Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Recent data indicates that retail Bitcoin wallets are no longer able to influence short-term fluctuations in BTC prices.

Bitcoin’s Price Is Being Set Further Away From Bitcoin Holders

Bitcoin concluded March within a range that appeared tranquil on the surface but was notably congested beneath.

By Monday, Bitcoin’s price hovered around $67,000 following a week that had already witnessed one of the year’s most significant derivatives events and another series of institutional withdrawals from spot exchange-traded funds.

This combination warrants more scrutiny than it has garnered. Traditional analysis would categorize the movement into distinct segments: options expiry in one category, ETF flows in another, and price in a third.

Nonetheless, the reality indicates that Bitcoin’s short-term price dynamics are increasingly diverging from those who hold Bitcoin for its inherent value and are instead aligning with those who possess Bitcoin exposure for purposes such as hedging, rolling, allocating, or mitigating risk within a framework.

This transition alters the interpretation of market movements. It also redefines what a Bitcoin price shift truly signifies.

Related Reading

Related Reading

As Bitcoin weakens even ‘safe’ investments like the 2-year Treasury are starting to crack

The most secure segment of the bond market is beginning to show signs of instability as geopolitical tensions elevate oil prices, inflation concerns resurface, and lenders seek higher returns for lending to the U.S. for just two years.

Mar 29, 2026 · Andjela Radmilac

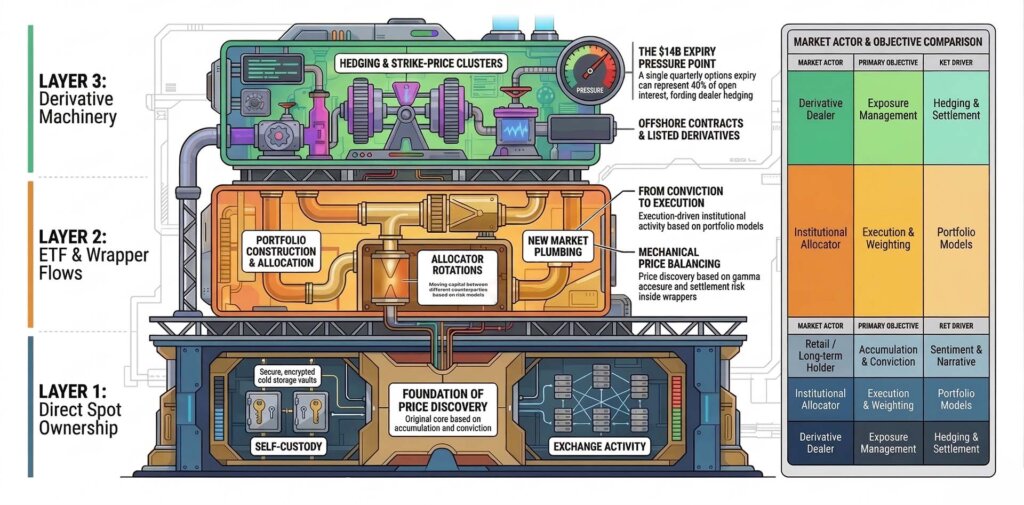

Price discovery has moved into the wrappers around Bitcoin

The initial pressure point originated from derivatives. Prior to Friday’s expiry, CryptoSlate noted that approximately $14 billion in Bitcoin options were set to expire on Deribit, representing nearly 40% of the exchange’s open interest.

This event marked a convergence of the year’s largest quarterly expiry and a market already under geopolitical strain. However, the more significant insight lies one layer deeper.

When an expiry is substantial relative to open interest, the price can begin to reflect the requirements of dealers and other intermediaries managing exposure into settlement. Price transforms into a balancing act.

This distinction may seem technical until it influences how individuals interpret every movement on the chart. Retail investors typically analyze Bitcoin through a lens of conviction. They presume that a price increase indicates greater buyer interest, a decline suggests waning conviction, and a stable range implies the market is awaiting news.

