Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

How organizations transformed Bitcoin into a weekday market, leaving retail to bear the weekend risks.

Bitcoin may be available for trading 24/7, but its liquidity is no longer consistent. The cryptocurrency, which was anticipated to become more robust after attracting billions in institutional investments via ETFs, has instead developed a dual nature—appearing stable and organized during New York trading hours, yet significantly more vulnerable once Wall Street closes.

Recent data from Kaiko released this week quantifies what many traders have sensed for some time: the ETF-driven evolution that enhanced Bitcoin’s weekday market has simultaneously diminished its weekend trading, resulting in a bifurcated trading landscape where smaller participants bear a disproportionate amount of risk.

Since the introduction of spot Bitcoin ETFs in January 2024, institutional involvement has become concentrated during US weekday sessions, with approximately 47% of trading volume occurring during these hours, as per Kaiko’s analysis.

Weekday trading volumes consistently double those of the weekend, a disparity that has expanded throughout 2025 and into 2026 as institutional allocations have increased. The expectation of a uniform 24/7 market, a characteristic intended to set crypto apart from traditional finance, is diminishing in reality, as Bitcoin remains accessible every Saturday and Sunday, while the capital that supports its liquidity is absent.

BTC continues to trade 24/7, but significant liquidity is becoming more selective

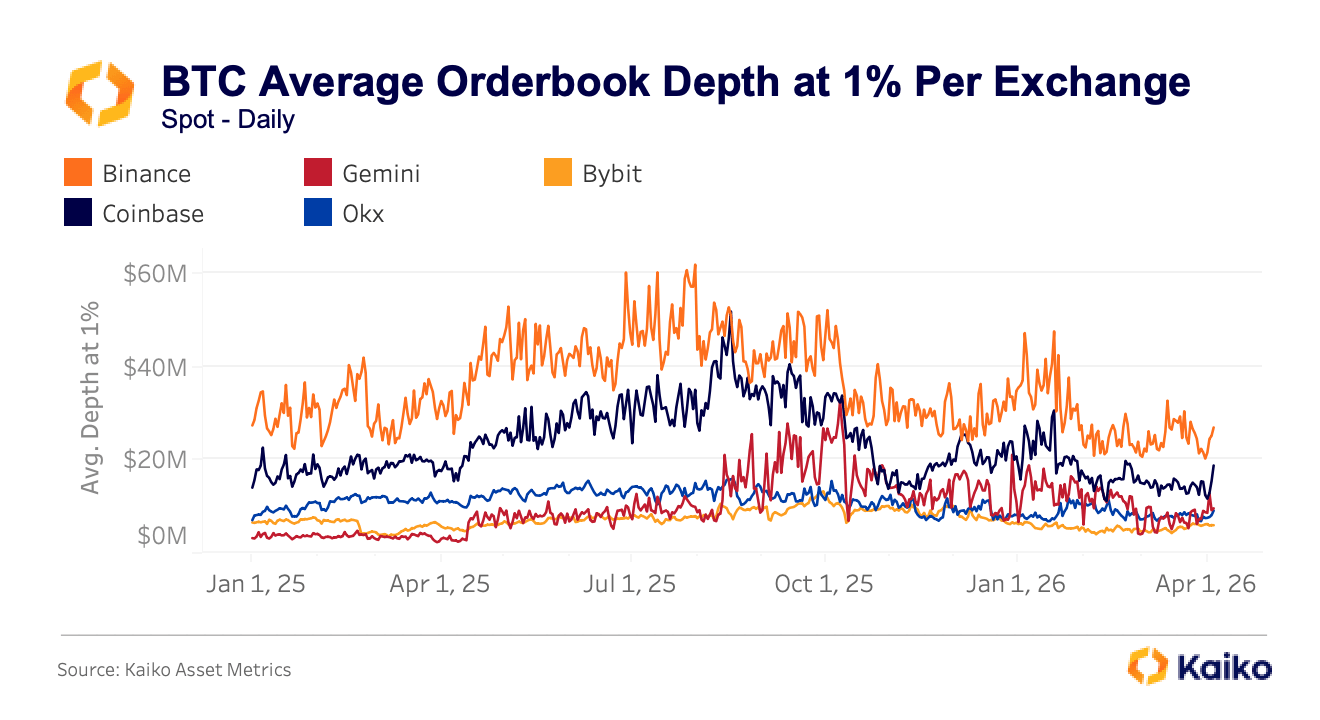

This change is evident in what traders refer to as orderbook depth, which measures the total dollar value of buy and sell orders within a specified range of the current price. This metric is crucial for assessing liquidity, as it indicates how much buying or selling a market can accommodate before the price begins to move unfavorably.

Kaiko monitors depth at 1% from the midpoint, meaning all resting orders within one percent above and below the current Bitcoin price, and this figure varies significantly depending on the trading platform. Binance consistently offers around $30 million in depth at that level, while Coinbase fluctuates between $16 million and $20 million.

