Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

In this week’s Crypto Long & Short Newsletter, Nilmini Rubin discusses the difficulties that both crypto and traditional markets face in establishing a combined, shared governance framework. Subsequently, Meredith Fitzpatrick examines how financial institutions need to fundamentally reassess AML risk as the lines between crypto and traditional finance blur.

(Yuri Krupenin/ Unsplash)

(Yuri Krupenin/ Unsplash)

What to know:

You’re reading Crypto Long & Short, our weekly newsletter providing insights, updates, and analysis for the professional investor. Sign up here to receive it directly in your inbox every Wednesday.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Nilmini Rubin discusses the challenge facing crypto and traditional markets in forming a hybrid, shared governance framework.

- Meredith Fitzpatrick examines how financial institutions must fundamentally reevaluate AML risk as crypto and traditional finance merge.

- Key headlines that institutions should focus on by Francisco Rodrigues.

- Maple loans surpass $1 billion in the Chart of the Week.

-Alexandra Levis

Expert Insights

Governance is the real Layer 1

By Nilmini Rubin, chief policy officer, Hedera

When Silicon Valley Bank failed in 2023, USDC temporarily lost its dollar peg as billions in reserves were locked in the bank. The repercussions were swift, halting markets, revaluing assets mid-transaction, and sparking a broader crisis of confidence. While regulators conduct stress tests on traditional markets, this incident revealed a new vulnerability where breakdowns in traditional finance can directly affect digital assets.

This situation raised essential questions about what occurs if risk transfers from crypto to traditional markets: who steps in, who bears the losses, and how is market confidence reinstated?

As blockchains increasingly support financial markets, the forthcoming phase of digital assets will be characterized not only by innovation but also by collective accountability. This accountability is influenced by the design of networks.

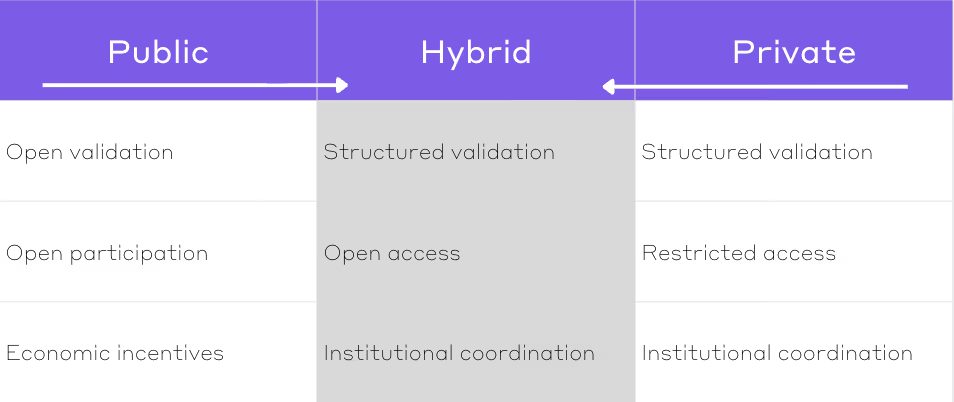

The false binary

For years, discussions surrounding blockchain were marked by a familiar dichotomy: public versus private networks.

Permissionless networks promote openness and resistance to censorship but may face difficulties with coordinated upgrades, regulatory compliance, or urgent interventions. Private systems prioritize control and adherence over neutrality and interoperability.

As institutional adoption grows, hybrid models are emerging as the favored approach.

Hybrid structures merge public verifiability with open participation and predictable governance, making them more appropriate for regulated scenarios and compliance frameworks that necessitate greater transparency and clearly defined roles. Coordinated accountability, rather than merely choosing between public or private, is the next significant challenge for blockchain.

Blockchain architecture is increasingly aligning with hybrid governance frameworks.

When governance meets crisis

In intricate systems, responsibilities are generally established before issues arise. Participants understand who holds authority, who takes on losses, and how emergencies are managed.

Blockchain networks should start with that level of transparency. When challenges arise due to sanctions enforcement, protocol malfunctions, or market crashes, effective governance becomes a significant test.

The industry has already witnessed early indicators. During the March 2020 market downturn, MakerDAO required urgent intervention after auction failures wiped out millions in value. The protocol managed to recover, but such incidents should not be allowed to happen frequently or at scale. In other instances, networks have employed coordinated forks to respond to hacks or unlawful activities, but only after the fact.

As tokenization grows, enhancing resilience will necessitate governance structures that foresee crises and delineate decision-making processes prior to events to effectively mitigate risks.

Putting governance to the test

Related Posts

Mature financial systems routinely stress-test their governance frameworks to ensure resilience well before disruptive moments occur.

