Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

US employment surpasses expectations, but underlying labor challenges may maintain pressure on Bitcoin.

The US economy saw an increase of 178,000 jobs in March, significantly surpassing the consensus estimate of 60,000, while the unemployment rate fell to 4.3%. This type of report can shift macroeconomic narratives and impact risk assets before traders complete their initial assessments.

Bitcoin was trading around $67,000, remaining unaffected by the data. The yield on the 10-year Treasury rose by four basis points to 4.35%, and the dollar index increased to 100.08.

The market’s immediate interpretation was clear: a robust labor market provides the Federal Reserve with less incentive to lower rates, which in turn leads to tighter financial conditions that could negatively affect macro-sensitive assets like Bitcoin.

Why this matters: Bitcoin’s response was influenced by more than just a jobs report exceeding expectations. The indication of a stronger labor market diminishes the Fed’s urgency to reduce rates. If this perspective persists, yields and the dollar may remain stable, exerting pressure on liquidity-sensitive assets such as BTC.

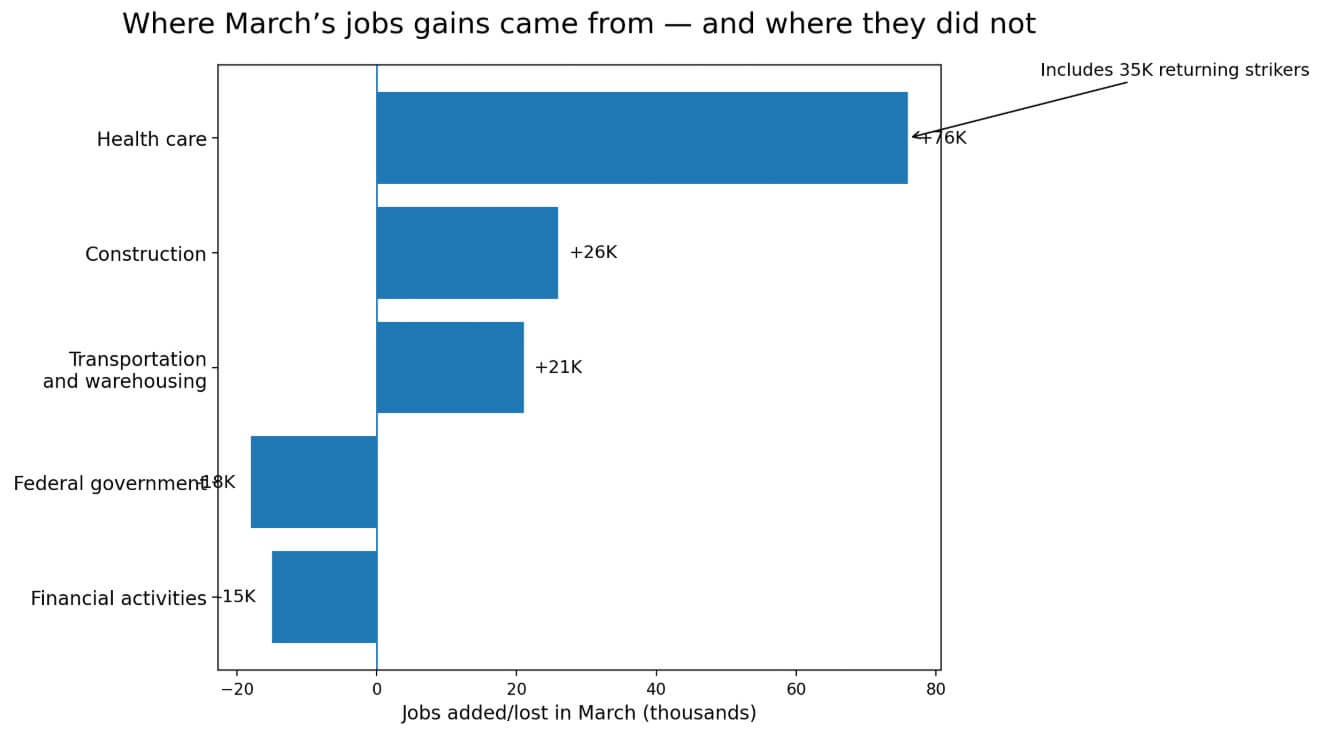

Examining the sources of the 178,000 jobs reveals a more complex picture. The health care sector alone contributed 76,000 positions, with 35,000 of those being workers returning from a strike in physicians’ offices. These figures reflect a recovery in hiring.

Construction added 26,000 jobs, aided in part by favorable weather, while transportation and warehousing accounted for another 21,000. Conversely, federal government employment decreased by 18,000, and financial activities lost 15,000 jobs.

Related Reading

Related Reading

161,000 US jobs just disappeared after a revision as Bitcoin navigates increasingly messy macro data

Nearly 1 million US jobs were found to be nonexistent, according to a significant government revision.