Graph illustrating Bitcoin’s average orderbook depth at 1% across exchanges from Jan. 1, 2025, to Apr. 1, 2026 (Source: Kaiko)

Graph illustrating Bitcoin’s average orderbook depth at 1% across exchanges from Jan. 1, 2025, to Apr. 1, 2026 (Source: Kaiko)

Secondary exchanges, such as Gemini, Bybit, and OKX, generally display $10 million to $15 million in volume, resulting in a two-to-three-times differential that directly leads to less favorable prices for those placing significant orders on the wrong platform.

This differential does not remain constant under pressure; in fact, it tends to widen precisely when it is most detrimental. During the tariff-induced sell-off last October, BTC spot prices diverged significantly across exchanges within minutes, with Binance quoting $102,318, OKX at $102,142, and Bybit lagging at $101,675, creating a $643 spread that persisted for several minutes rather than the seconds typically expected if standard automated arbitrage mechanisms were effectively closing gaps.

This pattern recurred during the geopolitical tensions in the Middle East in March 2026, when the cost of trading BTC-USDT on Bybit surged 230% from its usual level, with similar spikes observed on OKX and Binance. Both incidents began on weekends, when institutional participants had already withdrawn, and order books were at their most sparse.

Related Reading

Related Reading

Bitcoin’s rebound looks like a trap as real Hormuz threat may not be over

Banks and energy analysts anticipate a slower recovery in oil flows, sustaining inflation and Fed risk for Bitcoin.

Apr 8, 2026 · Gino Matos

When Wall Street closes, the gap between “the price” and your price can widen rapidly

This situation has concrete and significant implications. On Feb. 1, Bitcoin’s price fell below $78,000 on a Saturday afternoon, resulting in approximately $2.2 billion in liquidations across more than 335,000 traders within 24 hours.

The decline was exacerbated by the structurally thin liquidity on weekends rather than by any specific negative news regarding Bitcoin, indicating that the market was not reacting to adverse information but rather to the mechanical reality that fewer participants were available to absorb selling pressure.

Related Posts

A subsequent analysis by VanEck of the broader February sell-off indicated that Bitcoin’s single-day price movement on Feb. 5 ranked among the fastest declines in the asset’s recorded history based on statistical measures of speed and magnitude, representing an extreme event that probability models would suggest occurs almost never, yet has now happened twice in five months.

A trader executing a buy or sell order on a Saturday evening, or on any secondary platform during heightened volatility, may not receive a price close to the consensus Bitcoin price they believe they are trading at.

The disparity between the quoted price and the executed price tends to widen when the repercussions of a poor fill are most severe, and this asymmetry disproportionately impacts participants who lack the institutional infrastructure to wait for more favorable conditions.

Related Reading

Related Reading

Bitcoin whales are dumping massive amounts of supply on exchanges as liquidations mirror the 2022 FTX market collapse

Traders search for “smoking gun” as rumors circulate, but ETF outflows and whale deposits provide clearer insights into Bitcoin’s steep decline.

Feb 6, 2026 · Oluwapelumi Adejumo

While retail traders clearly continue to engage in crypto, Kaiko’s research indicates they have been relegated to the thinner, less secure segments of the market. In terms of timing, retail traders are more vulnerable during off-hours and weekends, periods when ETF flows are inactive and institutional market-making diminishes.

Geographically, retail remains predominant in markets that do not resemble the US ETF-driven Bitcoin trade, with South Korea continuing to rely heavily on retail participation and altcoin volume, while Turkey’s crypto activity reflects macro-stress hedging and stablecoin demand rather than the institutional activity that has surged in the US.

There is also an asset dimension to this division.

Institutional capital, funneled through ETFs and prime brokerage arrangements, has standardized Bitcoin trading more than any other aspect of crypto, concentrating sophisticated market-making and deep liquidity around BTC, while leaving the remainder of the landscape (altcoins, local-currency pairs, smaller platforms) with thinner coverage and less professional support. Speculative and fragmented activity continues to thrive across the broader market, but not in the same exchanges and hours that institutions have occupied.

Same Bitcoin, different market quality

The data reveals a reality that is increasingly hard to ignore: there may now be two Bitcoin markets operating in parallel. A deeper, more efficient, institution-driven weekday market accessible through ETFs and prime venues, and a thinner, more volatile off-hours market where smaller traders are more likely to be present and more susceptible to the costs of poor execution.

In theory, Bitcoin is the same asset for all, but in practice, the quality of the market one encounters is heavily influenced by when and where one trades.

This is not an assertion that ETFs have harmed Bitcoin. Institutional involvement has provided tangible benefits, including enhanced aggregate liquidity, tighter average spreads during normal conditions, and a level of legitimacy that previous cycles lacked.

Cumulative net inflows into US spot Bitcoin ETFs remain around $53 to $54 billion since their inception, even after significant outflows in early 2026, and they have absorbed substantial capital and endured genuine volatility without collapsing.

However, the same dynamics that improved Bitcoin’s optimal trading hours seem to have revealed how uneven the market can become when that participation diminishes, offering maturity for some sessions while leaving fragility in others.

The post How institutions made Bitcoin a weekday market so retail takes on all the weekend risk appeared first on CryptoSlate.