Hybrid networks must incorporate that discipline on-chain. Governance stress testing clarifies roles, aligns incentives, and fortifies coordination under stress, aiding the industry in preparing for scenarios such as stablecoin volatility, regulatory changes, and AI-influenced governance dynamics.

Governance is the real Layer 1

Digital assets are redefining ownership and participation. The next challenge is applying that same innovation to governance.

The networks that will thrive will not necessarily be those with the largest number of tokens or the quickest transaction speeds. They will be the ones adept at governing effectively when the system faces pressure.

Headlines of the Week

– By Francisco Rodrigues

The crypto sector has continued to navigate the regulatory landscape this week, making strides into the mortgage market while also appearing to face restrictions on providing yields for stablecoin holdings. Other significant developments enhance trust in the industry, even amidst price declines.

- The latest text of the stablecoin yield in the crypto Clarity Act prohibits rewards for merely holding a stablecoin and limits approaches that would render it similar to a bank deposit.

- The U.K. government has instituted an immediate ban on crypto donations to political parties due to concerns over concealed foreign funding and inadequate traceability.

- Coinbase collaborates with Fannie Mae to provide crypto-backed mortgages to homebuyers: Coinbase is now partnering with Fannie Mae-approved Better Home & Finance Holding Co. to allow cryptocurrency holders to utilize their digital assets as collateral for down payments when purchasing homes.

- Tether engages a ‘Big Four’ firm to conduct a comprehensive audit of USDT reserves: Tether has enlisted a “Big Four” auditing firm to perform its first complete financial statement audit. The company has been providing periodic attestations of the assets backing its USDT stablecoin but has refrained from a full audit.

- Nearly 50% of all circulating bitcoin is currently underwater as long-term holders sell at a loss: Data indicates that almost half of all bitcoin in circulation is now valued less than its purchase price as capital flows supporting the market have reversed.

Expert Perspectives

The new financial order: updating TradFi risk for crypto

– By Meredith Fitzpatrick, partner and head of cryptocurrency, Forensic Risk Alliance

The merging of traditional finance and cryptocurrency is no longer a theoretical concept — it is a reality. Regulatory clarity in major jurisdictions is hastening institutional engagement with digital assets, from Europe’s Markets in Crypto-Assets (MiCA) framework to the increasing legislative momentum in the U.S. with the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act. For financial institutions, the question has shifted from whether to engage with crypto to how to do so securely.

A critical error made by many institutions is treating crypto as an extension of existing products. It is not. Cryptocurrency fundamentally alters how anti-money laundering (AML) risks must be evaluated, monitored, and controlled.

At its essence, blockchain introduces three defining features: immutability, pseudonymity, and borderless value transfer. These characteristics reshape both the risk of financial crime and the tools required for its management.

Control shifts from accounts to keys

In traditional finance, assets are safeguarded through centralized systems and reversible transactions. In crypto, control lies with private keys. When institutions provide custody, AML risk becomes intertwined with cybersecurity risk. A compromised key is not merely a breach — it represents an irreversible transfer of value, often beyond recovery. This necessitates controls such as multi-signature authorization, cold storage, strict access governance, and wallet segregation — all of which fall outside traditional AML frameworks but are essential for risk mitigation.

Non-custodial wallets mean dynamic risk assessments

Traditional AML heavily relies on customer identity and static risk profiling. In the realm of crypto, this model fails. Customers can transact using non-custodial wallets that operate outside institutional onboarding frameworks, and illicit activities often manifest in transaction patterns rather than through identity.

Consequently, risk assessment must shift from “who the customer is” to “what the wallet does.” This requires continuous monitoring of on-chain behavior, including exposure to high-risk counterparties, mixers, and decentralized protocols. Risk becomes dynamic, not periodic.

Crypto financial crime is structurally more complex

Cryptocurrency-related money laundering can involve emerging technologies, such as chain-hopping and the use of privacy-enhancing tools like mixers, which lack direct parallels in traditional finance. Transactions can traverse multiple jurisdictions in minutes, making legacy screening systems inadequate. Effective AML now relies on blockchain intelligence: the capability to trace funds, identify both direct and indirect exposure to risky entities, and interpret transaction patterns across networks.

These transformations demand a corresponding evolution in governance and risk management. Boards and risk committees must redefine their risk appetite to account for crypto-specific exposures. Institutions should establish specialized teams (e.g., digital asset approval committees and high-risk customer panels) to tackle rapidly evolving risks.

Most critically, the Enterprise-Wide Risk Assessment (EWRA) must become adaptive. Static, point-in-time assessments are insufficient in an environment where risk profiles can shift with a single transaction.

The table below illustrates how customer risk evaluation must adapt:

| Area of focus | TradFi | Crypto |

|---|---|---|