Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Citadel and Fidelity have taken a significant step towards restructuring cryptocurrency in a manner similar to Wall Street.

EDX Markets’ pursuit of a federal trust bank charter represents more than just another instance of crypto expansion. It serves as a real-time examination of whether firms supported by Wall Street can integrate a larger portion of crypto’s custody and settlement framework within the U.S. banking system.

EDX, backed by Citadel, Fidelity, and Schwab, aims to apply equity market structure principles to crypto via a federal trust bank

EDX Markets’ request for a federal trust bank charter raises a more significant question than merely whether another major financial consortium seeks increased involvement in digital assets.

The more pressing inquiry is whether some of the companies that have influenced the development of modern U.S. equity market structure are now attempting to implement a similar functional division in crypto, with custody, settlement, collateral management, and fiduciary asset management being incorporated into a federally regulated banking framework.

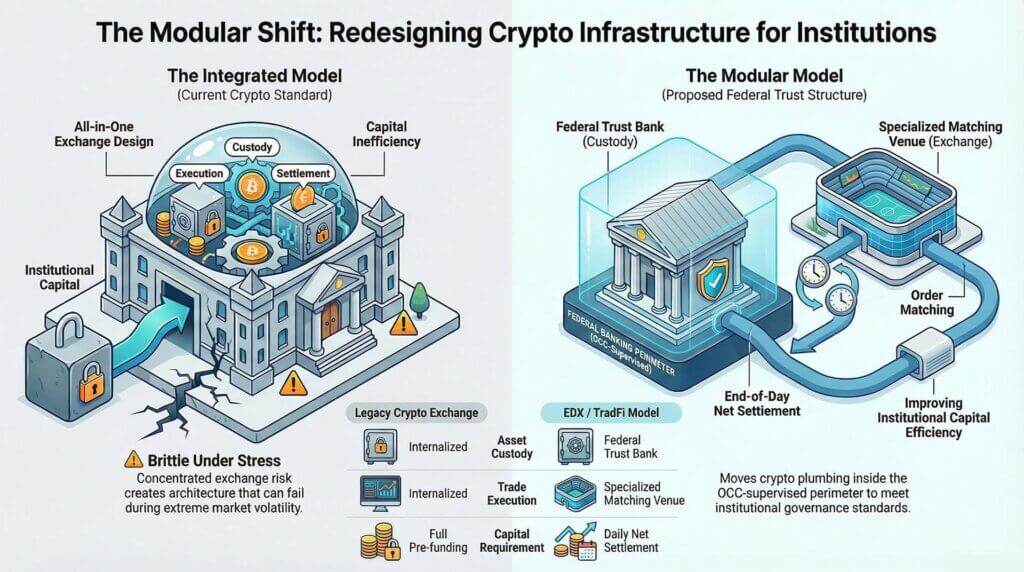

This perspective is directly derived from EDX Trust’s submission to the Office of the Comptroller of the Currency. The application contends that traditional financial markets have evolved around specialized roles such as brokers, exchanges, market makers, clearinghouses, and custodians, while digital asset markets have emerged around vertically integrated platforms where execution, custody, and balance sheet functions frequently coexist.

Why this is significant: Should this model gain approval and actual operational flow, a greater portion of crypto’s backend infrastructure could transition from all-in-one exchanges to federally regulated institutions. This shift would impact who manages custody, how trades are settled, and which firms become the preferred channels for institutional investment.

EDX’s proposal seeks to redefine this landscape. Order matching would remain with EDX Markets, while the suggested national trust bank would oversee custody, fiduciary asset management, settlement-related activities, and riskless principal operations.

Related Reading

Related Reading

The Fed is preparing to penalize banks for holding Bitcoin amid rising US crypto tensions

Basel’s thresholds and punitive risk weights can render direct Bitcoin exposure excessively costly, even when legally allowed.

Mar 13, 2026 · Gino Matos

For a market still influenced by the repercussions of concentrated exchange risk, this distinction lends significant weight to the application. The submission indicates a desire to shift a substantial portion of crypto infrastructure away from all-in-one venue designs and towards a modular structure that institutions are already familiar with.

