Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

The current bond turmoil in Britain is highlighting the relevance of Bitcoin that many individuals appear to have overlooked.

The bond turmoil in Britain is reigniting a discussion that Bitcoin was designed to address—instances when confidence in sovereign debt and monetary policy begins to falter.

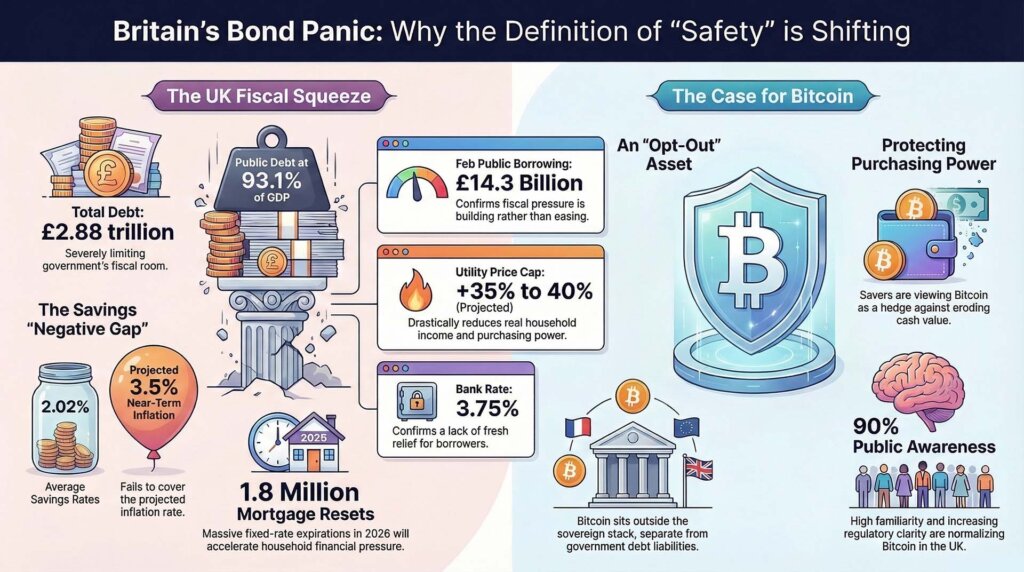

The fiscal tightening in Britain intensified following the release of official borrowing statistics, which revealed that public sector net borrowing for February reached £14.3 billion, an increase of £2.2 billion compared to the previous year and the second-highest February figure since records commenced in 1993.

Public sector net debt was recorded at £2.88 trillion, equating to 93.1% of GDP. On the same day, the Bank of England maintained the Bank Rate at 3.75% and cautioned that the recent energy crisis would elevate inflation over the next few quarters, while also increasing household fuel and utility expenses.

The immediate market reaction is evident in gilts, interest rate expectations, and mortgages. The slower adjustment is reflected in savings habits. There is no necessity for a rush into Bitcoin for the asset to be re-evaluated in a new context. A renewed wave of skepticism regarding cash, government bonds, and postponed rate reductions is sufficient to alter how savers perceive risk.

This transition begins with calculations rather than ideology. The Bank of England indicated in its latest minutes that preliminary staff projections now estimate CPI inflation to be between 3% and 3.5% over the next few quarters. It also noted that rising household fuel and utility costs would put pressure on real incomes. By January, the central bank’s data indicated that the average rate on household instant-access deposits was 2.02%.

Consequently, easy-access cash is yielding less than the inflation range the Bank itself currently anticipates. The disparity is evident, approximately 0.98 to 1.48 percentage points below the near-term CPI trajectory. For savers, this marks the beginning of a shift in the definition of safety. Cash still preserves nominal value but does less to safeguard purchasing power.

