Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Bitcoin value plummeted as a broader market downturn coincided with a $14 billion options expiration this morning.

The price of Bitcoin has once again been pressured downward due to an oil shock, rising Treasury yields, diminished expectations for rate cuts, and a significant Deribit expiry that is set to impact an already weakened market.

Approximately $14.1 billion in BTC options were scheduled to expire today, March 27, along with an additional $2.2 billion in Ethereum contracts expiring that same morning, resulting in a combined total of around $16.38 billion.

This represents nearly 40% of Deribit’s BTC open interest expiring in a single session.

According to Reuters, the overall risk-off sentiment is linked to oil prices exceeding $105, increased Treasury yields, a strengthening dollar, and markets eliminating Fed rate cuts for 2025 amid escalating tensions in the Middle East.

Yesterday, BTC recorded an intraday low of $68,127, while ETH reached $2,036. The expiry coincides with an ongoing selloff, and this morning Bitcoin has dropped to as low as $66,200, with Ethereum falling below $2,000.

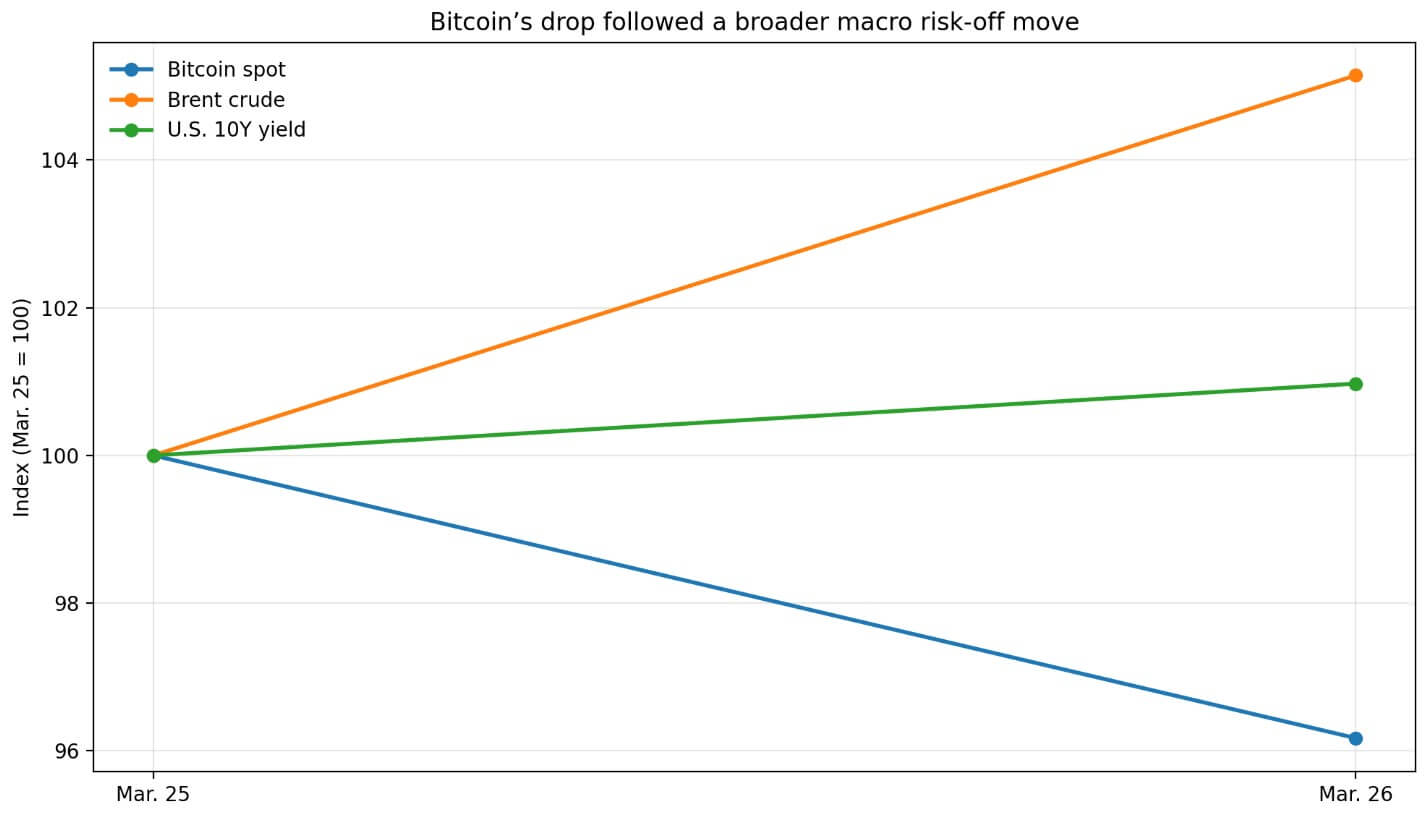

An indexed chart indicates that Bitcoin fell approximately 4% from March 25 to March 26 as Brent crude prices surged above $105 and the U.S. 10-year yield increased.