The entities behind EDX bolster this interpretation. Citadel Securities, Fidelity, and Charles Schwab supported the venue at its inception, and the proposed trust bank emerges at a time when the federal charter process appears to be evolving into a competitive avenue rather than a mere regulatory experiment.

The OCC’s digital assets licensing applications page reveals that EDX Trust joined a growing list of pending applicants in March, alongside firms like Morgan Stanley Digital Trust, zerohash, and Revolut Bank US.

This follows the OCC’s December announcement that it had conditionally approved five national trust bank charters related to digital assets, including applications associated with Ripple, Fidelity Digital Assets, BitGo, and Paxos.

The competitive importance lies in the emerging pattern. Federal trust bank status is beginning to resemble a new layer of institutional crypto infrastructure, one that could influence who is allowed to intermediate regulated capital and who remains outside the most secure perimeter.

This gives EDX’s application broader implications than a typical custody expansion. The submission outlines a model centered on end-of-day net settlement for spot trades, as opposed to the heavily prefunded arrangements prevalent in many areas of crypto trading.

EDX asserts that this structure could enhance capital efficiency and lessen the operational burden on institutional participants. The intended users specified in the application highlight this ambition: broker-dealers, futures commission merchants, registered investment advisers, corporations, and other regulated intermediaries whose engagement relies on custody arrangements, counterparty controls, and supervisory familiarity.

Viewed through this lens, the application signals an effort to establish a crypto market structure capable of accommodating institutional flow on a larger scale, with federal oversight positioned closer to the assets and the settlement process than traditional crypto venues have historically permitted.

Related Reading

Related Reading

Congress has only weeks left to persuade banks on the crypto CLARITY Act or risk losing it to midterms

Congress must resolve the stablecoin yield impasse or leave it to regulatory interpretation amid intense banking pressure.

Mar 16, 2026 · Oluwapelumi Adejumo

Diagram comparing integrated crypto exchange model with modular institutional structure, showing custody, execution, and settlement separated into specialized components

Diagram comparing integrated crypto exchange model with modular institutional structure, showing custody, execution, and settlement separated into specialized components

Why the application highlights crypto infrastructure, not merely another access narrative

The most telling aspect of EDX’s application is its definition of the market issue. The document dedicates significantly more attention to structural separation than to promotional language regarding adoption or innovation.

This choice conveys a substantial message. EDX is essentially informing the OCC that the missing component in crypto is infrastructure that regulated institutions can navigate without adopting the operational and governance characteristics of vertically integrated exchanges.

This argument resonates because it aligns directly with how major financial institutions already conceptualize market participation. In equities and listed derivatives, institutions engage through a network of specialized actors and clearly defined responsibilities.

Matching venues match. Custodians provide custody. Clearing and settlement functions operate within distinct frameworks. Risk is assessed and transferred through established institutional channels.

By that standard, crypto still appears uneven. Exchanges frequently merge execution, asset custody, financing, and internal balance-sheet activities. The outcome is an architecture that can expand rapidly in bullish markets but appears fragile under pressure.

Related Posts

EDX’s proposed trust bank seeks to address that structural deficiency. According to the application, EDX Trust would offer custody for digital assets and fiat balances, fiduciary asset management, and settlement support for spot transactions executed on EDX Markets.

The filing also indicates that custodied cash and stablecoins would be invested in highly liquid instruments targeting returns near the federal funds rate, while custodied digital assets could be staked or utilized in permissible yield-generating activities. This expands the institution’s role beyond mere safekeeping, positioning the proposed bank closer to the core of collateral, idle asset utility, and balance-sheet efficiency.

Related Reading

Related Reading

White House sets February deadline to resolve $6.6 trillion dispute between Coinbase and banks

Even “crypto” is now divided, and the outcome will set the precedent for all future disputes regarding custody, DeFi, and taxes.

Feb 4, 2026 · Gino Matos

Settlement design is central to the proposal

The design of the settlement process is particularly crucial. EDX states in its OCC application that spot trades would settle once daily on a net basis, and that certain clients could post collateral instead of fully prefunding their activities, depending on their financial status and risk profile.