The household sector in Britain is also evolving rapidly. The latest projections from UK Finance suggest that around 1.8 million fixed-rate mortgages will mature in 2026. The Office for National Statistics has already indicated in its household-costs index that inflation was at 3.6% for all households and 3.7% for mortgagors in the fourth quarter of 2025. This occurred prior to the Bank’s latest warning that energy prices would further increase costs.

The sequence in the UK involves government borrowing, gilt repricing, and household finances. Gilts appear less stable. Easy-access cash yields below the near-term inflation trajectory. Mortgage challenges are poised to impact more households as fixed agreements expire.

In this context, Bitcoin becomes increasingly relevant as savers contemplate whether a small asset outside the sovereign framework should be part of their portfolio.

Infographic comparing Britain’s bond market stress, rising public debt, and inflation pressures with Bitcoin as a potential hedge and store of value.

Infographic comparing Britain’s bond market stress, rising public debt, and inflation pressures with Bitcoin as a potential hedge and store of value.

| Indicator | Latest figure | How it changes saver behavior |

|---|---|---|

| February public borrowing | £14.3 billion | Indicates that fiscal pressure is continuing to build rather than diminish |

| Public debt | 93.1% of GDP | Restricts the potential for a straightforward fiscal reset |

| Bank Rate | 3.75% | Confirms that the Bank did not provide new relief |

| BoE near-term CPI view | 3% to 3.5% | Indicates renewed pressure on real incomes |

| Instant-access deposit rate | 2.02% | Leaves easy cash below the Bank’s inflation expectations |

| Mortgages resetting in 2026 | 1.8 million | Accelerates the household impact of rising rates |

The squeeze begins with cash flow, then extends to portfolio decisions

The Bank of England’s latest account of the situation provides the cross-market context. In its March statement, the Bank noted that approximately one-fifth of global oil and LNG supply typically transits through the Strait of Hormuz, Brent crude and Dutch TTF gas prices were around 60% higher than pre-shock levels, and UK gas futures suggested that the next Ofgem cap could increase by 35% to 40%.

Related Reading

Related Reading

While the world watches oil prices, one critical Fed cash backstop is almost empty

Bitcoin may currently be more vulnerable as a concealed Fed liquidity buffer that previously alleviated stress is nearly depleted.

Mar 20, 2026 · Liam 'Akiba' Wright

This serves as the link between macroeconomic data and the retail saver. A government can maintain a significant deficit for years without altering how households perceive money. However, a spike in utility bills occurs monthly. A mortgage reset arrives with a letter and a direct debit. These are the moments when a saver begins to evaluate trade-offs concerning purchasing power, liquidity, volatility, and trust in the issuer.

This distinction is important as Bitcoin experienced a decline of approximately 50% from October 2025 to February 2026, while options volatility surged to its highest level since 2022. During a period of active tightening, investors tend to sell volatile assets and increase cash holdings. Bitcoin remains susceptible to liquidity pressures during such times.

This trend also reinforces the longer-term case for Bitcoin in the context of this UK situation. Gilts are volatile, anticipated rate cuts have been postponed, and easy-access cash yields less than the inflation the central bank now predicts. Under these circumstances, Bitcoin begins to appear less as mere speculation and more as an alternative to sovereign monetary commitments. It carries its own volatility and presents a different risk profile compared to the challenges currently facing cash and government debt holders.

The regulatory environment in the UK facilitates this discussion more than it did in previous years. The Financial Conduct Authority’s recent consumer research indicated that crypto awareness exceeds 90%, and 25% of crypto users expressed a greater likelihood of investing if the market were more regulated.

This finding underscores familiarity with the asset class and sensitivity to regulatory clarity. It leaves the magnitude and timing of any new demand uncertain.

Britain warrants attention beyond its borders because the household dynamics are particularly transparent. The US continues to dominate crypto transactions, ETF headlines, and dollar liquidity. However, Britain reveals the pressure points more swiftly.