In a market influenced by large listed products, options, and institutional balance-sheet strategies, such interpretations become less dependable. A quiet trading session may involve significant mechanical activity. A sudden price shift can indicate a hedge adjustment before it reflects a directional stance on Bitcoin itself.

This is why the $14 billion expiry merits more than just a note on volatility. The expiry concluded at 08:00 UTC on March 27, eliminating around 40% of open positions on Deribit.

Related Reading

Related Reading

Bitcoin price just collapsed because the macro selloff collided with a $14 billion options expiry this morning

Approximately $14.1B in Bitcoin options and $2.2B in Ethereum options expired on Friday, Mar. 27. Historical trends indicate increased volatility surrounding expiry.

Mar 27, 2026 · Gino Matos

This scale prompts a straightforward question for spot holders. If a significant portion of short-term pricing is being swayed by the hedging and settlement activities surrounding listed contracts, how much of what is perceived as Bitcoin demand is actually derivative maintenance?

This inquiry becomes more pronounced when ETF flows are reintroduced into the analysis. Farside Investors’ spot Bitcoin ETF tracker has maintained a running tally for U.S. products, and the overarching trend throughout 2026 has been one of persistent outflow pressure.

Billions of dollars have exited this category this year. This flow pressure establishes a further layer of separation between Bitcoin’s price and the intentions of Bitcoin holders.

An ETF share represents Bitcoin exposure, yet the trading decision behind it may originate from an allocator shifting among products, a risk manager reducing gross exposure, or a portfolio adjustment that is largely unrelated to long-term perspectives on the network, the asset’s monetary principles, or self-custody.

When these two channels are combined, the market begins to appear different.

The first channel involves options, where expiry-related positioning can influence short-term movements as traders and dealers manage strike exposure, gamma, and settlement risks.

The second channel pertains to ETFs, where the flows mirror portfolio construction decisions within conventional finance as much as they reflect genuine interest in Bitcoin itself.

One channel relies on hedging mechanisms. The other depends on wrapper demand. Both exist one layer removed from the traditional perception of Bitcoin price being primarily determined by direct buyers and sellers in the spot market.

This layer shift has practical implications for individuals holding a small amount of BTC, owning an ETF in a brokerage account, or viewing Bitcoin as a signal asset. Many believe they are observing the asset’s demand. Increasingly, they are also monitoring demand for the structures surrounding the asset.

Diagram showing a three-layer Bitcoin investment structure: Layer 1 spot ownership, Layer 2 ETF and wrapper flows, and Layer 3 derivative machinery, with labels comparing market actors, objectives, and sources of price pressure.

Diagram showing a three-layer Bitcoin investment structure: Layer 1 spot ownership, Layer 2 ETF and wrapper flows, and Layer 3 derivative machinery, with labels comparing market actors, objectives, and sources of price pressure.

Related Reading

Related Reading

Related Posts

Bitcoin sets $88k ceiling for 2026: After a start this bad BTC has never finished a year positive

Bitcoin’s historically poor opening stretches establish an $88k ceiling for this year, with no precedent for recovery into a full-year gain.

Mar 27, 2026 · Liam ‘Akiba’ Wright

Why calm price action can carry more market stress than it seems

This helps clarify a pattern many individuals sensed during the recent sessions without precisely identifying it. Bitcoin around $67,000 may appear resilient. It can also seem oddly subdued given the surrounding macro noise and flow pressure.

The intraday range remained well within the emotional expectations typically associated with a quarter-end expiry of this magnitude. Such restrained movement often invites vague descriptions of indecision.

Significant expiry events can constrict movement as the market gravitates toward areas with the densest derivative exposure, then release that compression post-settlement when the hedge structure resets.

When open interest clusters around major strikes, the market may spend time hovering around levels that induce the least pain or imbalance into settlement. This dynamic is influenced more by positioning than by conviction.

Once this framework is established, several familiar frustrations become clearer. Bitcoin can maintain its value while ETF funds exit. Bitcoin can decline following positive long-term adoption news. Bitcoin can appear indifferent to narratives that would have previously triggered a more substantial movement.