An indexed chart indicates that Bitcoin fell approximately 4% from March 25 to March 26 as Brent crude prices surged above $105 and the U.S. 10-year yield increased.

Why the final 30 minutes carry the most weight

Deribit settles expiring contracts at 08:00 UTC using a 30-minute time-weighted average of its index, sampled every four seconds from 07:30 to 08:00 UTC.

This method generates around 450 observations instead of a single closing price, making the delivery price more difficult to manipulate, while also ensuring that significant market movements during this period directly influence settlement.

At the same time, the delta of expiring options and futures declines linearly toward zero during the same 30 minutes. Hedges are being adjusted, rolls are compressing, and the pricing clock is ticking all at once.

This convergence attracts disproportionate attention relative to the duration of the window.

A 2025 SSRN paper utilizing Deribit data found that BTC options activity tends to cluster around 8:00-9:00 GMT, with the settlement-hour effect being most pronounced on days with a higher number of expiring contracts and shorter maturities. Both conditions apply in this instance.

| Metric | Value | Why it matters |

|---|---|---|

| BTC options expiring | $14.16B | Core scale of Friday’s expiry |

| ETH options expiring | $2.22B | Adds to broader market impact |

| Combined BTC + ETH expiry | $16.38B | Shows total size of the reset |

| Share of Deribit BTC open interest rolling off | Nearly 40% | Highlights concentration in one session |

| Settlement time | 08:00 UTC, Mar. 27 | Fixed event readers can watch |

| Key pricing window | 07:30–08:00 UTC | This half hour determines the delivery price |

| Settlement method | 30-minute TWAP of Deribit index | Final price is based on an average, not one print |

| Sampling frequency | Every 4 seconds | Produces about 450 observations |

| BTC spot reference | Near $68,000 | Baseline for all comparisons |

| BTC max pain | $75,000 | Positioning reference, not a forecast |

| Put/call ratio | 0.63 | Indicates positioning skew |

| Distance from spot to max pain | ~9.4% | Shows max pain is well above current price |

| 7-day BTC ATM implied volatility | 52% | Basis for estimating near-term move |

| Implied one-day move | ~$1,866 | Frames realistic daily range |

| Implied 30-minute move | ~$269 | Frames realistic settlement-window move |

| Max pain distance in 1-day sigma terms | ~3.45σ | Suggests $75,000 is far from likely daily move |

| Max pain distance in settlement-window sigma terms | ~24σ | Shows max pain is extremely far from a realistic 30-minute move |

A 2023 study identified a distinct Bitcoin expiration effect in terms of volume, volatility, and returns around maturity, with the most significant effects occurring shortly before or at expiry, though not uniformly across exchanges or contracts.

