Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Fed rate cut likelihood diminishes, raising concerns of stagflation where Bitcoin serves as a safeguard against prolonged inflation.

Wall Street has been engaged in discussions for months regarding the timing of potential interest rate cuts by the Federal Reserve. Currently, traders are contemplating whether the next action could be an increase.

Two days after the Fed’s decision on March 18 to maintain its target range at 3.50%-3.75%, markets reacted differently. Bloomberg-based pricing indicated over 60% likelihood of a rate hike by October, with approximately 15 basis points of tightening anticipated by that time. CME FedWatch estimated year-end hike probabilities closer to 40%.

The probability of a rate cut next month has decreased from 17% in February to 0% for April, while the likelihood of a hike has increased to 6%.

Despite the divergence that signifies a genuine disagreement regarding timing and conviction, both indicators are aligned in the same direction. Hike expectations, which had been dormant for several months, have resurfaced.

The catalyst for this shift is oil. Brent crude prices surged above $109, and US crude reached $98 on March 20, as tensions in the Middle East heightened concerns about potential disruptions to the Strait of Hormuz, a critical passage that facilitates nearly 20% of the global oil supply.

The EIA’s March baseline still predicts that Brent will decline below $80 by the third quarter and finish the year around $70 if disruptions subside. However, the market currently bets that this assumption is overly optimistic, and this sentiment is directly influencing rate expectations.

A data graphic illustrates Fed hike probabilities exceeding 60% on Bloomberg-based pricing as Brent crude surpassed $109 on March 20.

The 10-year Treasury yield rose to approximately 4.37%, the 30-year yield reached its highest level since September, and the S&P 500 was on track for a fourth consecutive weekly decline.

Global equity funds experienced a loss of $20.3 billion in the week ending March 18, with US equity funds alone shedding $24.78 billion, while money market funds attracted $32.57 billion globally.

Cash, yielding nearly 4%, is drawing capital away from risk assets in real-time.

The contradiction Bitcoin cannot evade

Bitcoin remained just below $70,000 on March 20, declining alongside QQQ (-1.75%) and GLD (-1.93%).

The same session that adjusted Fed policy to a more hawkish stance also led to a decrease in gold prices, despite a geopolitical context that should typically bolster hard-asset hedges.

Gold dropped 1.8% as yields and the dollar increased. The inability of the traditional inflation and war hedge to maintain its value can be attributed to tighter financial conditions that are simultaneously driving down both gold and Bitcoin, overshadowing any safe haven demand that the geopolitical situation might otherwise generate.