This represents a departure from one of crypto’s defining limitations, the necessity to hold capital across venues prior to execution. For active institutional participants, capital efficiency directly influences the volume of flow, the amount of inventory that must remain idle, and whether participation can extend beyond exploratory allocations.

This is where the EDX model begins to resemble an effort to integrate the practices of established market structures into crypto. The firms behind the venue possess a deep understanding of fragmented liquidity, specialized roles, and the economics of execution architecture.

Their application suggests that crypto can no longer depend on venue-centric designs to maintain institutional depth. While vertically integrated exchanges may continue to command substantial volumes, a federally chartered trust layer could become the preferred option for certain classes of institutions that have either hesitated or engaged only through limited channels.

A further indication lies in how EDX approaches custody itself. The application states that the proposed bank would employ sub-custodian banks to hold private keys. This introduces an additional layer of segregation and operational specialization.

It also reinforces the notion that the filing aims to establish clear boundaries around function, liability, and control. As these boundaries solidify, crypto infrastructure begins to mirror the institutional frameworks that dominate traditional capital markets.

The next challenge is whether institutions will shift flow, and if charter status will become a lasting advantage

The federal charter itself will attract attention, but the more enduring question is whether this model will draw genuine institutional migration. Regulatory approval would confer legitimacy and supervisory standing.

However, approval alone would still leave the commercial question of whether the architecture can attract flow. Institutions must determine whether the combination of a matching venue and a federally supervised trust bank offers a superior option for execution, custody, capital efficiency, and governance compared to existing crypto venues and current bilateral arrangements.

There are reasons to believe that this question is now pertinent. The OCC’s December conditional approval for Fidelity Digital Assets’ transition to an uninsured national trust bank indicated that the federal banking perimeter is already becoming more accessible to crypto-native and crypto-adjacent infrastructure.

Fidelity’s approval included considerations for crypto custody and trade execution services, establishing a significant benchmark within the broader shareholder ecosystem surrounding EDX. Simultaneously, the OCC’s current application queue suggests that several firms recognize strategic value in obtaining similar status.

As multiple entities pursue the same charter path, access to the charter begins to resemble a competitive boundary rather than merely a credential.

This competitive boundary could transform the exchange landscape. If custody, settlement, and collateral functions shift towards federally chartered trust institutions, the economic center of gravity in crypto could transition from venue-centric models to modular infrastructure.

A venue would still be crucial for liquidity, matching quality, market design, and access. However, the components of the stack that institutional allocators prioritize most—asset control, segregation, supervisory clarity, and settlement discipline—could migrate to entities specifically designed for those functions. This would challenge the long-standing rationale for consolidating everything under one roof.

EDX also enters this phase with a history of scale behind it. According to Ledger Insights, which referenced company figures, EDX processed $36 billion in cumulative notional trading volume during 2024.

This figure should be regarded as company-reported rather than independently verified market share, yet it still serves as a useful reference point. It indicates that EDX is filing from a position of operational experience rather than merely a concept.

The venue has broadened its listed assets significantly beyond its initial launch offerings. The operational premise is clear: EDX seeks a wider product range coupled with a structure designed to accommodate greater institutional participation.

The unresolved aspect lies in adoption. Major intermediaries and asset managers must determine whether a trust-bank-based structure genuinely enhances the economics and controls of participation.

Market makers will need to evaluate whether the model supports the depth and responsiveness they require. Institutions that currently route activity through crypto-native venues will weigh operational familiarity against the advantages of federal oversight and enhanced functional separation.

This comparison will ultimately decide whether this filing signifies a structural turning point or merely another incremental layer in crypto’s extensive regulatory development.

For the time being, the signal remains strong. EDX’s application frames the institutional bottleneck in crypto as a market-structure issue and proposes a federal trust bank as part of the solution.

This shifts the next phase of competition to a different arena. The market has spent years concentrating on products, access points, and the expansion of listed assets. The more significant contest may now lie deeper within the stack, where custody, settlement, collateral management, and supervisory architecture dictate who can facilitate the next wave of institutional flow, and under what conditions.

The post Citadel and Fidelity just made their clearest move yet to rebuild crypto like Wall Street appeared first on CryptoSlate.