These outcomes may seem contradictory when the market is evaluated as a direct reflection of Bitcoin conviction. They appear entirely coherent when the market is viewed as a layered structure where direct holders, ETF allocators, options traders, and dealers coexist, each with distinct motives and timeframes.

The deeper implication is psychological. Casual Bitcoin observers still tend to assume that a movement in the asset conveys a singular message. That assumption has always been flawed. It is now considerably weaker.

The market has become more transparent in one regard and less intuitive in another. There is more data available, more regulated vehicles, and more institutional entry points.

Simultaneously, the causal link between an individual wanting Bitcoin and Bitcoin’s movement has lengthened. There are more intermediaries involved, more wrappers around exposure, and more reasons for capital to engage with Bitcoin without sharing the perspective that formed the asset’s early holder base.

Many still perceive Bitcoin as the one major asset where ownership and conviction align more closely than in traditional markets. That relationship has weakened.

A person who directly owns Bitcoin in self-custody and a fund that acquires or divests Bitcoin exposure through an ETF are part of the same price formation process, albeit with entirely different behaviors influencing that process. Adding a substantial options market on top further detaches day-to-day movements from the straightforward question of who believes in Bitcoin.

The next test sits beyond expiry and ETF withdrawals

This does not diminish Bitcoin’s significance. It alters the landscape. Price discovery now comprises layers. The first layer involves direct spot ownership and exchange activity. The second encompasses ETF creations, redemptions, and secondary-market trading. The third includes listed and offshore derivatives, particularly surrounding large expiries. The fourth pertains to macro capital, which utilizes Bitcoin as one expression of a broader portfolio perspective.

Any trading session can be dominated by a single layer or by the interplay among several layers simultaneously.

The latter half of this month has provided a clear illustration of that layered structure. A significant expiry, noticeable ETF pressure, geopolitical tensions, and a spot price stabilizing around the mid-$60,000s created an unusual blend of noise and restraint.

This combination leads to an uncomfortable conclusion for those who still interpret every movement through sentiment. Short-term Bitcoin pricing is increasingly influenced by market mechanics.

Market mechanics are where much of the genuine price formation occurs once an asset becomes substantial enough to attract listed vehicles, options, and institutional balance-sheet management. Bitcoin has reached this stage. The change here is less about legitimacy and more about interpretation.

Retail can still influence the market, and long-term holders remain relevant to the structural supply dynamics. Their impact now coexists with a much larger array of participants whose goals are not accumulation, ideology, or even directional conviction. Their goal is execution.

Execution capital behaves differently. It purchases because a portfolio model indicates an increase in weight. It sells because a risk committee mandates a reduction in exposure. It hedges due to excessive open interest around a strike. It rolls because the calendar necessitates a roll. It responds to correlation and liquidity conditions before reacting to the Bitcoin white paper.

This represents a markedly different price-setting constituency from what many still envision when they analyze a Bitcoin chart.

The next test lies in the sessions following the expiry and in the ongoing pressure from ETF withdrawals. If Bitcoin begins to trade with greater directional freedom once the largest quarterly options event has concluded, it would reinforce the notion that hedging mechanisms had been compressing movement into settlement.

If ETF withdrawals continue to influence the demand structure, it would support the second aspect of the thesis: that the wrappers surrounding Bitcoin are exerting more impact on price discovery than many holders have fully acknowledged.

For anyone with capital exposed to markets, the essential adjustment is conceptual before it becomes tactical.

A Bitcoin chart prompts an immediate inquiry: What do Bitcoin buyers and sellers think at this moment? That question remains valuable. It no longer suffices.

A more pertinent question now lies one layer deeper: Which segment of the market is influencing price today, holders, allocators, or hedgers?

This represents a different perspective on Bitcoin, and once recognized, it becomes challenging to overlook.

The asset still retains its historical monetary and cultural arguments. Its short-term price formation now reflects a much more conventional market structure.

Bitcoin holders continue to participate in the market. They simply no longer occupy the central position in every movement.

The post Latest data shows retail Bitcoin wallets can no longer control short-term BTC price moves appeared first on CryptoSlate.