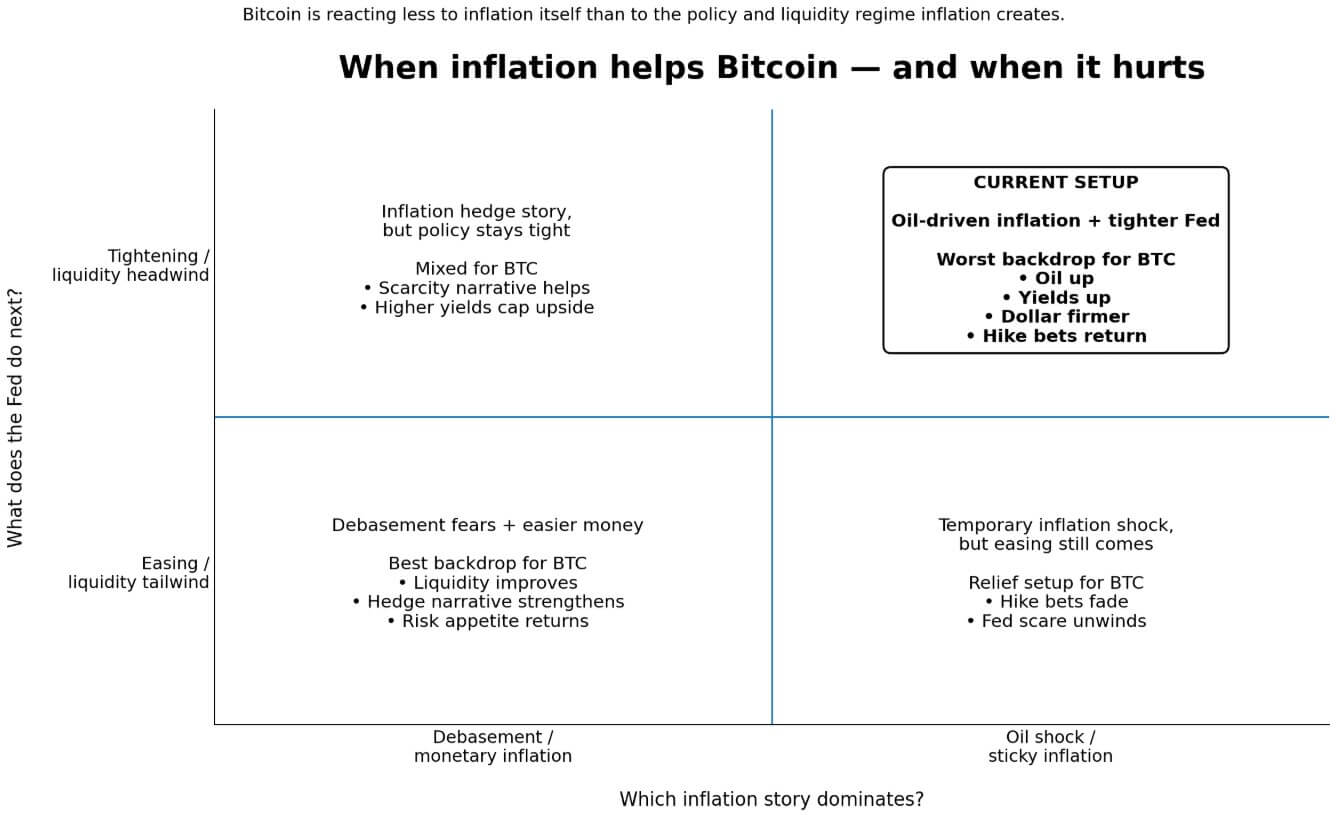

The argument for Bitcoin as an inflation hedge encounters a similar contradiction, as it is effective when inflation indicators suggest fears of debasement and the prospect of easier monetary policy. It struggles when inflation signals rising oil prices, increasing yields, a stronger dollar, and an unwillingness from the Fed to ease.

A four-quadrant chart illustrates Bitcoin’s performance across inflation and Fed policy scenarios, placing the current oil-driven situation in the least favorable quadrant.

A four-quadrant chart illustrates Bitcoin’s performance across inflation and Fed policy scenarios, placing the current oil-driven situation in the least favorable quadrant.

Fed Chair Jerome Powell stated at the conclusion of the March meeting that the central bank is monitoring whether rising fuel and input costs impact core PCE inflation.

If core inflation rises above 3.2%, which is Bank of America’s threshold for a credible case for a hike, alongside unemployment remaining near 4.5% and oil prices in the $80-$100 range, the Fed may find itself in a situation where inflation is persistent enough to maintain a tight policy stance.

However, growth has not yet weakened sufficiently to necessitate emergency cuts. For Bitcoin, this moderate inflation without recession scenario may represent the most challenging macro environment.

An IMF working paper indicated that a single crypto factor accounts for 80% of the fluctuations in crypto prices, and that Fed tightening diminishes that factor through a risk-taking channel.

Related Posts

Moreover, as more institutional capital has entered the crypto space, Bitcoin’s correlation with equities has increased. The BIS noted that the recent decline in crypto, with Bitcoin dropping approximately 50% from its 2025 peaks amid a broader shift away from growth assets, coincided with a sell-off in tech stocks.

Spot US Bitcoin ETF flows already reflect this shift: inflows of $199.4 million on March 17 turned into outflows of $253.7 million on March 18 and 19 combined, according to data from Farside Investors.

