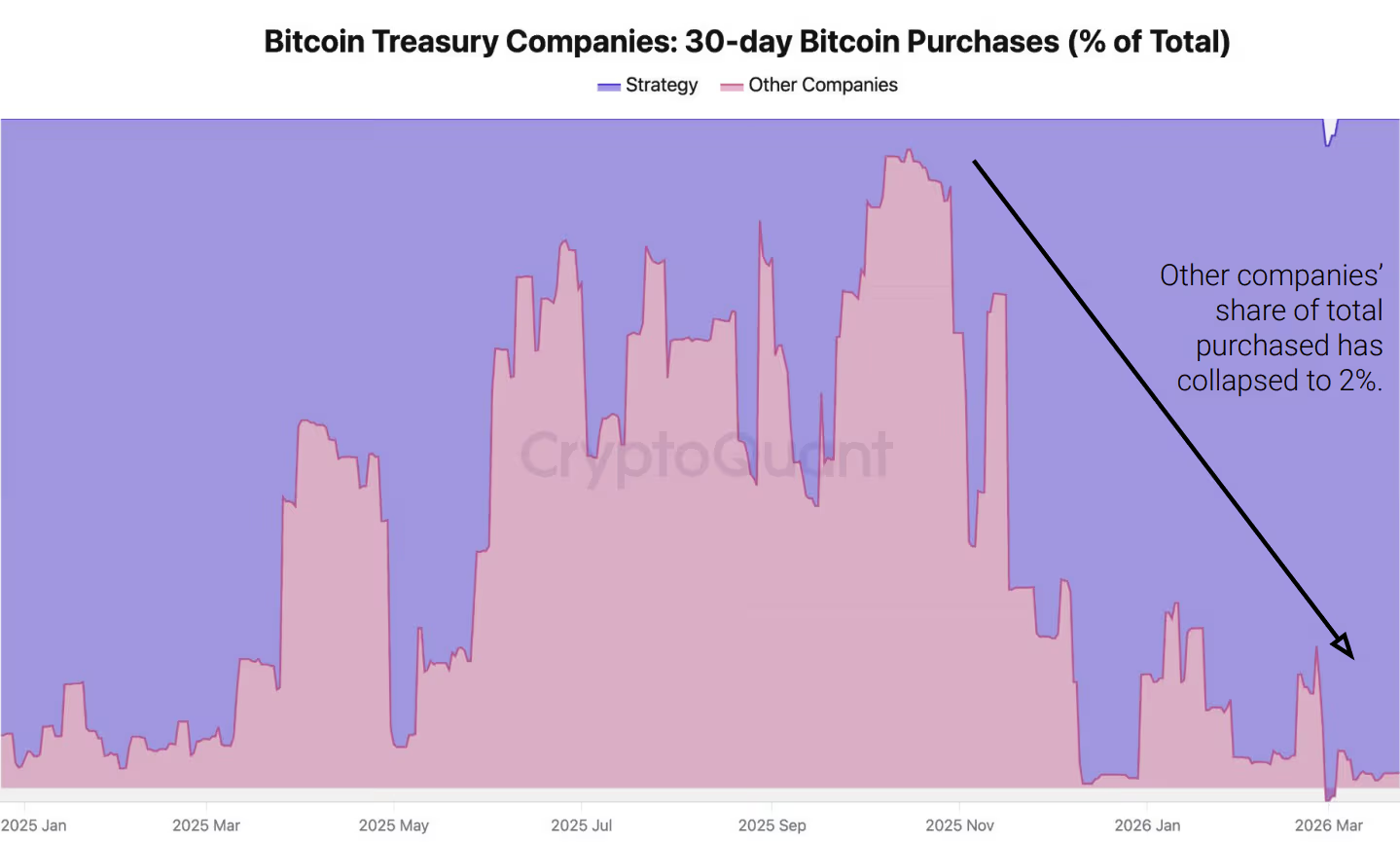

Strategy has accounted for almost all recent BTC digital-asset treasury acquisitions, with the share of other firms plummeting from 95% to around 2%, according to data from CryptoQuant.

What to know:

- Corporate bitcoin acquisitions have largely consolidated within one entity, Strategy, which obtained about 45,000 BTC over the last month, while all other treasury firms collectively acquired merely around 1,000 BTC.

- Strategy currently possesses approximately 76% of all bitcoin held by treasury firms, presenting a concentration risk in a market once characterized by a broader institutional interest in the asset.

- The decline in bitcoin prices from above $110,000 in mid-2025 to below $70,000 today has left numerous treasury buyers significantly disadvantaged, hindering the overall corporate acquisition model, even as Strategy continues to gather assets and amass a substantial cash reserve to fulfill obligations.

Corporate bitcoin acquisitions have narrowed to a single entity, and the market expectation of a broadened institutional base for the asset has instead become a concentration risk.

According to a recent CryptoQuant report, Strategy, the world’s largest corporate bitcoin holder, acquired approximately 45,000 BTC in the last 30 days, marking its quickest accumulation rate since April 2025.

