Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Cryptocurrency assets challenge conventional accounting standards, presenting significant risks for auditors and fund managers. Ganna Vitko analyzes trends in the U.S. and EU.

(Amol Tyagi/ Unsplash)

(Amol Tyagi/ Unsplash)

Key Information:

You are reading Crypto for Advisors, CoinDesk’s weekly newsletter designed to elucidate digital assets for financial advisors. Subscribe here to receive it every Thursday.

In this article

BTC$69,579.04◢1.40%

BTC$69,579.04◢1.40%

In this edition of the newsletter, Ganna Vitko, president of the Toronto Chapter of Women in Crypto, elaborates on the accounting regulations applicable to cryptocurrencies and digital assets, along with the difficulties that arise from managing these new types of assets.

Additionally, in the Ask an Expert segment, Aaron Brogan of Brogan Law addresses inquiries regarding token issuance and its tax ramifications.

– Sarah Morton

The accounting and auditing hurdles for cryptocurrency funds: an overview of the EU and U.S. markets

The cryptocurrency sector presents considerable challenges for auditors and accountants across all regions. Here are some of those challenges.

What to Know:

- As digital assets do not align seamlessly with current Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS), there is considerable ambiguity surrounding their classification, valuation, and disclosure in both the EU and the U.S.

- While the EU is gradually progressing towards better standardization through new regulations, the U.S. continues to depend on interpretive methods.

- This situation forces auditors, accountants, and fund managers to deal with increased inconsistency and risk.

The financial sector has experienced an extraordinary transformation over the last ten years. As digital assets become integral components of the financial landscape, all market participants have had to adjust to new realities.

Related Posts

No group has faced more challenges than auditors and accountants. In particular, traditional auditing and accounting methodologies—rooted in conventional financial instruments and dependable infrastructure—are inadequate for the rapidly evolving environment of digital wallets and distributed ledgers.

Below, we will examine some of the primary obstacles auditors and accountants encounter in both the U.S. and EU.

The essence of the challenges

At the core of the accounting and auditing difficulties lies a fundamental disconnect: digital assets simply do not conform to long-standing frameworks. For example, under U.S. GAAP and IFRS, assets are categorized into distinct classifications such as cash, securities, derivatives, or intangibles.

However, cryptocurrencies resist such clear categorization. Are they considered financial instruments? Intangible assets? Or should they be classified as inventory? Despite recent efforts, few jurisdictions have successfully defined them.

This ambiguity has various adverse consequences, influencing how crypto holdings are validated, when impairments are acknowledged, and how gains and losses are recorded in financial statements.

Regulatory scrutiny and enforcement patterns

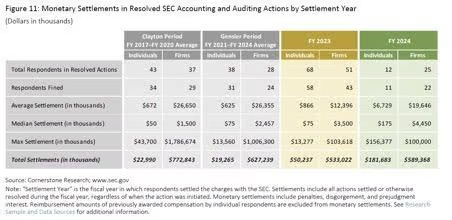

It is important to recognize that this uncertainty in accounting and custody is occurring in a context where regulatory oversight is at unprecedented levels. While not all SEC enforcement actions are directly related to cryptocurrency or audit failures, recent statistics on accounting and auditing enforcement provide valuable insight into the compliance landscape that digital asset funds currently navigate.

The figures presented in the table above indicate a significant change in enforcement trends. For instance, the number of respondents in accounting and auditing cases has decreased in fiscal year 2024. However, the average settlement amounts have risen considerably, particularly for individual respondents. This trend suggests a shift away from broad enforcement actions towards a focus on fewer cases with greater financial implications. Consequently, this increases the personal and professional risks for all parties involved.

Conversely, Europe is pursuing a notably different trajectory. As the Markets in Crypto-Assets (MiCA) framework begins phased implementation and supervisory collaboration strengthens among member states, the focus is gradually shifting towards established compliance frameworks and standardized reporting requirements.

Thus, there exists a contrast in regulatory dynamics between these regions. In the U.S., the intensity of enforcement fluctuates with changes in policy direction and case prioritization. In contrast, the EU is advancing codification through structured legislative harmonization. Both of these trends influence the governance environment in distinct but significant ways for cryptocurrency fund managers and their auditors.

Looking forward: optimal practices and innovation

- Regular third-party verification of reserves

- Independent valuation services utilizing multi-exchange pricing

- Strengthened internal controls over cryptocurrency operations

- Investment in auditing technologies that utilize blockchain analytics.

Auditors and accountants are also broadening their expertise and collaborating with specialists, which represents a significant advancement.

Conclusion

For both auditors and accountants, navigating these complexities necessitates greater technical acumen and proactive engagement with all forthcoming guidance. Ultimately, conditions will improve as more refined frameworks emerge. Such frameworks will enhance transparency, mitigate risk, and promote sustainable development within the cryptocurrency fund ecosystem.

– Ganna Vitko, president, Toronto Chapter of Women in Crypto

Ask an Expert

Q. My client is thinking about launching a meme coin. What factors should they consider?

The SEC has issued guidance indicating that it does not classify certain “meme coins” as securities. If a client intends to sell these tokens, they should understand that the tax implications of meme coin sales differ from those of exempt securities offerings. According to IRC § 1032, proceeds from stock are not subject to income tax, but this legal provision does not have a corresponding crypto equivalent. Therefore, if your client sells meme coins, they may be liable for ordinary income tax.

Q. How might this evolve in the future?

There has been an initiative among cryptocurrency legal experts, such as Miles Jennings, to bring cryptocurrency projects back to the U.S. However, many projects prefer to launch offerings offshore, partly to evade the tax consequences associated with issuing in the United States. Taxation remains a prominent policy topic among crypto advocates in Washington, D.C., and a resolution to the issuance dilemma may be addressed in forthcoming legislation.

– Aaron Brogan, managing attorney, Brogan Law

Continue Reading

- Bitcoin has surpassed the 20 million mined threshold, with 1 million units remaining to be mined by 2140.

- Stablecoins will not receive any form of deposit insurance under GENIUS regulations, as stated by the FDIC.

- Millions of Americans are beginning to receive IRS digital asset tax form 1099-DA.