Bitcoin’s performance hinges on which aspect of the inflation scenario prevails: whether rising prices allow the Fed to ease or compel it to tighten.

Currently, the tightening narrative prevails, as conditions are constricting, the discount rate on speculative assets is increasing, and cash is becoming more attractive.

Two potential paths ahead

The bullish scenario relies on the EIA baseline remaining intact. If oil prices decline more swiftly than anticipated, labor conditions soften ahead of the April 3 jobs report, and the February PCE data on April 9 shows no second-round effects impacting core inflation, hike probabilities could diminish as rapidly as they increased.

One-year inflation swaps reached 3% this week, while the five-year forward swap fell to 2.35%, its lowest level in nearly a year. This movement suggests that markets still perceive a possibility of a temporary energy disruption rather than a fundamental regime shift.

If this scenario unfolds, Bitcoin could benefit from a liquidity tailwind. Citi’s 12-month framework establishes a base-case target of $112,000 and a bullish target of $165,000 under a scenario where the Fed resumes easing.

| Scenario | Macro trigger | What happens to Fed expectations | What it likely means for Bitcoin |

|---|---|---|---|

| Bull case | Oil retraces faster than expected; labor softens ahead of the Apr. 3 jobs report; Feb. PCE on Apr. 9 shows no second-round effects impacting core | Hike probabilities diminish; markets shift back toward pricing cuts or at least a less hawkish Fed trajectory | BTC regains a liquidity tailwind and can trade more on easing expectations than on tightening concerns |

| Bear case | Oil remains in the $80-$100 range into summer; core PCE rises above 3.2%; unemployment stays near 4.5% | Hike expectations solidify into a sustained higher-for-longer trade | BTC behaves more like a duration-sensitive risk asset, with tighter financial conditions and stronger cash competition impacting its price |

| What to monitor next | Apr. 3: jobs report; Apr. 9: PCE; Apr. 28-29: FOMC | Weak data would undermine the hike narrative; persistent inflation and robust labor would reinforce it | These releases will determine whether Bitcoin’s inflation-hedge narrative regains momentum or whether the liquidity headwind intensifies |

The bearish scenario hinges solely on the EIA being incorrect. If oil remains in the $80-$100 range into summer, core PCE exceeds 3.2%, and the April 28-29 FOMC meeting produces a statement that quietly affirms the market’s hawkish repricing rather than countering it, hike expectations will solidify into a lasting positioning move.

Money market assets are already approaching a record $8 trillion, and the flows that shifted into cash this week are unlikely to rotate back automatically. In that scenario, Citi’s recessionary bear case for Bitcoin projects a price of $58,000, with BTC trading as a duration-sensitive risk asset for as long as the rate ceiling remains in place.

The global perspective

Brokerages now anticipate that the ECB and the Bank of England may raise rates as early as April, with traders pricing in 72 and 78 basis points of tightening through 2026, respectively.

The Hormuz chokepoint also accounts for about 20% of global LNG trade. A prolonged disruption would elevate energy costs across Europe and Asia simultaneously, limiting the ability of any major central bank to ease.

Bitcoin’s correlation with global risk appetite, already intensified by institutional involvement, indicates that the tightening pressure is coming from multiple sources within the same macro environment that previously propelled crypto upward.

Long-term inflation expectations have not surged, and this containment is the only factor distinguishing the current repricing from a full-blown stagflation scenario.

Nonetheless, contained long-term expectations do not negate the immediate policy dynamics.

The Fed’s own dot plot allows for renewed hawkishness: participants’ appropriate-rate range for 2026 spans from 2.6% to 3.6%, and the variation at the upper end is sufficient to accommodate one or two inflation surprises before the median projection shifts.

Bitcoin now faces a critical test to ascertain whether it trades as an inflation hedge or as a concentrated bet on global liquidity.

The post Fed rate cut chance hits zero, threatening stagflation where Bitcoin thrives as a hedge against long term inflation appeared first on CryptoSlate.