Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Jefferies analysts caution that the rise of stablecoins may impact the profitability of conventional banks.

The utilization of digital dollars in payments and cryptocurrency markets could gradually divert deposits from banks, compelling financial institutions to pursue more expensive funding, according to a recent report by Jefferies.

Key points:

- A report from Jefferies indicates that while stablecoins are not expected to trigger an immediate rush on U.S. bank deposits, they could gradually diminish bank profits as digital dollar adoption increases.

- The firm projects that the rise of stablecoins might result in a 3% to 5% decrease in core deposits over five years, which could lead to a roughly 3% reduction in average bank earnings as funding expenses increase and fee income faces challenges.

- Although the GENIUS Act’s prohibition on yield for passive stablecoin holders lessens the risk of a sudden deposit exodus, the report cautions that banks need to innovate their own tokenized payment solutions to avert a continuous profitability decline.

Competition is intensifying between cryptocurrency companies and traditional banks over stablecoins, with Jefferies analysts noting that they could consistently pressure bank earnings as the usage of digital dollars expands.

While stablecoins are not poised to present an immediate existential threat to banks, Jefferies analysts anticipate a potential 3% to 5% core deposit runoff for banks over the next five years, likely increasing funding costs and impacting banks’ profitability.

According to analysts led by David Chiaverini, “The intermediate-term risk of gradual deposit runoff from emerging activity-based yield opportunities and payment use cases should not be overlooked.”

This “modest pressure” scenario may result in an estimated 3% decline in earnings for the average bank, the analysts stated.

It is clear why banks might be concerned about the growth of stablecoins, which are cryptocurrencies designed to maintain a consistent value and are often pegged 1:1 to fiat currencies such as the U.S. dollar or the euro.

Stablecoins are already commonly utilized in cryptocurrency trading; however, following the passage of the GENIUS Act last year in the U.S., the market is branching into payments, treasury management, and international transfers. By the end of 2025, supply is expected to reach $305 billion, marking a 49% increase from the previous year, while adjusted stablecoin transfer volume is projected to rise to $11.6 trillion in 2025, according to the report.

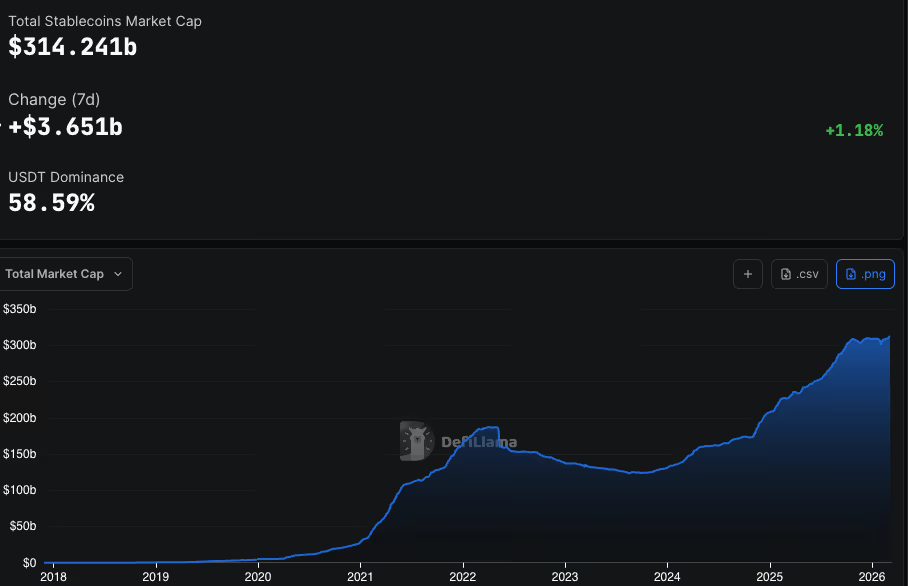

Currently, the total market capitalization of the stablecoin sector is approximately $314 billion, a rise from roughly $184 billion in 2022, based on DefiLlama data. Jefferies estimates that this could escalate to between $800 billion and $1.15 trillion over the next five years.

Stablecoin marketcap (DefiLlama)

Stablecoin marketcap (DefiLlama)

This growth is significant for banks, as stablecoins function as digital cash that operates continuously and integrates with decentralized finance platforms that provide yields exceeding most traditional bank accounts.

Related Posts

Bank of America CEO Brian Moynihan cautioned earlier this year that the overall banking system might be adversely affected by the “potential of $6 trillion in deposits” shifting towards stablecoins and related products offering yield-like returns.

The long-term concern

Jefferies’ primary assertion for stablecoins not posing an immediate threat is that the current U.S. market structure bill restricts their attractiveness as basic savings instruments, despite the uncertainty surrounding the bill’s passage.

“The CLARITY [act] would establish stablecoins as payment instruments, as opposed to savings vehicles, by addressing the ‘stablecoin yield loophole’ that remains open in GENIUS.”

The GENIUS Act, enacted in July 2025, prohibits regulated stablecoin issuers from providing yield directly to passive holders. This limitation diminishes the likelihood of a sudden shift away from checking and savings accounts.

Moreover, banks and other traditional financial entities are either introducing their own stablecoins or contemplating doing so to gain a competitive edge. Fidelity Investments has launched its initial stablecoin, the Fidelity Digital Dollar (FIDD). Bank of America’s Moynihan indicated that the bank would issue a stablecoin if Congress permits it, while the CEO of Goldman remarked that his bank has “a significant number of employees focused on tokenization and stablecoins.”

Nevertheless, the report emphasizes that the long-term risks should not be underestimated.

“We recognize the potential for activity-based rewards from stablecoin transactions, payments, and settlements, as well as incentives from DeFi staking and lending protocols to present a comparable risk to bank deposits.”

Which banks face heightened exposure to this risk?

Jefferies suggests that banks with larger shares of retail and interest-bearing deposits appear more vulnerable than custody banks or major institutions already investing in digital asset infrastructure.

“We consider WTFC, FLG, WBS, EGBN, and AX as the banks under coverage most at risk, given their substantial concentration of retail and interest-bearing deposits.”

Read more: Stablecoin market hits $312 billion as banks, card networks embrace onchain dollars