Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

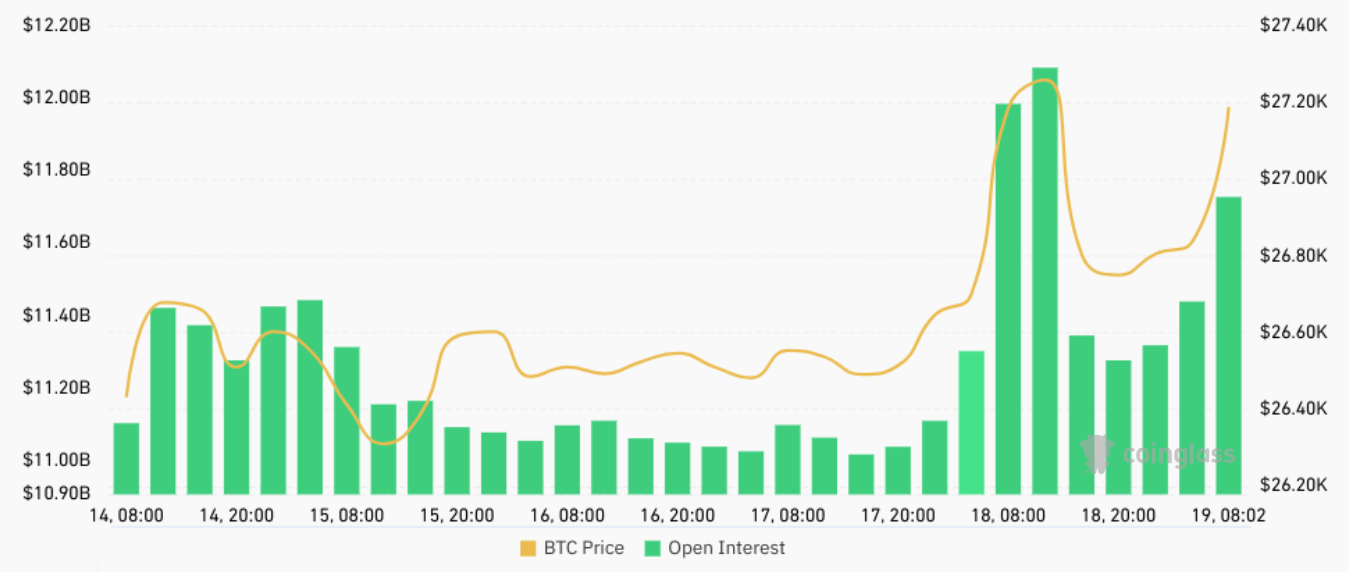

On September 18, Bitcoin’s (BTC) open interest on derivatives exchanges saw a sudden increase of $1 billion, leading investors to speculate whether large holders were accumulating in anticipation of the release of Binance’s court documents.

However, a detailed examination of derivatives metrics reveals a more complex scenario, as the funding rate did not show evident signs of heightened buying interest.

The decision to unseal these documents was authorized by the United States Securities and Exchange Commission, which had accused Binance of failing to cooperate despite previously consenting to a court order concerning unregistered securities activities and other claims.

BTC futures aggregate open interest, USD (green, left). Source: CoinGlass

BTC futures aggregate open interest, USD (green, left). Source: CoinGlass

The open interest surged to $12.1 billion, while Bitcoin’s price simultaneously rose by 3.4%, reaching its highest level in over two weeks at $27,430.

Nevertheless, investors soon recognized that, apart from a statement from the Binance.US auditor regarding the difficulties in ensuring complete collateralization, there was minimal substantial information disclosed in the unsealed documents.

Later that day, Federal Judge Zia Faruqui denied the SEC’s request to examine Binance.US’ technical infrastructure and provide additional information. However, the judge mandated that Binance.US must supply further details about its custody solution, raising questions about whether Binance International ultimately oversees these assets.

By the conclusion of September 18, Bitcoin’s open interest had decreased to $11.3 billion as its price fell by 2.4% to $26,770. This drop indicated that the entities responsible for the open interest increase were no longer willing to maintain their positions.

These large holders may have been dissatisfied with the court’s outcomes, or the price movements may not have occurred as anticipated. In any event, 80% of the open interest increase vanished in under 24 hours.