Mar 8, 2026 · Andjela Radmilac

The BLS indicated that total payroll employment had changed little overall over the past 12 months.

This context makes the March report appear as a rebound from a turbulent February, with sector-specific recovery contributing significantly to the overall increase.

A bar chart illustrates health care leading March job gains at 76,000, including 35,000 returning strikers, while federal government and financial activities experienced job losses.

A bar chart illustrates health care leading March job gains at 76,000, including 35,000 returning strikers, while federal government and financial activities experienced job losses.

The household survey runs the other way

The household survey, which monitors employed and unemployed individuals across the population, showed a contrasting trend compared to the payroll figures.

The civilian labor force decreased by 396,000 in March, with participation dropping to 61.9%. Household employment fell by 64,000, and the number of individuals not in the labor force increased by 488,000.

Marginally attached workers rose by 325,000 to 1.9 million, and discouraged workers increased by 144,000 to 510,000. The average workweek was shortened to 34.2 hours.

Average hourly earnings increased by only 0.2% month over month and 3.5% year over year, with no wage acceleration to support the payroll increase.

| Indicator | March reading | Why it matters |

|---|---|---|

| Nonfarm payrolls | +178K | Strong headline beat versus expectations |

| Unemployment rate | 4.3% | Makes the labor market look firm at first glance |

| Civilian labor force | -396K | Suggests weaker labor-market participation beneath the headline |

| Labor-force participation rate | 61.9% | Fewer people working or looking for work |

| Household employment | -64K | The people-based survey moved opposite the payroll survey |

| Not in labor force | +488K | Reinforces the softer under-the-hood read |

| Marginally attached workers | +325K to 1.9M | Shows weaker labor attachment at the margin |

| Discouraged workers | +144K to 510K | Signals more workers are giving up on job searches |

| Average workweek | 34.2 hours | A shorter workweek can point to softer labor demand |

| Average hourly earnings | +0.2% m/m, +3.5% y/y | No wage reacceleration to confirm the payroll beat |

The revision for February adds another layer of complexity. The BLS adjusted February’s figures down to -133,000 from -92,000 and revised January’s figures up to 160,000 from 126,000. The net two-month revision was only -7,000, resulting in a pattern that is noisy and lacks a consistent directional trend.

Payroll growth in the first quarter averaged approximately 68,000 per month, a modest pace by any expansion standard.

The BLS revises monthly estimates twice as additional employer reports are received and seasonal factors are recalibrated.

Since 2003, the average absolute revision from the first to the third estimate has been 51,000 jobs. A revision of that magnitude would adjust March’s figure from 178,000 to around 127,000, which is considerably less striking.

Related Posts

To negate the entire increase, March would require a job-creation figure exceeding 118,000, roughly 2.3 times the historical average, and typical revision fluctuations do not reach that level.

The BLS’s annual benchmark revision removed 898,000 jobs from the March 2025 payroll level, four times the average absolute benchmark revision of the previous decade.

This revision indicated that initial payroll figures have recently exhibited more uncertainty than markets generally account for during the first trading hour following a strong report.

The rates channel behind Bitcoin's drop

The Federal Reserve maintained its target range at 3.50% to 3.75% in March.

The median participant’s forecast placed 2026 unemployment at 4.4%, PCE inflation at 2.7%, and the year-end fed funds rate at 3.4%. With March unemployment at 4.3% and a payroll figure of 178,000, policymakers felt no urgency to act.

Research from NYDIG frames the Bitcoin-to-macro connection similarly: BTC trades in accordance with real rates, liquidity, and risk appetite. A Fed that maintains its stance in a strong labor market removes the near-term catalyst that Bitcoin requires.

The February JOLTS report supports this without raising alarms. Job openings remained near 6.9 million, but hires decreased to 4.8 million, and the hiring rate fell to 3.1%, the lowest level since April 2020.

Initial jobless claims for the week ending March 28 were reported at 202,000, close to cycle lows.

Collectively, these data points depict a labor market in a state of equilibrium, with layoffs contained, new hiring sluggish, and companies maintaining their workforce levels.

This environment does not prompt a Fed pivot, and a Fed that does not pivot keeps financial conditions tighter for an extended period.