When debt levels are high, borrowing exceeds expectations, utility bills rise, and a significant portion of mortgages approaches reset, the implications reach households more rapidly. The crypto implication is a broader readiness to view sovereign debt and bank deposits as inadequate responses to the term “safe.”

Related Posts

The official projections align with this perspective. In its March forecast, the OBR anticipated 10-year gilt yields at 4.5% and 30-year yields at 5.3% prior to this latest shock, while also predicting public sector net debt to increase from 94.5% of GDP in 2025-26 to 96.5% in 2028-29.

It expects the tax burden to rise toward 38% of GDP by 2030-31. These figures indicate ongoing fiscal pressure and leave little room for a reassuring version of the traditional approach where rate cuts, stable bonds, and patient savers collectively resolve the issue.

Related Reading

Related Reading

Bitcoin price faces a crucial weekend test as US growth collapses to 0.7% while inflation stays stubborn

The data appeared unstable even before the oil crisis, and Powell now faces the challenge of explaining what will break first.

Mar 14, 2026 · Gino Matos

What the next 12 months could entail

The plausible scenarios for the upcoming year each have distinct impacts on savings behavior.

The shock diminishes but does not reverse

The Bank’s inflation range of 3% to 3.5% proves to be approximately accurate for the next few quarters, utility bills increase, and households rebuild precautionary cash despite soft real returns.

In this scenario, Bitcoin may not attract significant inflows, although it gains narrative traction. The rationale is straightforward: if cash is liquid but losing purchasing power, and bonds are no longer stable, a non-sovereign asset appears easier to justify as part of a diversified savings strategy.

The energy shock continues

The National Institute of Economic and Social Research modeled a scenario of persistent shock in which UK inflation runs 0.7 percentage points higher in 2026, GDP is projected to be 0.2% lower in 2026 and 0.3% lower in 2027, and the Bank Rate is expected to be about 0.8 percentage points above baseline.

Prior to the latest developments, NIESR’s winter forecast had the Bank Rate at 3.25% by the end of 2026. Collectively, these ranges maintain a trajectory above 4% if the shock persists.

This scenario is most likely to strengthen the case for Bitcoin. High debt constrains fiscal flexibility. Persistent inflation erodes cash value. Prolonged high rates impact mortgages. This combination heightens interest in assets that lie outside the state’s liabilities, even as Bitcoin itself remains volatile and sensitive to broader market pressures.

Market-functioning stress

The third scenario would negatively impact Bitcoin in the short term while enhancing its appeal over a longer duration. NIESR’s separate bond-market note cautions that a sovereign duration shock can transition from repricing into a financial-stability crisis, where central banks may require market-functioning support even while inflation remains problematic.

This represents the institutional contradiction that Bitcoin was designed to address. It is also the type of market phase that can initially pressure Bitcoin if investors seek liquidity.

This tension clarifies why Britain’s recent bond movement is noteworthy. The trade is complex. The mechanism is evident. When a state borrows extensively, energy costs rise, inflation solidifies again, and households confront mortgage resets, the societal interpretation of safety begins to evolve. The discussion shifts from macroeconomic theory to monthly cash flows and maintained purchasing power.

Britain’s recent bond movement could catalyze a Bitcoin development before many Americans recognize it as such.

The UK data already reveals the components: £14.3 billion in February borrowing, debt at 93.1% of GDP, a policy rate maintained at 3.75%, near-term inflation returning to 3% to 3.5%, easy-access cash at 2.02%, and 1.8 million mortgages set to reset in 2026.

None of these figures indicate an immediate advantage for Bitcoin. Collectively, they illustrate increasing pressure on the traditional definition of safety.

If energy prices remain high, if the next utility cap rises as futures suggest, and if mortgage resets continue to occur during a period of elevated gilt yields and postponed rate relief, more savers may conclude that cash and government securities no longer provide a comprehensive solution to their concerns.

The post Britain’s bond panic is currently making the case for Bitcoin many people seem to have forgotten appeared first on CryptoSlate.