(CryptoQuant)

(CryptoQuant)

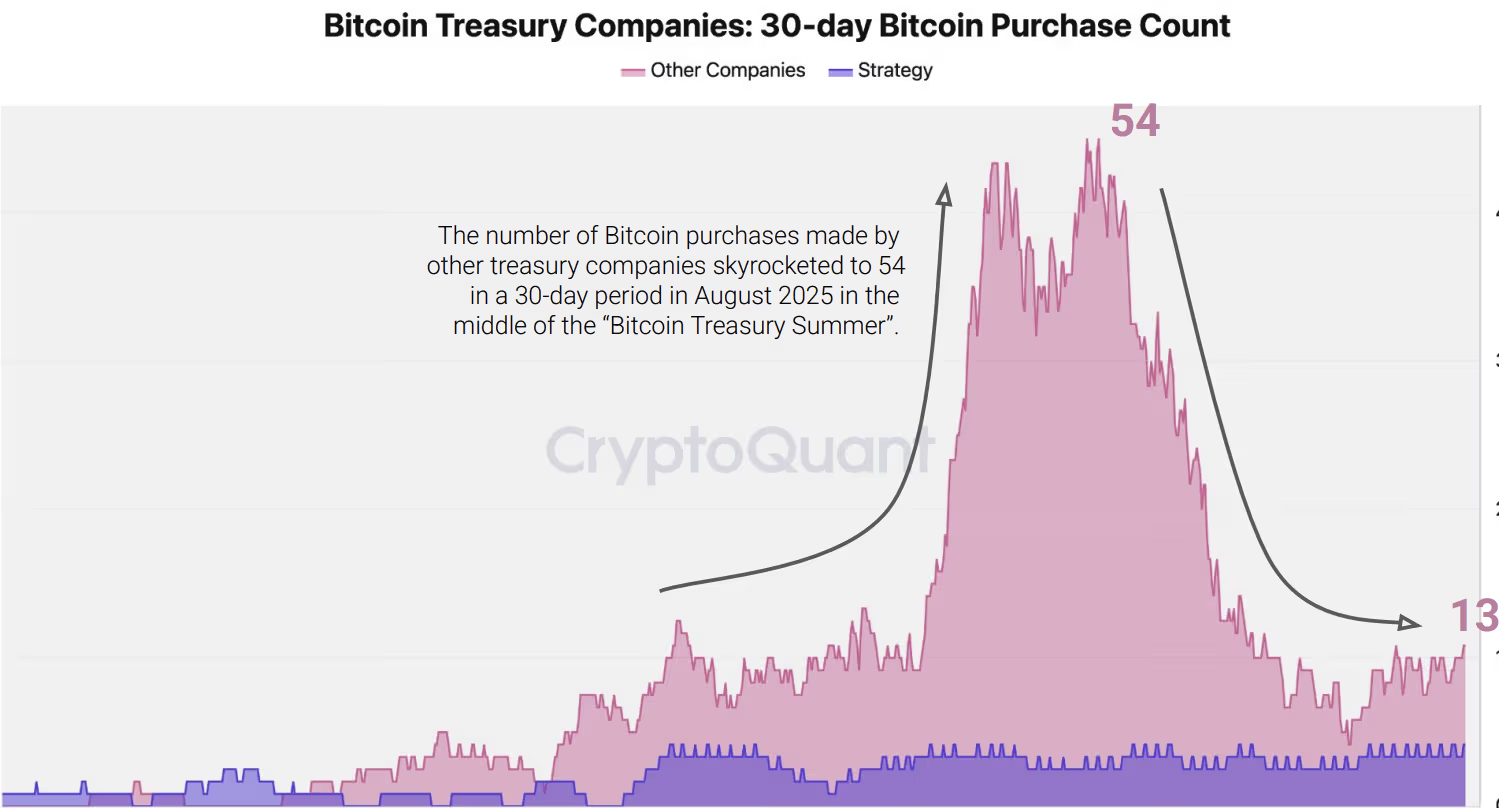

In contrast, other treasury firms combined managed to acquire about 1,000 BTC during the same timeframe, reflecting a 99% drop from a peak of 69,000 BTC recorded in August of the previous year. Their portion of total acquisitions has drastically decreased to 2%, down from 95% at the peak of the market.

(CryptoQuant)

(CryptoQuant)

According to CryptoQuant data, Michael Saylor’s Strategy now controls approximately 76% of all bitcoin held by treasury firms.

Related Posts

The data corroborates concerns raised by Galaxy Digital last summer. In a report published in July, Galaxy asserted that the digital asset treasury company model was primarily a liquidity derivative that thrived as long as equities traded at a premium compared to their underlying bitcoin holdings.

When those premiums diminished, the cycle would reverse: lower prices would reduce net asset values, eliminate the equity premium, and render share issuance dilutive instead of accretive.

This scenario has unfolded almost precisely as forecasted.

During July and August of 2025, the period when these firms were accumulating, BTC traded above $110,000. Currently, it is trading below $70,000, based on CoinDesk market data, as it gradually recovers from the crash on October 10.

Companies that made aggressive purchases near the peak of the cycle, such as Metaplanet and Nakamoto Holdings, reported average acquisition costs exceeding $107,000 as of December, according to Galaxy’s analysis, placing them at a significant disadvantage at current price levels.

Strategy has taken measures to protect itself, revealing in December a $1.44 billion cash reserve aimed at eventually building this up to cover 24 months’ worth of dividend and interest obligations.

This defensive strategy has not curtailed its purchasing activity. However, CryptoQuant’s data indicates that no other company is matching its pace, and most have ceased their efforts.

The outcome is a much more concentrated demand profile than what the market had initially anticipated.

At Bitcoin Asia in Hong Kong last summer, treasury firms promoted themselves as a scalable new category of corporate buyers capable of absorbing bitcoin supply and outperforming passive investments.

For now, that vision has become limited to a single balance sheet.