Futures’ buyers and sellers are matched at all times

Related Posts

It can be inferred that the majority of the demand for leverage was fueled by optimistic sentiment, as Bitcoin’s price rose alongside the open interest increase and subsequently fell as 80% of the contracts were liquidated. However, linking cause and effect solely to Binance’s court decisions appears unwarranted for several reasons.

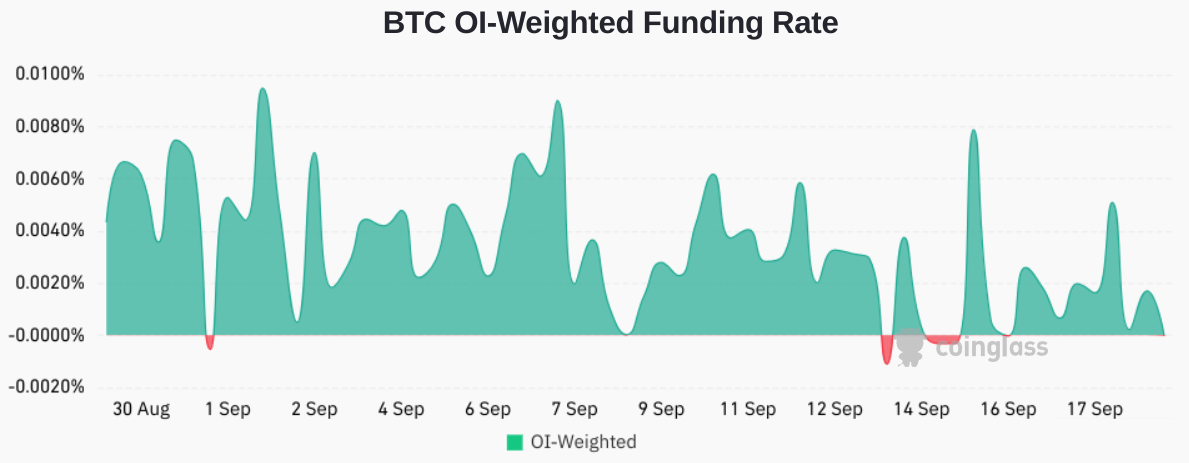

Firstly, it was not expected that the unsealed documents would be favorable to Binance or its CEO, Changpeng “CZ” Zhao, considering it was the SEC that initially requested their release. Furthermore, the Bitcoin futures contract funding rate, which measures imbalances between long and short positions, remained relatively stable during this timeframe.

BTC futures average 8-hour funding rate. Source: CoinGlass

BTC futures average 8-hour funding rate. Source: CoinGlass

If there had indeed been an unexpected demand surge of $1 billion in open interest, primarily driven by eager buyers, it would be reasonable to expect that the funding rate would have surged above 0.01%. However, the opposite occurred on September 19, as Bitcoin’s open interest grew to $11.7 billion, while the funding rate dropped to zero.

With Bitcoin’s price climbing above $27,200 during this subsequent phase of open interest growth, it becomes increasingly clear that, regardless of the underlying motivations, the price pressure tends to be upward. While the precise reasoning may remain unclear, certain trading patterns could provide insight into this movement.

Market makers’ hedge could explain OI spike

One plausible explanation could involve market makers executing buy orders on behalf of significant clients. This would account for the initial excitement in both the spot market and BTC futures, driving the price higher. Following the initial increase, the market maker becomes fully hedged, negating the need for further buying and resulting in a price correction.

During the second phase of the trade, there is no effect on Bitcoin’s price, as the market maker must liquidate the BTC futures contracts and acquire spot Bitcoin. This leads to a decrease in open interest and may disappoint some participants who were expecting further buying enthusiasm.

Rather than hastily categorizing every “Bart” formation as manipulation, it is prudent to investigate the operations of arbitrage desks and thoroughly analyze the BTC futures funding rate before reaching conclusions. Thus, when there is no excessive demand for leveraged long positions, an increase in open interest does not necessarily indicate a buying frenzy, as was observed on September 18.

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

This article is for general informational purposes and is not intended to be and should not be construed as legal or investment advice. The views, thoughts, and opinions expressed here are solely those of the author and do not necessarily reflect or represent the views and opinions of Cointelegraph.