Disclaimer: Information found on CryptoreNews is those of writers quoted. It does not represent the opinions of CryptoreNews on whether to sell, buy or hold any investments. You are advised to conduct your own research before making any investment decisions. Use provided information at your own risk.

CryptoreNews covers fintech, blockchain and Bitcoin bringing you the latest crypto news and analyses on the future of money.

Bitcoin derivatives signal caution as $46 billion market retreats from Iran ceasefire surge.

On March 31, 2026, Wall Street experienced its most successful trading day in almost a year. The Dow Jones Industrial Average surged by over 1,100 points, the S&P 500 increased by 2.9%, marking its best single-day performance since last May, and the Nasdaq soared by 3.8%.

The sentiment, as one market summary optimistically referred to it, was “Hormuz Hope,” a rally fueled by the potential that the US-Iran conflict and its grip on global oil supplies might finally be easing.

President Trump indicated a willingness to conclude the military operations, while Iran’s president stated that his nation possessed “the necessary will to end the war” if its security conditions were satisfied.

However, beneath these headlines, traders engaged in the more intricate aspects of financial markets (the options, futures, and hedges) were not convinced. Although the market appeared to be stabilizing with potential for growth on the surface, the underlying positioning remained quite uncertain.

To comprehend why this is the case, one must understand two basic concepts: the meaning of “open interest” and what it indicates when it decreases. Open interest refers to the total value of active bets in the derivatives market, including futures and options contracts that have not been settled or closed. An increase in open interest signifies that more traders are investing, demonstrating confidence in the market’s direction. Conversely, a decline indicates that they are closing their positions, minimizing losses, and withdrawing.

Bitcoin’s $46 billion derivatives issue

Bitcoin trades continuously across numerous exchanges globally, effectively serving as a real-time indicator of global risk appetite, and currently, that indicator is providing an unclear signal.

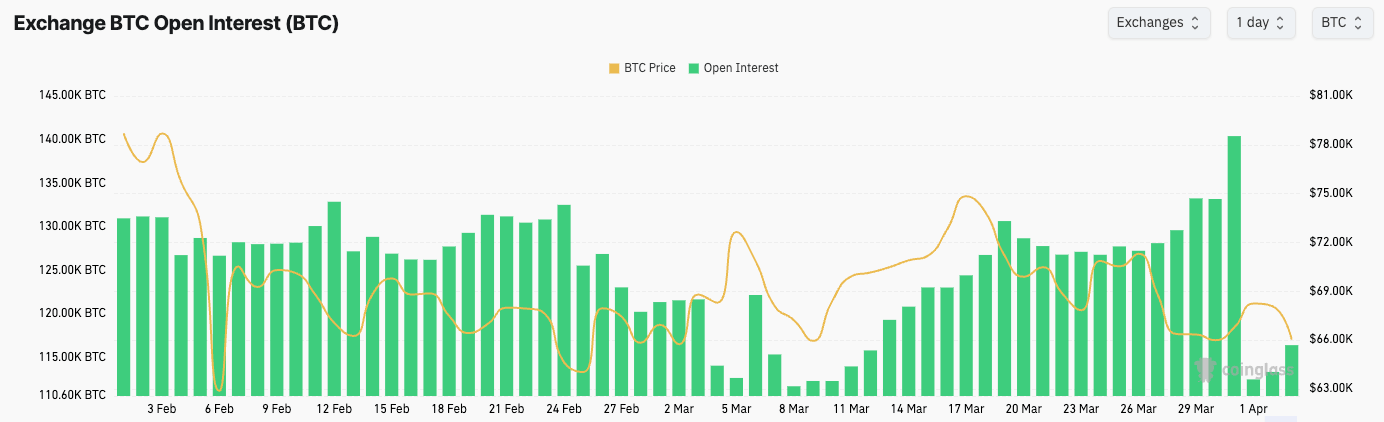

The total open interest in Bitcoin derivatives stands at approximately 703,940 Bitcoin, equating to around $46.85 billion in notional value, reflecting a market still heavily leveraged following a period of considerable stress. If hopes for peace were genuinely returning, a confident re-risking would manifest as traders making aggressive purchases. Thus, the 4.41% single-day decline in open interest observed on April 1 suggests more caution than conviction.

