Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

The upcoming Bitcoin downturn may signal a loss of confidence on Wall Street, leading to increased selling activity.

This weekend, Bitcoin’s price fell below $67,000, following a significant decline that left it over 40% lower than its peak in October 2025. In February, BTC had decreased by approximately 47% from its high near $126,000.

In previous market conditions, such a drop would have triggered various negative reactions that would extend well beyond the spot market. Panic would spread rapidly, long-term holders would sell off, and the selling pressure would exacerbate itself.

However, this time, very little of that occurred.

Related Reading

Related Reading

Bitcoin price has never ended a year higher after a start this bad — is $88k the 2026 ceiling now?

Historically, Bitcoin’s worst opening periods set a ceiling of $88k for this year, with no historical precedent for a recovery into a full-year gain.

Mar 27, 2026 · Liam 'Akiba' Wright

The most notable aspect of this pullback was not the price movement itself, but the surrounding behavior.

Even during a downturn of this magnitude, the US spot bitcoin ETF sector performed significantly better than anticipated. Eric Balchunas, the chief ETF analyst at Bloomberg, noted in February that only about 6% of ETF assets had exited during the decline.

The introduction of spot bitcoin ETFs was always viewed as a pivotal moment for crypto, but the more significant shift may be occurring now, as the market faces considerable pressure. Bitcoin has attracted a new class of holders, who seem less inclined to sell at the first sign of difficulty.

The SEC approved spot bitcoin exchange-traded products in January 2024, with trading commencing the following day. This led to one of the largest product launches in ETF history.

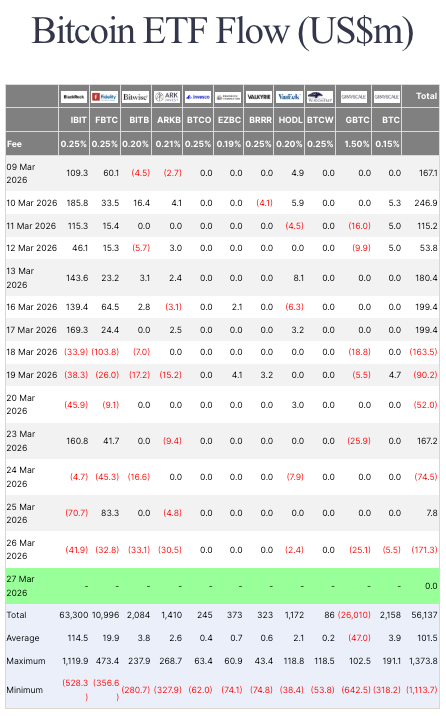

As of March 27, Farside’s data indicated approximately $56.1 billion in cumulative net inflows across US spot Bitcoin ETFs since their launch. BlackRock’s IBIT alone accounted for about $63.3 billion, while Fidelity’s FBTC attracted around $11.0 billion. In contrast, Grayscale’s GBTC experienced a loss of approximately $26.0 billion.

There has been genuine selling within this category, with some instances being quite substantial. Nevertheless, overall, ETFs continued to draw in capital.

Thus, when Bitcoin experienced its drop, it did not drag ETFs down with it.

The daily flow dynamics remain volatile, but they align with general expectations. Farside data shows net inflows of $167.2 million on March 23, followed by a net outflow of $171.3 million on March 26. A perfect calm is unlikely in the near future, particularly given the ongoing geopolitical unrest, but there is relative resilience. A significant downturn occurred, yet the mass exodus many anticipated did not materialize.

Table showing spot Bitcoin ETF flows from March 9 to March 27, 2026 (Source: Farside)

Table showing spot Bitcoin ETF flows from March 9 to March 27, 2026 (Source: Farside)

The new Bitcoin holder

The ETF structure transformed who could own Bitcoin and the manner in which they could possess it. Rather than being held on exchanges and in wallets, BTC transitioned into institutional products that exist within a familiar investment framework.

Related Posts

Related Reading

Related Reading

Bitcoin price is heading for weekend collapse to $61k – will a social media post from Trump save it?

Bitcoin could test $61,700 this weekend unless Trump issues another market-stabilizing message.

Mar 27, 2026 · Liam 'Akiba' Wright

ETFs introduced Bitcoin to institutional investors, but this adoption was reciprocal: it also brought institutional trading to Bitcoin. Some of the initial participants in Bitcoin ETFs may have been significant Bitcoin holders seeking regulated exposure, but the market soon became filled with those aiming to capitalize on its liquidity and volatility.

CF Benchmarks, analyzing 13F filings, revealed that much of the hedge fund exposure to Bitcoin ETFs was linked to basis-style trades rather than long-term conviction. SEC regulations also indicate that 13F filings are submitted with a delay, providing snapshots of past behavior rather than real-time actions. Nonetheless, they illustrate how diverse the investor base has become.

This distinction is crucial. When we state that Wall Street barely reacted, it does not imply that no one sold as BTC lost half its value. It signifies that the ETF sector endured a severe drop without the mass exit that once seemed unavoidable.

