Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

In this week’s Crypto Long & Short Newsletter, Gregory Mall of Lionsoul Global discusses how ETFs have redirected a significant portion of bitcoin volatility into U.S. equity options markets.

(Giulia Squillace/ Unsplash+)

(Giulia Squillace/ Unsplash+)

What to know:

You are reading Crypto Long & Short, our weekly newsletter that provides insights, news, and analysis for professional investors. Sign up here to receive it directly in your inbox every Wednesday.

Hello readers,

Welcome to our institutional newsletter, Crypto Long & Short. This week:

STORY CONTINUES BELOWDon’t miss another story.Subscribe to the Crypto Long & Short Newsletter today. See all newslettersSign me up

- Gregory Mall on how ETFs have redirected a growing share of bitcoin volatility into U.S. equity options markets

- Key headlines institutions should monitor by Francisco Rodrigues

- Mid-cap assets show unexpected resilience in Chart of the Week

Thank you for being with us!

-Alexandra Levis

Expert Insights

When ETF options start influencing bitcoin

– By Gregory Mall, chief investment officer, Lionsoul Global

Related Posts

The introduction of U.S. spot bitcoin ETFs represented a significant turning point. The iShares Bitcoin Trust ETF (IBIT) quickly became one of the most rapidly growing ETFs in history, attracting tens of billions into a regulated framework. Less highlighted, yet equally crucial, is the subsequent swift growth of IBIT options.

In the past year, open interest in IBIT options has surged into the multi-billion-dollar range. During specific high-volume trading sessions, activity has approached levels typically seen on Deribit, the cryptocurrency futures and options platform. A substantial portion of bitcoin’s convexity is now located within U.S. equity options markets instead of offshore crypto exchanges.

This transition is significant as it alters the transmission of volatility.

From offshore leverage to onshore gamma

Historically, bitcoin volatility was primarily driven by offshore perpetual futures. Price movements were influenced by funding imbalances, leverage accumulations, and liquidation cascades.

ETF options introduce a distinct mechanism.

When investors purchase calls or puts on IBIT, dealers typically sell that optionality and hedge delta exposure. If dealers are short gamma, which is common when investors are net long options, they must buy as prices rise and sell as they fall. These hedging activities are inherently procyclical and can amplify underlying price movements.

Since IBIT holds actual bitcoin, hedging does not remain limited to the ETF itself. Arbitrage and creation and redemption activities transmit ETF positioning into the underlying market. Bitcoin increasingly engages in the same positioning mechanics that affect equity indices.

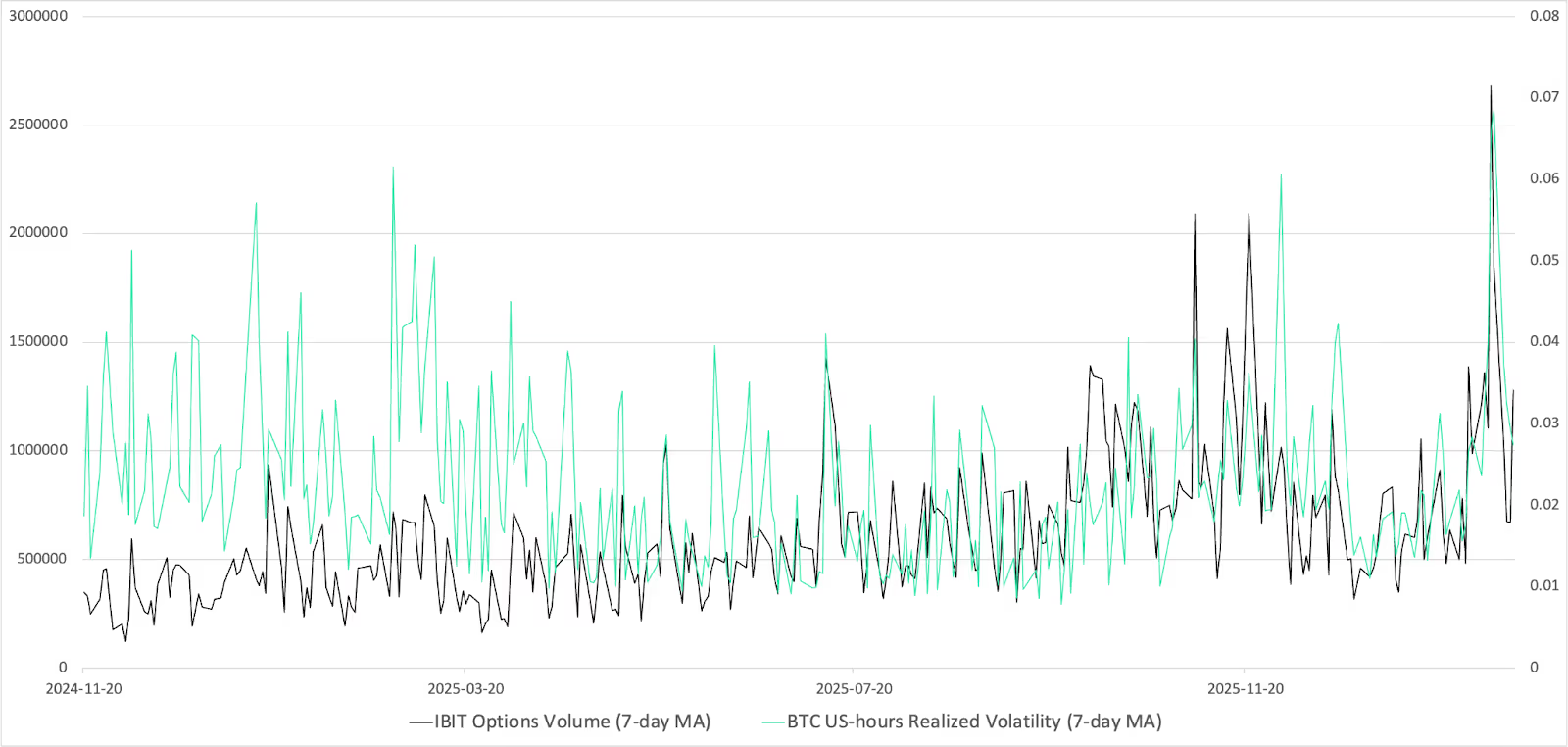

The structure of ETF options markets, where investors are generally net long options, indicates that dealers frequently hold short gamma during periods of high demand. This dynamic likely intensified during February, when volatility was low and crypto-native participants accumulated downside puts. Ongoing option purchases in a low-volatility environment leave market makers short convexity across both ETF and offshore venues. When spot prices drop, hedging flows can reinforce this feedback loop. In the graph below, we illustrate the movement of IBIT option volume and BTC U.S.-hours realized volatility, demonstrating a strengthened relationship in recent weeks.

Chart 1 illustrates the co-movement between IBIT option volume and BTC U.S.-hours realized volatility, showing that their relationship has strengthened in recent weeks. To formally assess this relationship, we perform a regression analysis of bitcoin realized volatility on lagged IBIT options volume while controlling for BTC funding rates, equity returns (Nasdaq Composite), implied volatility (CBOE Volatility Index, or VIX), short-term interest rate variations, and U.S. dollar fluctuations. The findings indicate that IBIT options trading activity is significantly correlated with BTC volatility, even after considering broader macroeconomic factors.

Chart 1: Movement of IBIT option volume and BTC U.S.-hours realized volatility