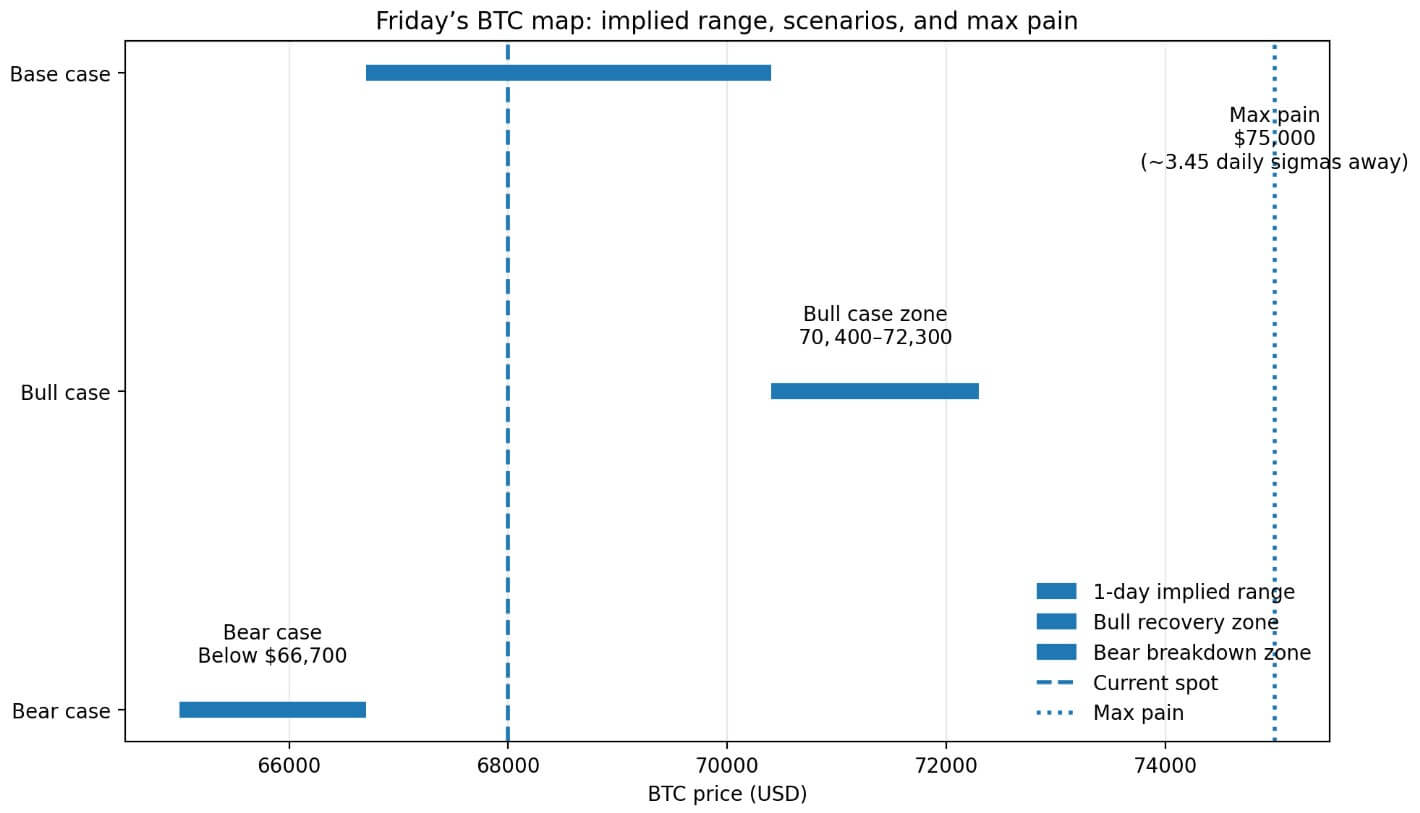

Reports referencing Deribit data indicated that Friday’s BTC max pain was set at $75,000, with a put/call ratio of 0.63. From yesterday’s spot near $68,000, this level was approximately 9.4% higher. Utilizing the stated 52% seven-day BTC at-the-money implied volatility, the implied one-day move is around $1,866, positioning $75,000 about 3.45 one-day sigmas above the spot price.

On a 30-minute implied-volatility basis, the implied settlement window move is approximately $269, indicating that $75,000 is nearly 24 settlement-window sigmas away.

At $75,000, max pain represents the point where open interest concentration is greatest, roughly 9.4% above the current spot and nearly 24 settlement-window sigmas away.

The macro arc that frames the expiry

Related Posts

BTC’s recent strength had already begun to weaken prior to the latest decline.

Deribit-related commentary on March 25 characterized Bitcoin as relatively stable amidst broader traditional market pressures, highlighted by declining equities and tighter credit conditions.

By March 26, that stability faltered: BTC fell below $69,000 as the oil shock, rising yields, and eliminated rate-cut expectations reasserted their influence.

Reuters reported that global equity funds lost $20.3 billion in the week ending March 18, while money market funds gained $32.57 billion, reflecting a widespread defensive shift.

Short-dated BTC implied volatility decreased from 57% to 52% this week as temporary de-escalation headlines emerged, while put skew remained intact. BTC 25-delta puts continued to be approximately 5 volatility points more expensive than calls, and BTC futures-implied yields hovered around 2%-3% across various tenors.

The market has accounted for a less immediate shock, while put skew and subdued futures yields maintain an overall cautious tone. A $14.16 billion expiry now occurs within this context.

Given that Deribit commands approximately 85% of the market share in BTC and ETH options, its settlement rules have implications that extend well beyond its user base. When a single venue’s 30-minute TWAP governs cash settlement for such a substantial notional, the mechanics of that window can influence the spot market.

The best and worst potential outcomes

A de-escalation announcement regarding oil or geopolitical issues did not materialize before 07:30 UTC, preventing BTC from rebounding toward the $70,400-$72,300 range, and expiry hedging mitigating downside rather than introducing new selling pressure.

The window could have served as a stabilizing factor: with spot prices firming and fewer in-the-money open puts, dealer hedging flows would have been less one-sided, and the settlement TWAP would have printed above recent lows.

The expiry could have concluded without incident, and macro relief might have propelled the price into the weekend. The indicator would have been spot recovering prior to the settlement opening.

However, the stress from oil and rates intensified into the morning. BTC fell below $66,700, the lower limit of the current one-day implied range, and now expiry mechanics introduce intraday volatility to an already bearish market.

Dealer hedges on put positions necessitate selling into a declining market, amplifying short-term fluctuations around the settlement window. The 30-minute TWAP is producing a delivery price that reflects the full macro impact, and now the expiry is accelerating the downturn.

The macro environment that prompted the move is now extending into the post-settlement session.

A price map indicates Friday’s Bitcoin implied range between $66,700 and $70,400, with max pain at $75,000, 3.45 daily sigmas above the spot price.

A price map indicates Friday’s Bitcoin implied range between $66,700 and $70,400, with max pain at $75,000, 3.45 daily sigmas above the spot price.

Academic research and Deribit’s own data confirm that the settlement hour influences flows and pricing mechanics.

This morning’s 07:30-08:00 UTC window concentrated on hedging behavior, delta decay, and pricing methodology, compressed into a single, clearly defined interval within a macro environment that has already driven BTC lower than the implied daily range.

The post Bitcoin price just collapsed because the macro selloff collided with a $14 billion options expiry this morning appeared first on CryptoSlate.