Chart illustrating the total Bitcoin open interest (BTC-denominated) from Feb. 1 to Apr. 2, 2026 (Source: CoinGlass)

Chart illustrating the total Bitcoin open interest (BTC-denominated) from Feb. 1 to Apr. 2, 2026 (Source: CoinGlass)

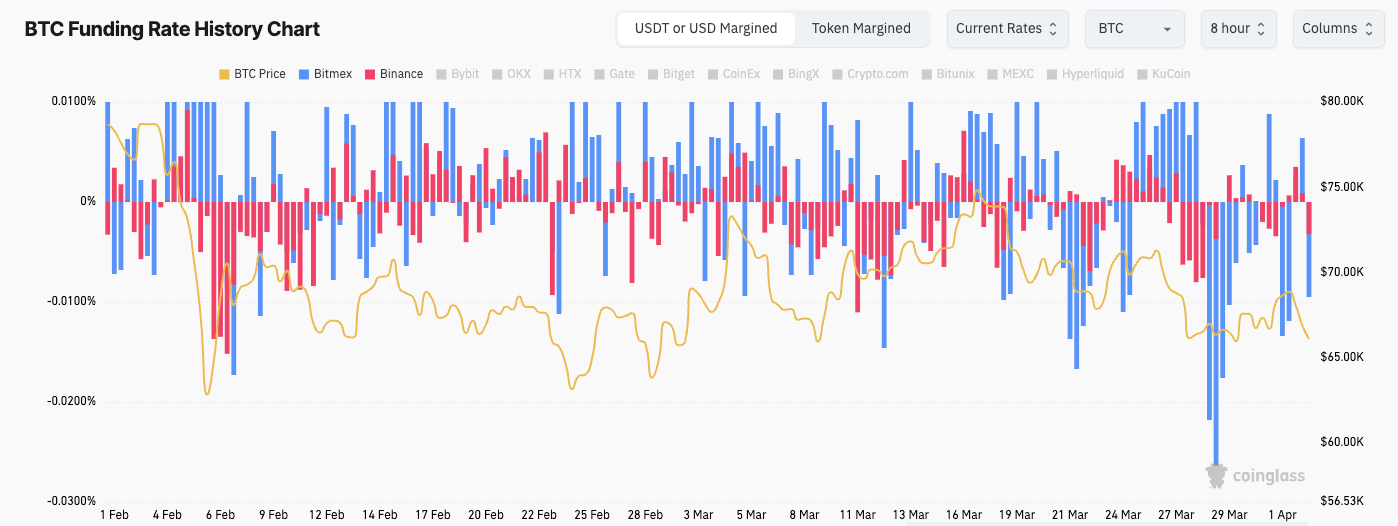

The funding rate, a fee that traders maintaining bullish positions must pay, has remained only slightly positive, marked by repeated negative dips. When funding rates spike, it indicates that bullish sentiment has pushed open interest to unsustainable levels, with buyers significantly outnumbering sellers. The subdued, flat-to-barely-positive funding rate for Bitcoin observed over the past two weeks suggests a lack of enthusiasm for new risk.

Chart depicting the funding rate for Bitcoin perpetual futures from Feb. 1 to Apr. 2, 2026 (Source: CoinGlass)

Chart depicting the funding rate for Bitcoin perpetual futures from Feb. 1 to Apr. 2, 2026 (Source: CoinGlass)

What makes this harder to dismiss as mere noise is the significant growth of institutional involvement in Bitcoin derivatives. Of that $46 billion in open interest, over $7 billion is held on CME, the regulated exchange where pension funds and sophisticated asset managers primarily conduct their hedging. The increase in institutional open interest has positioned Bitcoin as a mainstream financial asset, indicating that the retreat reflects decisions made in corporate boardrooms and trading desks, far beyond retail market speculation.

The ratio of options to futures in Bitcoin has also changed. Earlier this year, options, which function like insurance policies and provide protection against sudden price fluctuations, represented a much larger portion of the Bitcoin derivatives market, but that ratio has since decreased to about 65%, sharply down from nearly 90% last month.

As options exposure diminishes and futures take precedence, the market becomes more directional and less insulated: manageable, until a rapid downturn occurs. Data indicates particular sensitivity concentrated in the $66,000-to-$67,000 price range, an area where large positions seem to be concentrated and where a return to that band could destabilize the market quickly.

Related Posts

Oil options reflect the same narrative

The Strait of Hormuz, the 21-mile chokepoint through which approximately 20% of the world’s daily oil consumption passes, has seen commercial traffic significantly reduced since the onset of the conflict. Nearly 17.8 million barrels per day of oil and fuel flows have been disrupted, with close to 500 million barrels of total liquids lost thus far, according to Rystad Energy.