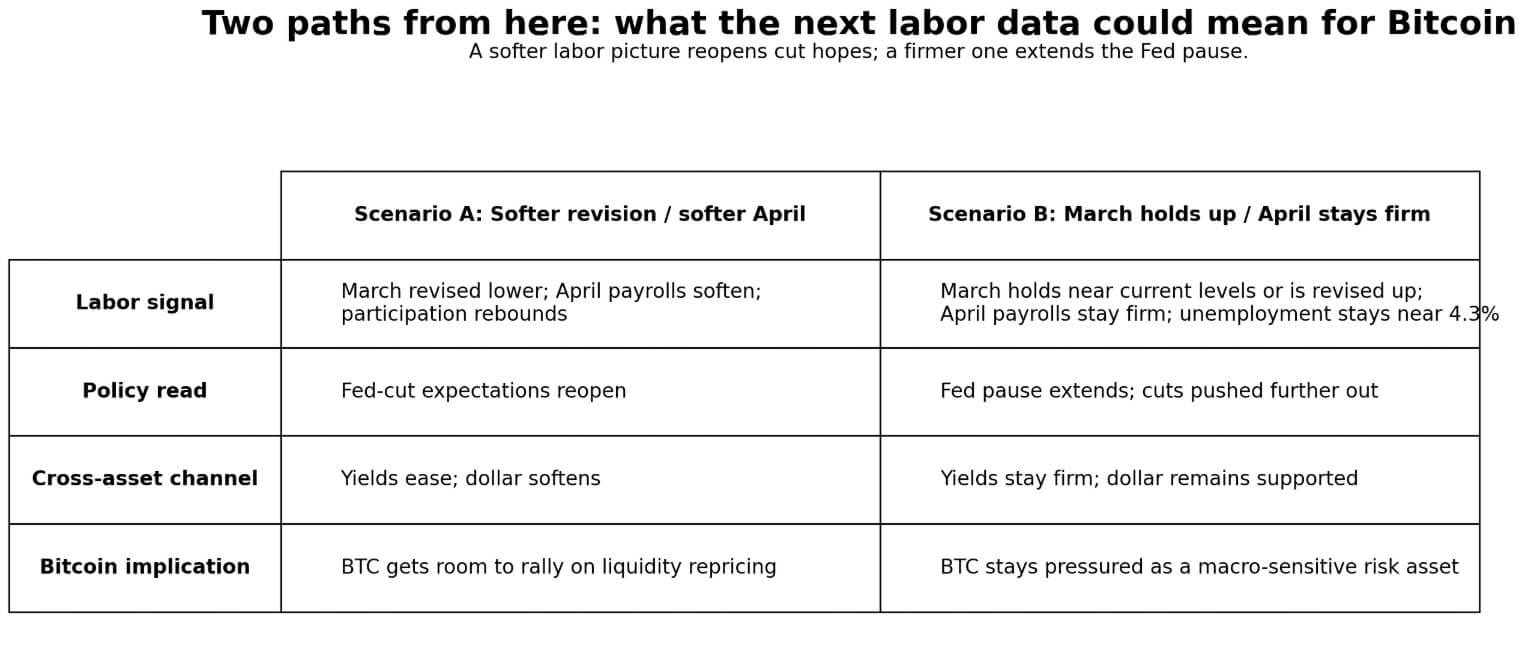

Potential outcomes for Bitcoin

Bitcoin’s price movements on April 3 were influenced by the rates channel. Labor strength diminished expectations for rate cuts, firmer yields, and a stronger dollar tightened conditions for liquidity-sensitive assets. This channel has the potential to reverse.

If the BLS revises March payrolls significantly lower toward sub-100,000, and April payrolls also come in weak while participation rebounds, the “headline-only strength” narrative could gain traction.

Expectations for cuts would reopen, yields would decrease, and Bitcoin would have the opportunity to rise on liquidity repricing. The weakness in the household survey, the distortion from returning strikers in health care, and the low-hiring backdrop from JOLTS each make this scenario plausible, but April data on May 8 would need to validate it.

If March remains close to current levels or the BLS revises it upward, and April payrolls exceed approximately 125,000 while unemployment stays around 4.3% or lower, February will be seen as the clear outlier.

The Fed would extend its pause with greater confidence, rate cuts would be pushed further out, and Bitcoin would continue to trade as a macro risk asset without a near-term liquidity catalyst.

The cross-asset movement on April 3, with rising yields, a stronger dollar, and a declining BTC, indicated that the market had already begun to price in that trajectory.

A two-scenario table illustrates how softer or firmer April labor data would influence Fed policy, yields, and the dollar in relation to Bitcoin’s price.

A two-scenario table illustrates how softer or firmer April labor data would influence Fed policy, yields, and the dollar in relation to Bitcoin’s price.

The next Employment Situation report is set for May 8 at 8:30 a.m. ET, which will include both April payrolls and the first revision to March.

This makes it a crucial checkpoint for every argument based on the April 3 report. March CPI is scheduled for release on April 10, and the next FOMC meeting will take place on April 28-29, two data points the Fed will consider before making its next policy decision.

CPI, in particular, will assess whether labor market strength aligns with persistent inflation or with the wage deceleration suggested by the March report.

The post US jobs crush forecasts, yet hidden labor weakness could keep Bitcoin under pressure appeared first on CryptoSlate.