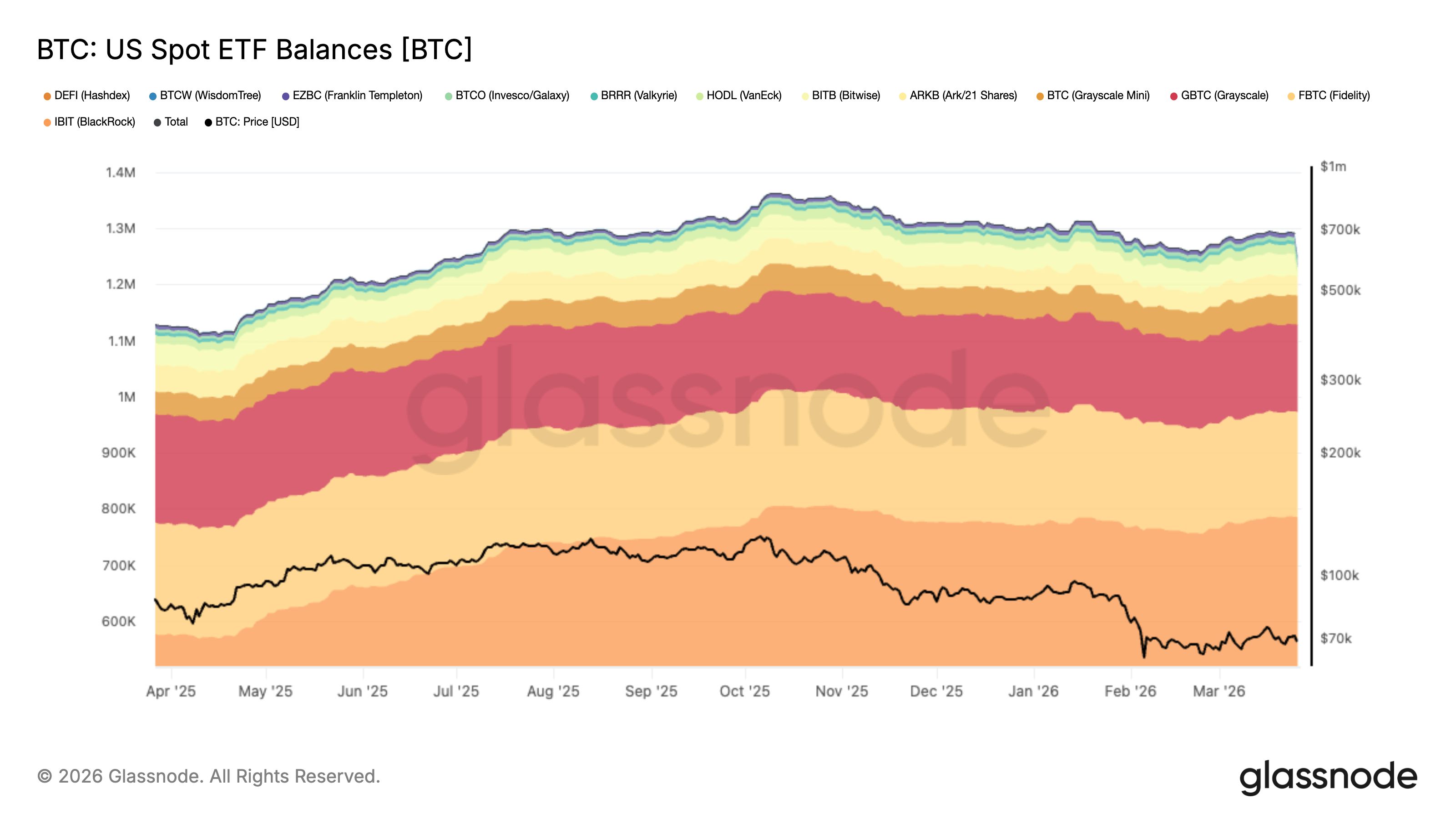

Examining the individual funds clarifies this further. IBIT remains the standout leader in the category, while FBTC has also established a substantial base, and GBTC continues to experience asset outflows. We have observed strong inflows into the leading funds, consistent support for several others, and ongoing withdrawals from the older incumbent.

Graph showing spot Bitcoin ETF balances from March 27, 2025, to March 26, 2026 (Source: Glassnode)

Graph showing spot Bitcoin ETF balances from March 27, 2025, to March 26, 2026 (Source: Glassnode)

A crash with a different rhythm

The most fitting comparison to the impact Bitcoin’s price had on ETFs may be gold.

In 2013, a sharp decline in gold prices prompted a significant outflow from gold-backed ETFs. The World Gold Council reported that 350 tonnes exited by the end of April that year, marking a 12.9% reduction in holdings.

However, Bitcoin’s ETF base appears to be different. The price decline has been considerably more severe than what gold experienced, yet the anticipated mass exit of large holders did not occur.

Nonetheless, Bitcoin is far from stable at this moment. March 26 alone saw a net outflow of $171.3 million from ETFs, and the price continues to fluctuate significantly in response to news regarding developments in Iran.

Yet, the response from holders is evolving, and this may represent the most significant change brought about by the ETF era.

There are two interpretations of this situation. One is that ETFs attracted stronger hands, investors who are more inclined to view Bitcoin as part of a broader investment portfolio. The other is that selling has merely slowed, and a larger macroeconomic shock could still test that patience later. Both scenarios are plausible, as the data has not yet resolved the debate.

Regardless of the future outcome, this shift in ETF behavior has unveiled something new about Bitcoin’s response under pressure. A 40% crash used to signify a full-blown bear market panic, but in this ETF-dominated environment, it has become a standard stress test. The price dropped sharply after a year of continuous gains, and ETF holders, at least collectively, managed to withstand the downturn much better than anticipated.

This may be the clearest indication yet that Wall Street has done more than simply invest in Bitcoin: it has altered the manner in which it sells off.

The post The next Bitcoin shock could be where Wall Street finally loses faith and starts selling appeared first on CryptoSlate.