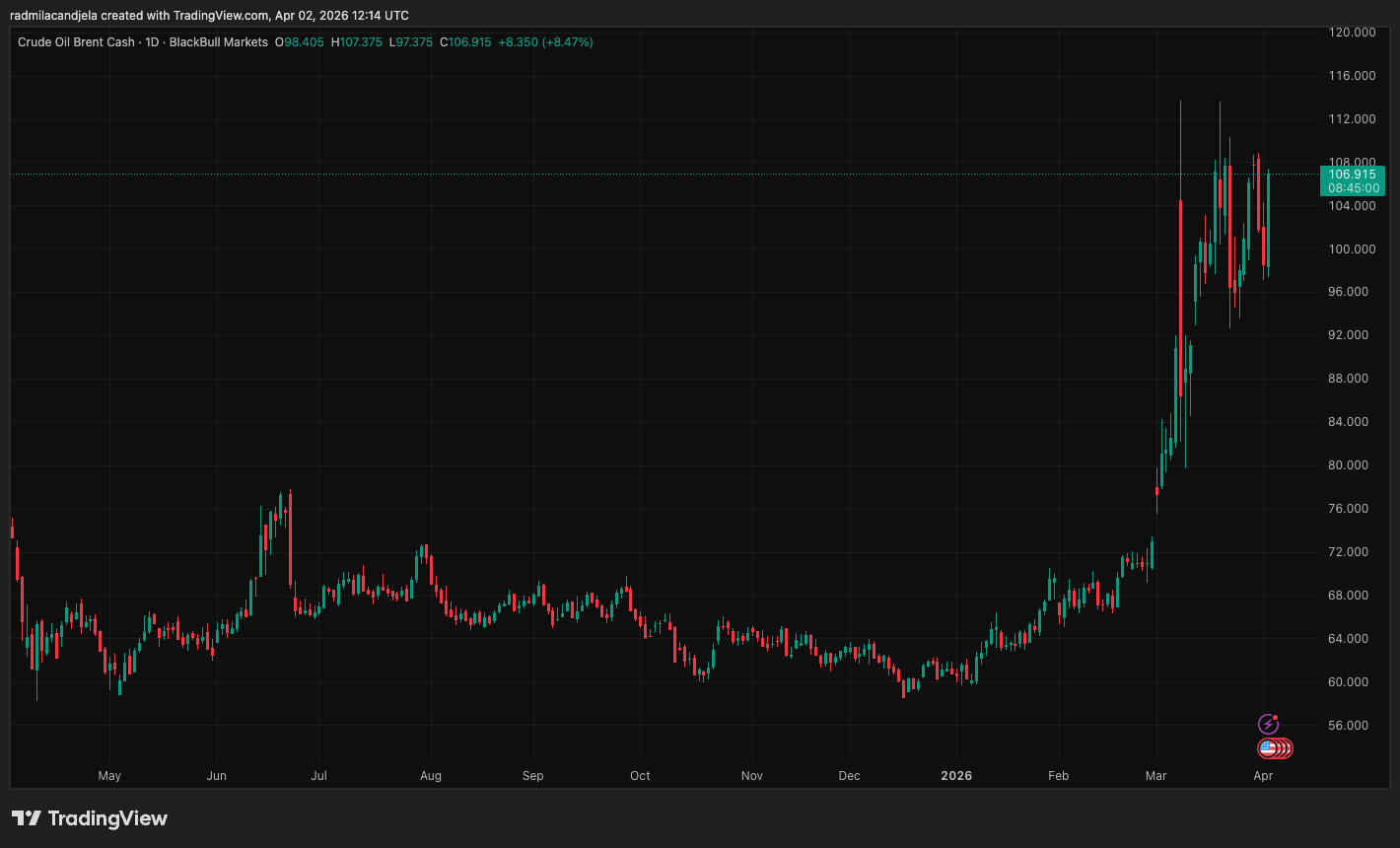

When Brent crude briefly fell below $100 a barrel on April 1, retreating from highs exceeding $112 just days prior, markets interpreted it as confirmation that the worst was behind them.

Graph showing the price of Brent crude oil from Apr. 1, 2025, to Apr. 2, 2026 (Source: TradingView)

Graph showing the price of Brent crude oil from Apr. 1, 2025, to Apr. 2, 2026 (Source: TradingView)

However, the options market remained considerably less certain. Ownership of Brent call options betting on crude reaching $150 a barrel by the end of April has surged tenfold in the past month, with open interest in those contracts now at nearly 29,000 lots, each representing 1,000 barrels of oil. This clearly indicates that the markets are considering tail risk scenarios related to this conflict.

The largest concentration of open interest remains in $100 call options, a positioning that reflects a market still hedging for further upside shocks rather than celebrating a definitive resolution.

deVere CEO Nigel Green articulated the underlying concern:

“Brent at $115 is being treated as a spike. The data tells a different story. Prices have risen nearly 60% in a single month, options markets are actively pricing scenarios of $150 oil, and up to 20% of global supply has been disrupted through the Strait of Hormuz. Those are not conditions associated with a short-lived shock.”

This perspective finds an unsettling resonance in the diplomatic record itself. Trump stated that Iran had requested a ceasefire; Iran’s foreign ministry labeled the assertion as “false and baseless.” With two governments presenting irreconcilable accounts of the same negotiation concerning the same chokepoint, the market rallied on the more optimistic narrative while the hedges continued to price both outcomes.

