Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

$61 million bitcoin investor liquidated on HTX as market sentiment returns to ‘extreme fear’

The liquidation marked the largest single forced closure within a 24-hour period as bitcoin lost its weekend gains and the fear index dropped to historic lows.

Key points:

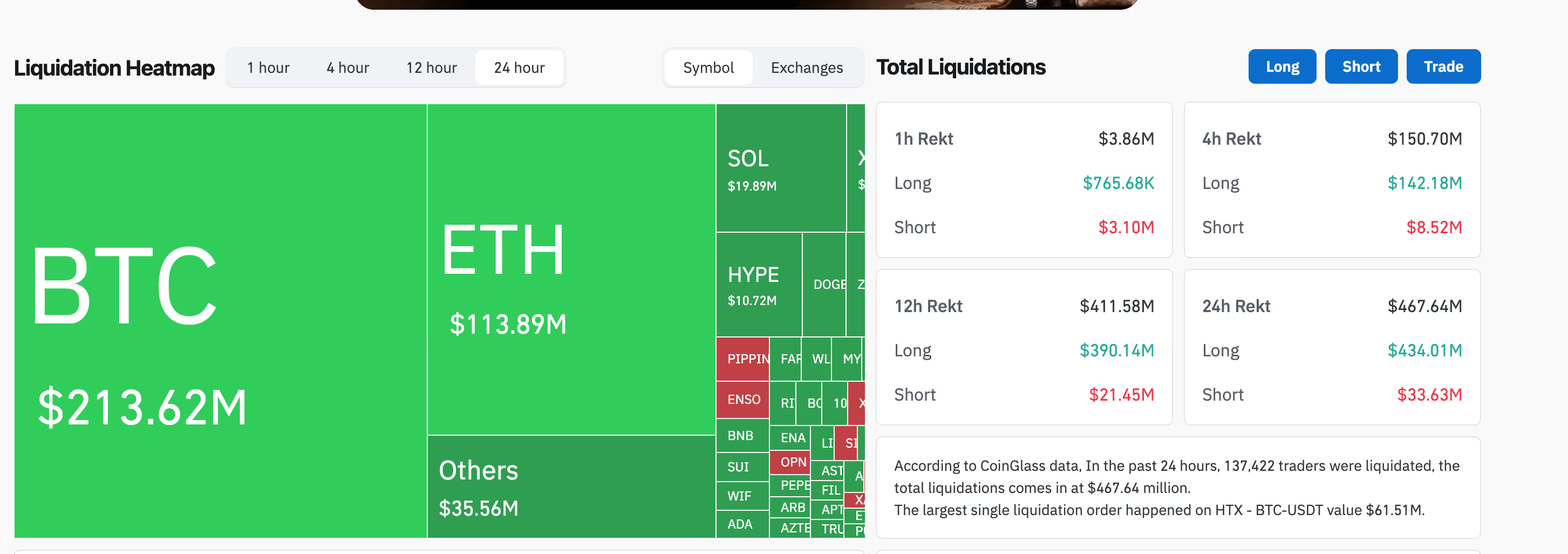

- Bitcoin fell from approximately $68,600 on Saturday to $64,300 on Monday, negating its weekend gains and causing about $468 million in crypto futures liquidations, primarily from long positions.

- A notable liquidation of $61.5 million in BTC–USDT on HTX and a decline in the Crypto Fear and Greed Index to an “extreme fear” score of 5 underscore the increasing anxiety and capitulation among short-term bitcoin investors.

- With bitcoin currently around 48% below its record high from October and traders persistently re-entering leveraged long positions during brief rallies, analysts caution that the cycle of sudden price increases, liquidations, and resets is likely to continue.

Bitcoin’s price declines on Monday eliminated a significant leveraged bullish position.

The $61.5 million trade was forcibly closed by cryptocurrency exchange HTX, which represents the largest single liquidation in the last 24 hours, according to data from Coinglass.

STORY CONTINUES BELOWStay updated on the latest developments.Subscribe to the Crypto Daybook Americas Newsletter today. See all newslettersSign me up

The liquidation occurred as bitcoin dropped from Saturday’s peak of $68,600 back to $64,400, erasing the gains made over the weekend in a short span of time. CoinDesk contacted HTX for a statement.

Related Posts

The significant impact—large enough to indicate a concentrated position from a whale or fund rather than a retail margin call—occurred amid a wider market downturn that saw $467.64 million in total liquidations across 137,422 traders, as per CoinGlass. Long positions represented $434 million of this, approximately 93% of the overall total, indicating a market still oriented towards upside before the week began and faced a flush when bids vanished.

Bitcoin futures alone accounted for $213.62 million in forced closures, followed by ether (ETH) at $113.89 million and solana (SOL) at $19.89 million. Hyperliquid’s HYPE token contributed an additional $10.72 million, a notable amount for an asset outside the typical top-five liquidation rankings.

Fear prevails

The selloff pushed Alternative.me’s Crypto Fear and Greed Index down to 5 out of 100, a score classified as “extreme fear,” which has only been reached three times since the index’s inception in 2018: August 2019, June 2022, and earlier this month during bitcoin’s drop to $60,000.

Glassnode’s data further corroborates the pressure. The firm reported on Monday that the seven-day moving average for net realized losses among recent bitcoin purchasers remained near $500 million daily, indicating that short-term holders continue to capitulate even following the initial flush in February.

“While the intensity has diminished, the overall situation still indicates a market under strain,” Glassnode observed, “with participants in the base formation phase continuing to capitulate.”

Bitcoin is now approximately 48% below its all-time high of $126,000 from October and 5.5% beneath its 2021 bull-market peak of $69,000—a level that once appeared to be a ceiling and now resembles a floor subject to repeated testing. The damage from Monday eliminated leverage, but the pattern persists: traders continue to reload long positions after each bounce, and the market consistently punishes them for it.