The outcome is a gap that is straightforward yet significant. Stocks are responding positively to a ceasefire framework that remains unverified, Bitcoin open interest is declining when it should be increasing, and oil options are still pricing a substantial likelihood of another energy spike.

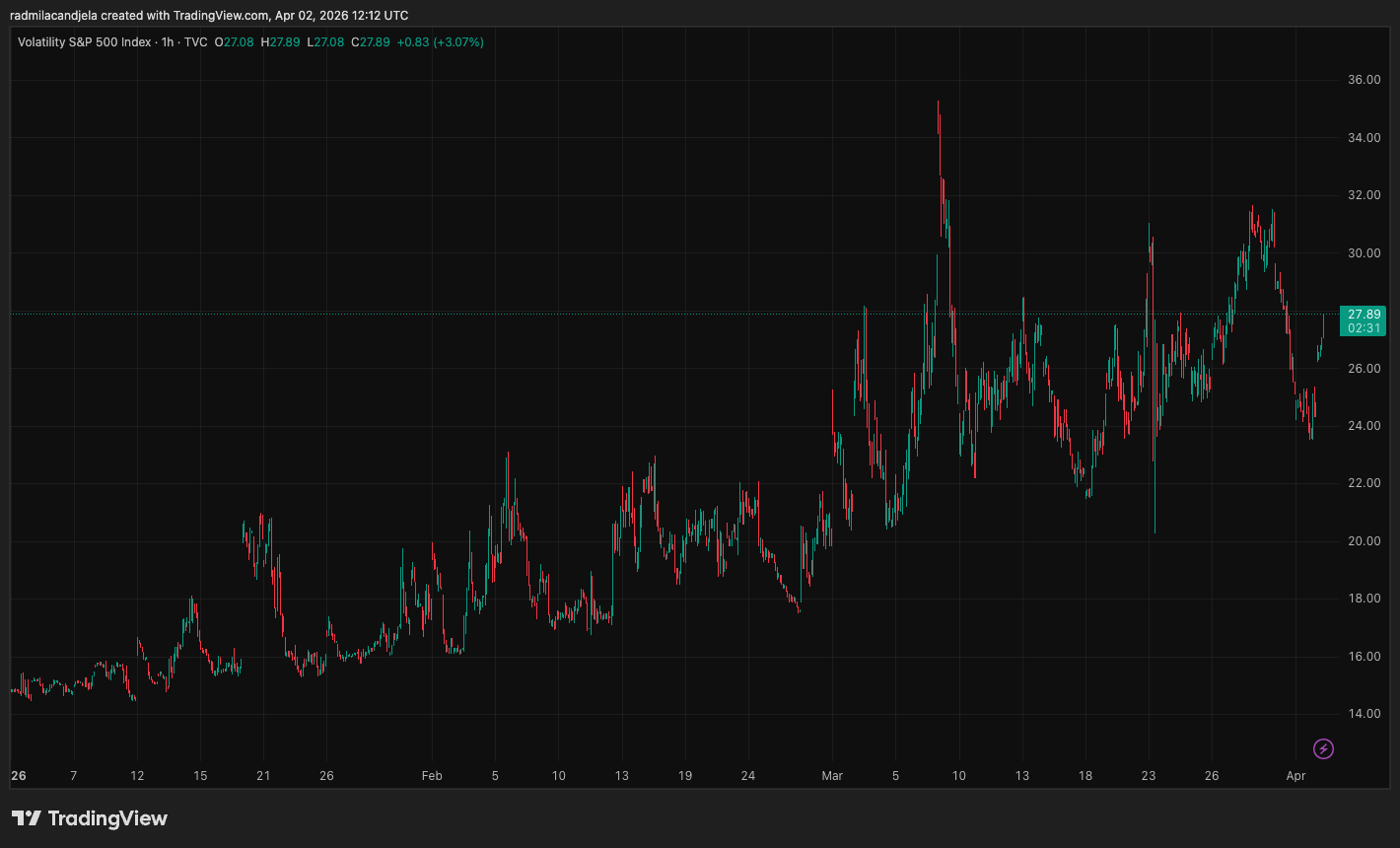

The VIX, Wall Street’s fear gauge, decreased but remained at 24.54, a level that still indicates heightened anxiety. Markets are generally adept at pricing the future they desire, but the derivatives beneath them tend to price the future they fear, and currently, those two futures appear quite divergent.

Graph illustrating the S&P 500 volatility index from Jan. 2 to Apr. 2, 2026 (Source: TradingView)

Graph illustrating the S&P 500 volatility index from Jan. 2 to Apr. 2, 2026 (Source: TradingView)

The rally has eased the headlines without resolving the underlying positioning, and if the ceasefire collapses, Bitcoin and oil are likely to be among the first indicators of that shift.

The post Bitcoin derivatives flash warning as $46B market pulls back from Iran ceasefire rally appeared first on CryptoSlate.